Company Overview - OneVue Holdings Limited is engaged in providing outsourced superannuation administration, unit registry and responsible entity services, and end-to-end superannuation services, including the provision of investment and portfolio administration, tax and reporting services. The Company's segments include Fund Services, Platform Services and Corporate. The Fund Services segment provides outsourced unit registry and installed software to a range of investment managers, custodians, trustees, responsibility entity services and superannuation administration. Its Platform Services segment offers services, including investment administration, tax and reporting services for both superannuation and other investments, a retail superannuation fund, self-managed superannuation fund (SMSF) compliance and administration services and investment management. It manages asset classes, including listed shares, term deposits, warrants, as well as personal assets and investments, including collectibles.

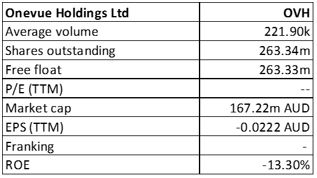

OVH Details

Generated operating cost savings with Diversa acquisition: Onevue Holdings Ltd (ASX: OVH) reported that they were able to generate $2.3 million in the annualized operating cost savings in the first month after finishing the Diversa acquisition, which represents 57% of the overall expected synergies of $4 million per annum. The associated redundancy costs of $0.5 million would be reflected in the interim profit results for the first half of FY 17. Moreover, OVH is confident that the residual $1.7 million forecast operating cost savings would be achieved by the end of the FY 17. In addition, Diversa's revenue performance since acquisition is also on track. OVH expects that the combination of the two businesses would be earnings per share (EPS) accretive in the first year (this excludes any one-off transaction and integration costs) due to the major level of expected cost synergies (in the order of $4 million per annum) by the end of FY18 (excluding one-off transactions and integration costs). Diversa business generated a pre-acquisition run rates and FUTMA (Funds under trusteeship, management and administration) at $9.3 billion as of September 2016 which is a rise from 27% as compared to the same period of last year and from 8.7 billion in the earlier quarter. Rising assets from current clients drove this performance.

Zero Debt and Positive Operating Cashflow for consecutive quarters: OVH’s operating cashflowin the September quarter 2016 grew by $707k on the back of the redundancy payments of $302k primarily made in the prior financial year and for performance fees that was received of $718k. Moreover, the cash at quarter end is at $18.7 million and there is no debt outstanding. The estimated cash outflows for the next quarter would include the estimated operating costs of Diversa from acquisition date and the expected restructuring and redundancy costs.

