Company Overview - OneVue Holdings Limited is engaged in providing outsourced superannuation administration, unit registry and responsible entity services, and end-to-end superannuation services, including the provision of investment and portfolio administration, tax and reporting services. The Company's segments include Fund Services, Platform Services and Corporate. The Fund Services segment provides outsourced unit registry and installed software to a range of investment managers, custodians, trustees, responsibility entity services and superannuation administration. Its Platform Services segment offers services, including investment administration, tax and reporting services for both superannuation and other investments, a retail superannuation fund, self-managed superannuation fund (SMSF) compliance and administration services and investment management. It manages asset classes, including listed shares, term deposits, warrants, as well as personal assets and investments, including collectibles.

.PNG)

OVH Details

March quarter performance with positive operating cash flow: OneVue Holdings Limited (ASX: OVH) has achieved the full run rate of cost saving synergies of $4 million per annum from the acquired Diversa business, which is well ahead of schedule, in the March quarter of 2017. For the Unit Registry segment, the funds under administration (FUA) of $465.4 billion at the end of the quarter were up $30 billion on the previous quarter and up $63 billion on the prior corresponding quarter (pcp). The company has processed items growth of 24% in the quarter on the previous quarter and 47% on pcp. The unit registry team had added 56 new funds in the March quarter and two new fund managers. The new funds added in the last twelve months totaled 149 and OVH is now administering 589 funds on behalf of 36 fund managers. For the Superannuation Services segment, the FUA at March 31, 2017 reached $1.8 billion, which is an increase of 4.6% ($79 million) on the previous quarter, with growth on pcp of 66% ($716 million). The superannuation services now administer 23 funds with over 90,000 members. The member numbers were in line with the prior quarter but are up 168% on pcp. The Platform Services segment also witnessed a growth of 24% as the FUA grew to $3.9b at 31 March 2017 ($749 million) on pcp. The gross quarterly inflows from new and existing clients were of $249 million, which is a growth of 46% on pcp, continuing the strong recent momentum and taking inflows to $1.1 billion for the last 12 months. The net inflows for the quarter of $103 million were down on the previous record quarter but in line with pcp. Additionally, for the Superannuation Trustee Services segment, the funds under trusteeship (FUT) has increased by $554 million for the quarter driven by growth in assets of existing clients. FUT at 31 March 2017 closed at $9.4 billion and the funds have grown by $2.2 billion or 31% over pcp. As per the cash flows highlights, net cash from operating activities reached $0.29 million in March quarter and $1.459 million in this year to date. Net cash used in investing activities reached $2.409 million during the quarter and $4.047 million in this year to date. Cash flows from financing activities reached $2.345 million during the quarter.

.png)

March 2017 Quarterly key measures update (Source: Company Reports)

