Company Overview: OneVue Holdings Limited is engaged in providing outsourced superannuation administration, unit registry, and end-to-end superannuation services, including the provision of investment and portfolio administration, tax and reporting services. The Company's segments include Fund Services, Platform Services and Corporate. The Fund Services segment provides outsourced unit registry and installed software to a range of investment managers, custodians, trustees and superannuation administration. Its Platform Services segment offers services, including investment administration, tax and reporting services for both superannuation and other investments, a retail superannuation fund, self-managed superannuation fund (SMSF) compliance and administration services and investment management. It manages asset classes, including listed shares, term deposits, warrants, as well as personal assets and investments, including collectibles.

OVH Details

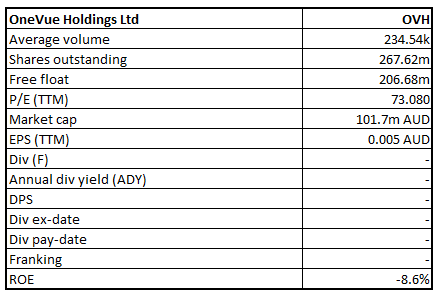

Decent Recurring Revenue Growth in FY19: OneVue Holdings Limited (ASX: OVH) happens to be a wholesale service provider to wealth management industry that carries out operations primarily via Fund Services and Platform Services, which contributed revenue around 64% and 36%, respectively of the total revenue as at 30 June 2019. As on November 19, 2019, the market capitalisation of OVH stood at ~A$101.7 million. The company has released an annual report for the period ended June 30, 2019, wherein revenue from continuing operations increased by ~35% to $49.62 Mn as compared to the prior year. Notably, 93% of the revenue is recurring, which underscores the quality of the company’s revenues. In FY19, the company’s EBITDA witnessed a rise of 59%, while its NPATA rose by 34%. Also, the company has declared a net gain of $8.6 million as a result of divestments. The company added that FY19 witnessed the completion of simplification of the business, freeing the management to focus on high-growth core sectors of Fund Services and Platform Services. It was also added that Fund Services, for the first time, is representing more than 60% of the company’s total revenues.

There are clear growth runways with respect to Fund Services and Platform Services, with strong tailwinds, which have been identified as the greatest margin improvement opportunity revolves around transitioning the clients already won. However, what might impact business in the short-term is the timing of some of the transitions, primarily those transitions which are being managed in the partnership with large institutions. They have been impacted by the new regulatory environment as well as increased governance and complexity. However, only the timing of revenue is impacted and not overall certainty of the positive impact of revenue. It was also stated that upon receipt of $31 million in the final proceeds from sale of Trustee business, the company’s net cash position would be exceeding $40 million and the company plans to look towards smart capital management. This includes payment of 2.19 cents per share special dividend (fully-franked) to the shareholders, pursuing other opportunities and considering a buy-back event. Therefore, it can be said that the company has been focusing on providing returns to shareholders, which might help it in getting traction among the market participants.

Against a backdrop of low-interest rates, shifts in the superannuation landscape, volatile markets, turmoil in advice market, and increasing momentum from active to passive investing, the company is well-placed to seize opportunities as they emerge. Moreover, favourable structural environment helped by the government mandated superannuation is anticipated to support the favourable outlook for year ahead, and beyond..png)

FY19 Financial Results Highlights (Source: Company Reports)

Top 10 Shareholders: The following table provides a broader overview of the top 10 shareholders in OneVue Holdings Limited:.png)

Top 10 Shareholders (Source: Thomson Reuters)

Overview of OVH’s Margins: The company’s gross margin stood at 83.4% in FY19, which is higher than the industry median of 66.3%, therefore, it can be said that OVH is generating respectable levels of revenues. The company is possessing an EBITDA margin of 10% in FY19. OVH has a decent liquidity level as can be evidenced by its current ratio of 2.70x in FY19, which is higher than FY18 figure of 1.05x and, thus, it can be said the company is capable enough to meet its short-term obligations. Also, a decent base of liquidity might also help OVH is making deployments towards strategic business objectives. Debt/Equity ratio has declined significantly in FY19 on a YoY basis and, thus, it can be said that OVH has been focussing towards deleveraging its balance sheet. Generally, a lesser debt reflects that the balance sheet is more or less, stable, which might help the company in focusing towards long-term growth objectives..png)

Key Metrics (Source: Thomson Reuters)

