Company Overview: OneVue Holdings Limited is engaged in providing outsourced superannuation administration, unit registry, and end-to-end superannuation services, including the provision of investment and portfolio administration, tax and reporting services. The Company's segments include Fund Services, Platform Services and Corporate. The Fund Services segment provides outsourced unit registry and installed software to a range of investment managers, custodians, trustees and superannuation administration. Its Platform Services segment offers services, including investment administration, tax and reporting services for both superannuation and other investments, a retail superannuation fund, self-managed superannuation fund (SMSF) compliance and administration services and investment management. It manages asset classes, including listed shares, term deposits, warrants, as well as personal assets and investments, including collectibles.

.png)

OVH Details

Decent Performance in 1H FY 2019: OneVue Holdings Limited (ASX: OVH) is an ASX listed fintech company that partners to disrupt the superannuation value chain. The company operates through two core business segments i.e., Fund Services, and Platform Services, which accounted revenue around 61% and 39%, respectively in 1HFY19 of total revenue. Recently, the company released its key business measure update for the quarter ended March 31, 2019 wherein fund numbers under Managed fund administration grew by 41% on Q-o-Q basis and 78% on PCP basis while FUA under Platform services grew by 7% on Q-o-Q basis and 15% on PCP basis and reached $4.7 billion. It had earlier released its half year results to December 2018 (1H FY 2019) in which its total revenues (including other income) witnessed a rise of $6.0 million and stood at $29.6 million, reflecting an increase of 26% over the prior corresponding period with organic growth of $4.4 million supplemented by growth from acquisitions of $4.9 million which offset revenues from the prior period divestments of $3.3 million. The company’s revenues from continuing operations encountered a rise of 31% as compared to the prior comparative period. OVH’s revenues have been supported by the quality of the recurring revenue which accounts for 91% of the total revenues. The Super member administration business which was acquired from KPMG has made the revenue contribution of $4.3 million. The company completed the strategic repositioning with the final divestment of Superannuation Trustee business and is focusing towards strong growth runways in the Fund Services and Platform Services. As presented in Sydney Investment Forum presentation, the company’s platform services revenue has witnessed a compound annual growth rate (CAGR) of 24.0% from 1H FY 2017 to 1H FY 2019 while fund services revenue encountered a CAGR of 30.5% during the same period which further builds the confidence in the company’s long-term growth. Furthermore, the macro industry trends are supporting the company’s growth momentum.

Going forward, the company is expected to be supported by favorable macro industry trends, decent current ratio and by lesser dependence on debt when it comes to funding assets as compared to broader industry (as evident from Assets/Equity ratio). Also, the unloading of Superannuation Trustee business wraps up the diversification program.

.png)

1H FY 2019 Half-Year Report (Source: Company Reports)

Superannuation Trustee Services Segment- Discontinued operation: In Superannuation Trustee Services, which is being now termed as a discontinued operation, Funds under trusteeship (FUT) as at March 31, 2019 amounted to $12.9 billion. FUT has grown by $1.1bn or 9.5% over the previous quarter. The release also mentioned about the sale of the Trustee Services business to Sargon and the parties have agreed to settlement date of on or before May 31, 2019.

Top 10 Shareholders: The following table gives a broad overview of the top 10 shareholders of OVH:

.png)

Top 10 Shareholders (Source: Thomson Reuters)

As can be seen from the above table, the first position has been secured by TIGA Trading Pty Ltd.

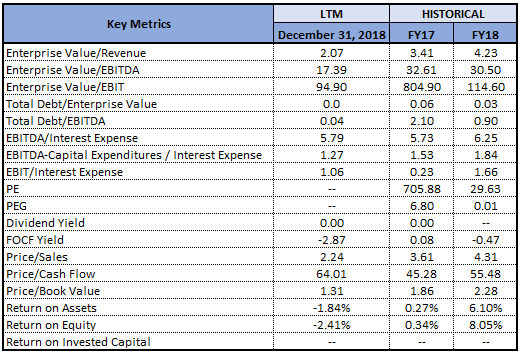

Decent Liquidity Levels Coupled With Rise in Assets/Equity Might Be Tailwinds: OneVue Holdings Limited is having the current ratio of 1.77x in 1H FY 2019 which implies a rise of 20.3% on the YoY basis reflecting that it’s liquidity standing has witnessed an improvement which might help it making further deployments towards its strategic business objectives. Also, the decent liquidity position might also help it achieving the long-term growth prospects. Additionally, the company’s Assets/Equity ratio stood at 1.38x in 1H FY 2019 which is lower than the industry median of 7.26x and, thus, it can be said that the company’s assets are primarily be funded by equity. However, it can also be assumed that the company is relying lesser on debt which might help it in meeting its broader business objectives. In 1H FY 2019, the company’s EBITDA margin stood at 8.7% which reflects a rise of 0.8% on the YoY basis.

.png)

Key Metrics (Source: Thomson Reuters)

Fund Services Revenue Witnessed 45% pcp Growth: OVH had stated that the Fund Services revenue witnessed a rise of $5.1 million or 45% over the prior corresponding period and there was robust growth from both Managed Fund Administration and Super Member Administration. However, it got offset by exited RE business. EBITDA of the business amounted to $3.1 million which implies a rise by $1.0 million from the prior corresponding period and the margins increased by 12 bps to 18.7% which reflects operating scale and leverage. With respect to the fund services, the primary growth drivers were a continuation of contracted transitions, securing of the new clients and integrating the KPMG Super acquisition. On December 21, 2018, the company made an announcement about the signing of new 3-year contract with Aon and Equity Trustees. The company’s Managed Fund Administration business witnessed a rise of 61% in the items processed, thus, bringing the number to 256,016. This increase was helped by a combination of new clients and continuing organic growth. Also, Super Member Administration administers 39 funds, with 152,493 members and the FUA (or Funds Under Administration) as at December 31, 2018 stood at $4.5 billion.