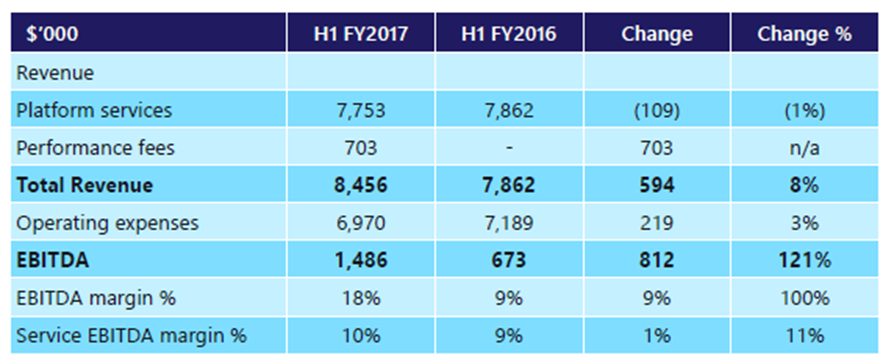

Strong 1H FY 17 Financial Performance:The group also delivered a solid performance in the first half of FY 17, reporting a 50% growth in the total revenue over the prior corresponding period (pcp) by $6.1 million to $18.5 million. The revenue grew due to the high levels of the recurring revenue. The recurring revenues now represent 92% of revenues, up from 89%. The revenue growth has been 77% CAGR from FY13 to FY16 and 50% for the first half of FY17. The operating expenses increased by 33% over pcp to $17.5 million, mainly due to the acquisitions and ongoing investment in growth. The EBITDA increased by $1.8 million to $0.9 million, which is a 212% improvement on pcp. EBITDA turnaround reflected the earning momentum of the business. The EBITDA margin expanded to 5%. Therefore, the NPAT grew by $2.4 million to $0.3 million, which is a 117% improvement on the pcp. Further, the realisation of Diversa synergies continued to track ahead of schedule with the full impact expected in Q4.

.png)

1H FY 17 Financial Performance (Source: Company Reports)

Fund Services Segment Performance in 1H 2017: The Unit Registry grew due to the transitions from the existing custodial relationships, onboarding new fund managers, and increased transaction volumes. Improving average revenue per member, type and number of transactions processed and size of assets in the superannuation fund also contributed to the performance. The New Super Services clients were secured and benefits of OVSS and Diversa Super acquisitions (3 months from October 2016) also added to the positive momentum. The strong acquisition and organic revenue growth has driven the margin improvement.There is an increasing momentum in the segment due to the transitions and automation initiatives. The group intends to maintain an EBITDA margin of 20%.

.png)

Fund Services Segment Performance in 1H 2017 (Source: Company Reports)

Superannuation Trustee Services Segment Performance in 1H 2017:The segment grew in the first half due to the benefits of synergies realized by the acquisition of Diversa, which is number one in scale in outsourced superannuation trustee services in the Australia market. This service comprises several specialist governance and compliance functions performed by trustees in the highly-regulated superannuation industry, which includes managing superannuation funds in accordance with their trust deed and regulatory obligations. Accordingly, the revenues continue to grow due to the retail superannuation client growth. Funds under Trusteeship reached $8.9 billion and rose $443 million post acquisition. The group also indicated to maintain an EBITDA margin of 35% to 40% range.

.png)

Superannuation Trustee Services Segment with growing target industry drivers (Source: Company Reports)

Platform Services Segment Performance in 1H 2017:The positive impact of the record gross inflows was reduced by MAP member fee reduction and one off loss of investment management client loss. The disciplined cost management has helped to underpin margin performance and the margin increased with operating leverage and performance fee benefits. The group intends to gain more business via their unique strategy of being the only platform with a strategy to counter traditional platforms, offer managed accounts and extend the current platform clients base into new client segments.

Platform Services Segment Performance in 1H 2017 (Source: Company Reports)

Outlook for the next few months: OVH’s focus for the near term has been indicated to extract the full synergies from the Diversa acquisition. OVH will be continuing to execute the Unit Registry transitions, raising the profile of the FUND.eXchange and continuing to evaluate strategically aligned earnings accretive transactions. Moreover, OVH will focus on the client retention and securing new clients. OVH will be further delivering operating leverage through scale and automation, as well as, ongoing disciplines. With regards to the industry drivers’ front, the Australian superannuation sector has been delivering a solid performance, and this trend is expected to continue in the coming years. The superannuation sector generated a CAGR of 10.1% from FY04 to FY15, and is expected to generate a CAGR of over 6.6% from FY18 to FY21.

Stock Performance:OVH stock sentiment has recovered with the stock rising over 12.3% in the last four weeks (as of May 15, 2017) post the volatility witnessed against performance in the last six months. Favorable industry drivers coupled with strong performance of the group have now contributed to the bullish sentiment. The group has been delivering a better performance than the overall sector, with revenues growing at a CAGR of 77% since FY13 and FY16. OVH client base is also diversified while top 10 clients accounting for 36% of total revenue while the largest client contributes 7% of total revenue. The group’s recurring revenue is also improving which now contributes 92% of their total revenues. OVH is pursing both organic and acquisitive opportunities as the company’s business has turned into a profitable business. OVH has huge transition pipeline and strong market opportunity which could drive the stock further. We give a “Buy” recommendation on the stock at the current price of $ 0.59

.PNG)

OVH Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...