Key Business Measures of September 2019 Quarter: With respect to Managed Fund Administration, the company stated that record number of the items were processed in September 2019 quarter and the figure stood at 173,687, which reflected a rise of 44% on pcp basis and the growth was because of the addition of new funds as well as ongoing growth from existing funds. The funds under administration (or FUA), even though not the driver of revenue, ended at $530 billion, which indicates scale and market leadership position. It was also added that business has been participating in significant new business opportunities and has a robust pipeline as more and more fund managers are looking to outsource fund administration to the specialist providers..png)

Fund Services (Source: Company Reports)

With respect to Superannuation Member Administration, the company stated that the number of members reached 159,063 that is up 7.6% on pcp basis. More than 45% of the member growth in September 2019 quarter was witnessed from new funds. Notably, FUA as at September 30, 2019, stood at $5.45 billion, implying a rise of 14.7%. The business has been focusing towards the integration as well as automation to help further growth and margin expansion.

Coming to the Platform Services segment, the FUA amounted to $5.8 billion as at September 30, 2019, reflecting a rise of 28% on pcp basis. The business encountered gross inflows amounting to $488 million, reflecting a rise of 56% on pcp basis and net inflows stood at $228 million, which were up 92%. However, a one-off outflow amounting to $30 million following the sale by adviser of their client book impacted FUA in September quarter. It was mentioned that the total annual net inflows reached $1.1 billion.

Decent CAGR Witnessed in OVH’s Revenues: The company’s total revenues have witnessed a CAGR growth of 18.21% in the time span of between FY15- FY19 and, therefore, it can be said that OVH is possessing decent capabilities to garner revenues, which might places it well to achieve long-term growth target. During the same time span, the company’s gross profit witnessed a CAGR growth of 17.61%. Between FY15- FY19, the company’s cash from operating activities have witnessed an improvement, which reflects that OVH’s operating capabilities have been improved. The cash receipts of OVH witnessed a CAGR growth of 21.58% between FY15- FY19 and, therefore, it can be said that the company has decent capabilities to build cash levels.

There are expectations that improvement in operational capabilities, revenue-generation abilities and capabilities to build cash levels might help the overall company to achieve long-term growth.

What to Expect from OVH Moving Forward: After simplification of the business model and sharpening of the focus on Fund Services as well as Platform Services businesses, Board and Management recognises that OVH needs to convert the streamlined operating business to strong growth, organically and by acquisitions. The key focus revolves around delivering high growth along with the margin uplift. The company has an intention to achieve this by concentrating towards the 4 key initiatives like driving automation and integration, continuing to innovate, increasing scale as well as building of the profile.

Considering the cash in bank, no debt as well as a business model, the company would be actively looking for growth opportunities, which accelerate scale and margin uplift. The company’s strategy revolves around high growth margin uplift and building brand awareness. OVH stated that both the business lines are having robust tailwinds and there is a robust pipeline of the potential new clients..png)

Key Valuation Metrics (Source: Thomson Reuters)

Valuation Methodologies:

Method 1: EV/Sales Multiple Approach.png)

EV/Sales Multiple Approach (Source: Thomson Reuters), *NTM: Next Twelve Months

Method 2: EV/EBITDA Multiple Approach.png)

EV/EBITDA Multiple Approach (Source: Thomson Reuters), *NTM: Next Twelve Months

Note: All forecasted figures and peers have been taken from Thomson Reuters

Stock Recommendation: The company’s stock has fallen 15.56% in the span of the previous three months, while in the time frame of the past six months, the stock declined 22.45%. As per ASX, the stock is trading towards its 52-week lower levels and, therefore, it can be said that OVH is offering decent opportunities for accumulation. The company has managed to deliver robust results in the year ended June 30, 2019, in the rapidly changing and challenging environment. The company’s total services revenues rose $12.9 million, and the figure stood at $49.6 million, reflecting a rise of 35% on the prior year. It was further added that robust organic growth of $6.5 million and acquisitions contributing $6.3 million were key drivers of growth. Moreover, the revenues were supported by quality of the recurring revenue.

The company stated that 2020 might witness the execution of its growth strategies i.e. automation and integration, innovation, increasing scale, and building brand awareness. OVH has the aim of increased scale benefits and margin expansion. Based on the foregoing, we have applied two relative valuation methods, i.e., EV/Sales and EV/EBITDA multiples and arrived at a target price upside of lower double-digit growth (in percentage terms). Hence, we give a “Buy” recommendation on the stock at the current market price of A$0.380 per share.

.png)

OVH Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...