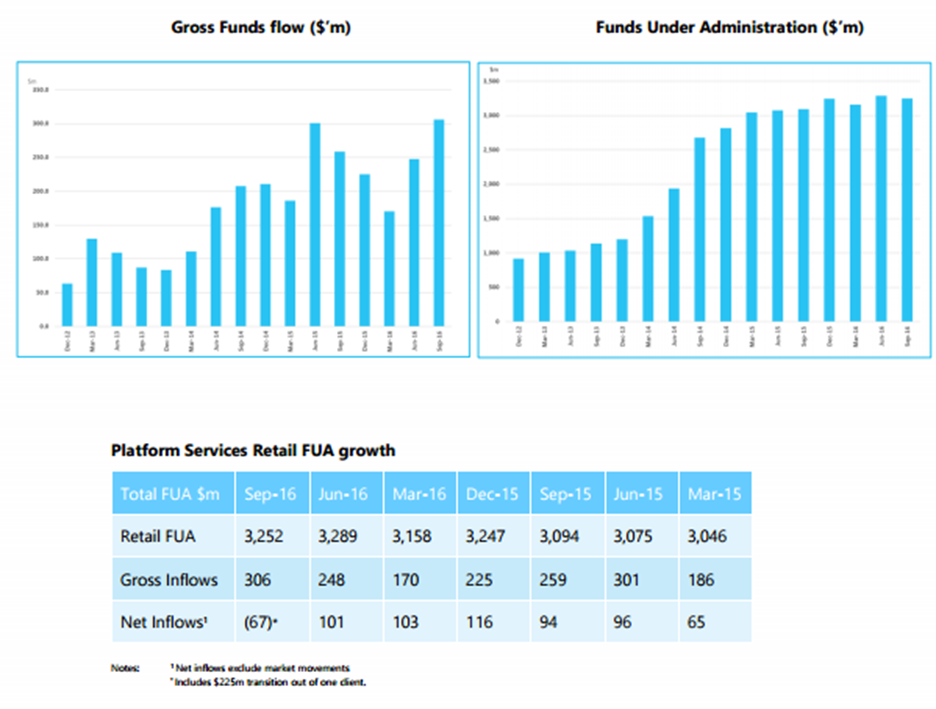

Strong Fund Services unit registry business: The Fund Services unit registry Funds under Administration (FUA) rose $17.5 billion for the September quarter of 2016 to close at $427.4 billion. The Fund Services unit registry transactions rose 113% as compared to the corresponding quarter and is up 5% on the prior quarter, while $2.9 million per annum of contracted revenues would transition over the next 12 months. Additionally, The Fund Services unit registry team has added 237 new funds in a year and is now administering over 480 funds on behalf of 34 fund managers, which would further cement OVH’s position as Australia’s leading outsourced unit registry provider. The business has received another unqualified audit for the year with SLA’s continuing to track above 99%. In addition, the contracted transitions would add $2.9 million per annum over the next 12 months and there is a high probability pipeline that could be more than double the organic revenue growth over the next 3 years.

.png)

Fund Services key statistics (Source: Company Reports)

On the other hand, Superannuation Services FUA at the end of September 2016 quarter is of $789 million, which is down on the previous quarter, due to the transition out of 1 fund with $293 million of FUA. However, 5 new funds were added in the previous quarter and a new fund with $375 million in FUA and 3,500 members is currently being transitioned with completion due by the end of the December quarter.

Platform Services received record inflows: OVH’s platform service got the record gross inflows of $306 million in the September quarter 2016, which is a growth of 18.3% as compared to the corresponding quarter of 2015 taking the inflows to $949 million for a year. However, the net inflows were affected by a one-off transition from a $225 million client moving to an insourced model, which would more than offset by the transition of new clients in FY 17 including a new client with $200 million of FUA (a leading provider of specialist financial products, services and advice). Moreover, Platform Services LUMINOUS and FUND eXchange have created a disruptive platform growth strategy. In addition, OVH had launched new products in FY 16, consisting of release of a new white label ‘Compass Funds’ with Sentry Group to advise on over $5 billion of funds. The group also launched international SMA capability, added 5 suites of managed fund model portfolios within the product structure of an SMA or MDA, enabling the advisers to enhance their back-office efficiency. Overall, OVH’s Platform Services is now positioned to capitalize on the projected growth in the managed account sector.

Growth of Fund flow (Source: Company Reports)

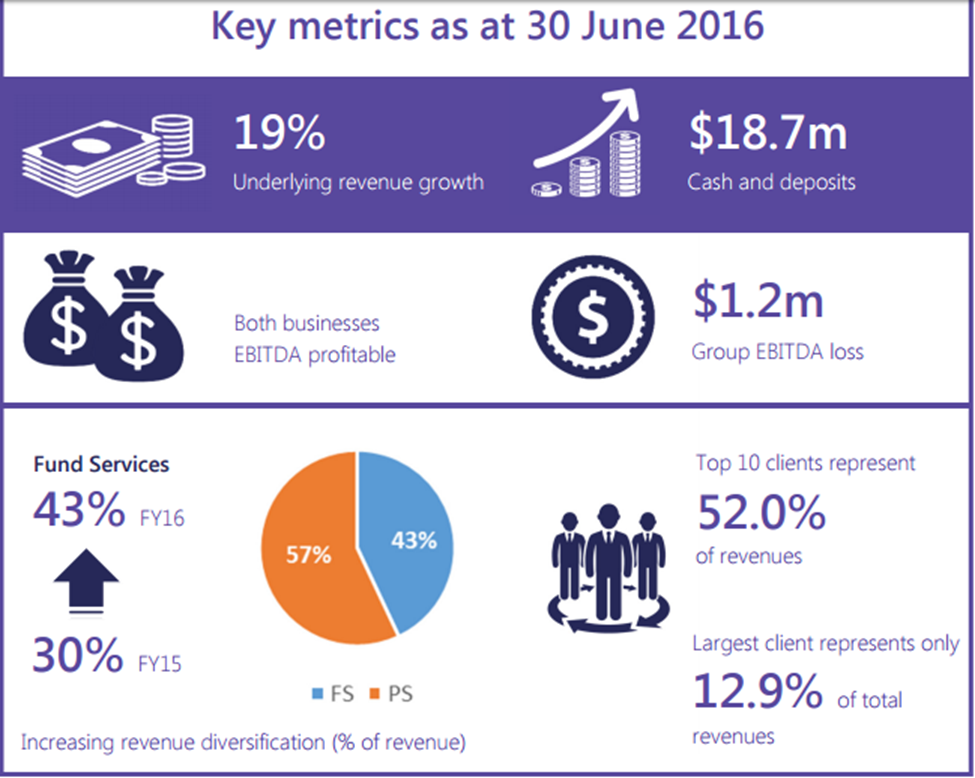

FY 16 financial performance highlights: OVH had reported a 5% growth in the revenue for fiscal year of 2016, which includes the 19% growth in the total services revenue but got impacted by lack of performance fees which fell 91%. The total services grew due to the 56% growth in the fund services and a 4% growth in platform services despite the market’s performance of -4%. Moreover, the underlying EBITDA grew $1 million (excluding performance fees) and both the operating businesses posted positive EBITDA results with growth. Meanwhile, the group is also boosting its capital position and raised over $17.5 million in FY 16 that got oversubscribed and continued to support the accelerated growth both organically and by acquisition.