.png)

Fund Services (Source: Company Reports)

Gross Inflows and Net Inflows Were in Line with Historical Underlying Trend: With respect to Platform Services, OVH stated that structural disruption has been driving the momentum even though there were market declines in last quarter of 2018. There were gross inflows amounting to $0.6 billion while the net inflows amounted to $0.2 billion. The Platform Services FUA amounted to $4.39 billion which reflects a rise of 7% on the prior comparative period after adjusting the exit of SMSF Admin and Investment Management Businesses. The company entered into a binding agreement to unload its third-party Superannuation Trustee business to Sargon Capital Pty Limited which involved total consideration amounting to $45 million. The sale proceeds would be deployed towards capital management initiatives, which includes the payment of fully franked special dividend of 2.19 cents per share, a buy-back of up to 10% of capital, and financing growth opportunities.

.png)

Platform Services (Source: Company Reports)

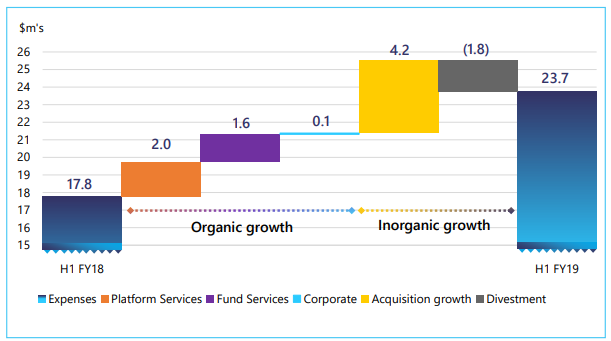

Operating Costs Witnessed $5.9 million Increase: In 1H FY19, OVH’s operating expenses amounted to A$23.7 million (continuing operations) which implies a rise of $5.9 million as compared to 1H FY 2018. This reflects $3.7 million from the organic growth, $4.2 million from the acquisitions while the divestments provided reduction in the costs amounting to $1.8 million. The company’s EBITDA from continuing operations witnessed a rise of 8% in 1H FY 2019 on YoY basis and there was underlying margin improvement in both the businesses – Fund Services (+12 bps) and Core Platform (+75bps).

Operating Costs Profile (Source: Company Reports)

What To Expect From OVH: OneVue Holdings Limited had stated that the macro industry trends are supporting the momentum and regulators, fund managers as well as investors are calling for the greater transparency of the costs and revenue drivers. Moreover, there has been increasing trend to outsourcing and new technologies are expected to improve the customer service levels, efficiencies as well as investor access.

With respect to Fund Services, the key revenue drivers are number/type of items processed, value-added services, number of funds, fund managers, and investors as well as number of members. While key profit drivers are average revenue per items processed, average revenue per member and scale benefits. For Platform Services, FUA bps and processing fees (fixed $ per activity) are the key revenue drivers and average bps of FUA margin as well as scale benefits are the key profit drivers.

The company focuses on strong growth runways in the Fund Services and Platform Services and it also possesses a strong pipeline of the new business opportunities.

Key Valuation Metrics (Source: Company Reports)

Valuation Methodologies:

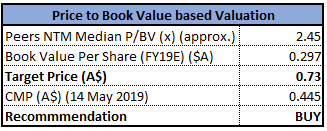

Method 1: Price to Book Value based Valuation

P/BV Based Valuation (Source: Thomson Reuters), *NTM-Next Twelve Months

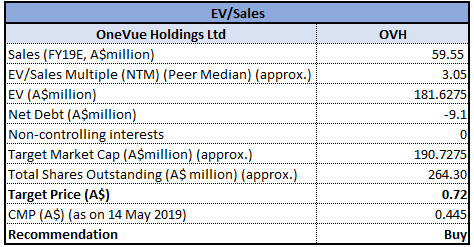

Method 2: EV/Sales Multiple Approach

EV/Sales Multiple Approach (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, *NTM-Next Twelve Months

Stock Recommendation: The stock of OneVue Holdings Limited is towards its 52-week lower levels and it had witnessed decent CAGR in Platform services revenue and Fund services revenue which might attract the attention of market players. The company’s top line has been witnessing favourable momentum in the past few years which reflects that it is having strong revenue generation capabilities. We expect that topline growth might be continued in the long run as it had witnessed a CAGR growth of 38.88% between FY 2014-FY 2018. Besides this, the company’s cash flow from operations has witnessed a significant improvement in the past few years (FY 2016-FY 2018) which implies that the company’s operational capabilities have been improving which can act as a tailwind for OVH moving forward. With respect to Platform Services, the transition of FUA of $500 million from two new white labels signed in the previous quarter is expected to complete in the next quarter. Coming to the returns posted on ASX, the stock of OVH has delivered the return of -24.79% in the span of previous six months while, in the time frame of past three months, the returns were -24.14%. By looking at decent outlook in the long-run on the back of its strategic approach towards topline and bottom growth with the vision of wealth building for investors, we have valued the stock using two Relative valuation methods, Price/Book Value ratio, and EV/Sales multiple and arrived at a double-digit upside growth in the next 12-24 months. Based on the foregoing, we give a “Speculative Buy” recommendation on the stock at the current market price of A$0.445 per share (up 1.136% on 14 May 2019).

.png)

OVH Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...