FY 16 Financial Performance (Source: Company Reports)

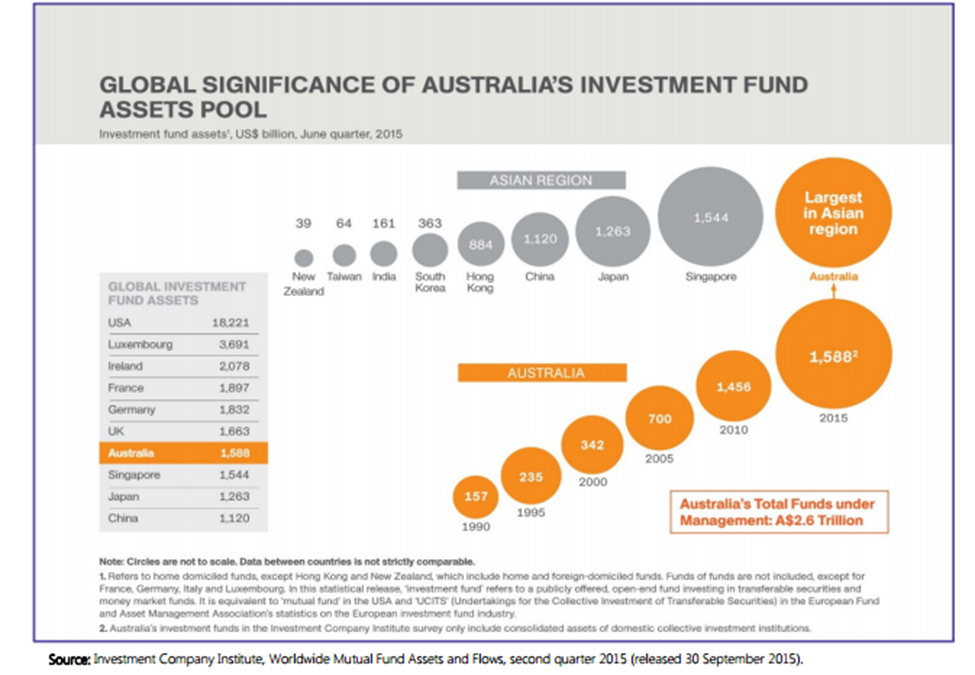

Significant target market opportunity: Australian superannuation FUM is forecasted to rise at a CAGR of 6.6% in the next 10 years. Accordingly, the group is positioning its portfolio to leverage this potential opportunity. OVH is decreasing its client concentration risk wherein their top 10 Onevue clients account 52% of total revenue while the largest single client accounts less than 13% of total revenue. The group is also enhancing their Fund Services revenues composition, which now accounts more than 43% in 2016 against 30% in 2015. Consequently, OVH is generating organic growth driven by rising superannuation assets and the direct benefits of this growth to both investment managers and superannuation service providers. The group is expanding its portfolio via acquisitions and with Onevue Super Services acquisition, the group would retain current clients while cross-selling and upselling further products or services to these clients. OVH had acquired Super Managers Australia, which is now Onevue Super Services to position them for growth in superannuation administration and has reported revenues above the expectations. The group’s outsourced unit registry solution is a major player in the delivery of a highly scalable, competitive offering which now has over $410 billion in Funds under Administration (FUA). This comprises 213 funds while 22 new investment managers are added during the year and over 450 funds are currently administered.

Australia’s position in Investment fund assets (Source: Company Reports)

Stock Performance:The shares of OVH stock declined over 8.2% in the last three months (as of November 14, 2016) given the current volatile environment in Australia and across the globe. On the other hand, the group intends to continue to focus on integrating their Diversa business into Onevue’s operating model as well as generate $4 million of committed synergies. The group intends to leverage the Onevue ecosystem to deliver the FUND.eXchange while Fund Services transitions are in the pipeline. Although these transitions might not generate immediate benefits, they would strengthen the group’s FUND.eXchange product menu. The group will hold its Annual General Meeting on November 24, 2016. Based on the foregoing, we give a “Buy” recommendation on the stock at the current price of – $ 0.59

OVH Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...