Company Overview: OncoSil Medical Limited is a late-stage medical device company, which is focused on localized treatments for patients with pancreatic and liver cancer. The Company is engaged in the development of its lead product candidate, the OncoSil localized radiation therapy, for the treatment of pancreatic cancer. The Company's lead product, OncoSil, is a brachytherapy device that emits beta radiation and is implanted directly inside the cancerous tumor. OncoSil is a silicon and phosphorus (p32) beta emitter, able to be implanted intra-tumorally via endoscopic ultrasonography in localized solid tumors of patients with pancreatic cancer. The Company focuses on an application for Conformite Europeene (CE) Mark to enable commercial sales of OncoSil in the European Union and an application for an Investigational Device Exemption (IDE) from the United States Food and Drug Administration (FDA) to enable commencement of the United States pivotal clinical study, known as OncoPac-1.

.png)

OSL Details

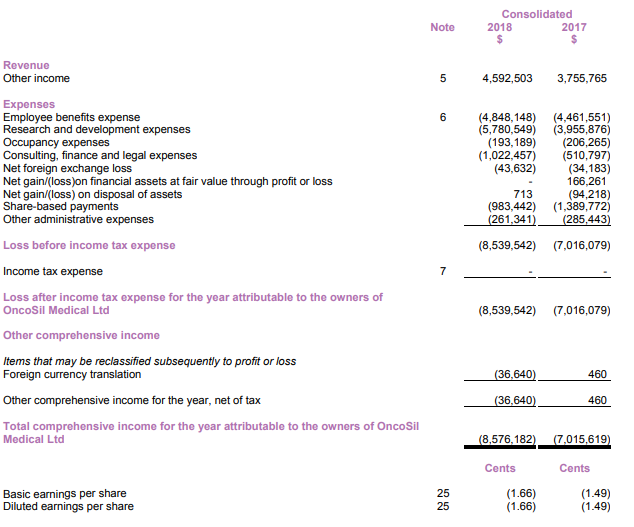

Robust Progress Made in FY 2018: OncoSil Medical Ltd (OSL) happens to be a medical device company which has maintained its focus on Interventional Oncology in the pancreas as well as liver; and is having a market capitalization of $107.22 million (as on February 15, 2019). The company witnessed significant progress lately, and it had maintained its focus towards the advancement of OSL’s Global Pancreatic Clinical Study Programme so that required supplemental performance as well as safety data which is needed to support the CE Mark application and future commercialization of OncoSil™ device can be generated and submitted. The company managed to successfully wrap up the patient recruitment for the PanCO study throughout the participating sites in Australia, United Kingdom as well as Belgium and has enrolled 50 patients. The company’s annual report for 2018 demonstrated that out of these 50 patients, the OncoSil™ device has been implanted in 42 patients and six patients have undergone surgical resection with the curative intent following re-staging of their tumours. The company’s other income has witnessed a rise from A$3,755,765 in FY 2017 to A$4,592,503 in FY 2018. Talking about margins, the company’s key margins have witnessed an improvement in FY 2018 on the YoY basis, further building the confidence in the future performance. In FY 2018, the company’s net margins improved 0.9% YoY to -185.9% which implies an improvement in the capability to convert the top line into the bottom line. Moreover, the company’s EBITDA margin encountered 2.9% YoY improvement in FY 2018 to -184.1%.

FY18 P&L Statement (Source: Company Reports)

Strong Liquidity Position Making Headroom for Further Growth Prospects: OncoSil Medical had wrapped up an oversubscribed institutional placement in the month of March 2018 which was aided by major existing shareholders along with the numerous new institutional investors and, as a result, the company raised approximately $12.7 million. OncoSil Medical had also wrapped up its share purchase plan in the month of April 2018 with existing shareholders to garner an additional $4.0 million.

The company’s strong liquidity position is reflected in its FY 2018 current ratio which has significantly improved by 63.7% YoY and stood at 11.46x implying an improvement in the liquidity position and, thus, placing it in a robust position to satisfy the short-term commitments.

OSL Received R&D Tax Incentive Refund: OncoSil Medical Limited had got the cash refund amounting to $4.3 million which was from Australian Taxation Office following lodgement of 2017/18 financial year tax return. The cash rebate is associated with expenditure on eligible Australian as well as international R&D activities which was done during 2017/18 financial year. There are expectations that ongoing research and development activities which include the components of global pancreatic clinical study programme (PanCO & OncoPaC-1 studies) would be remaining eligible for the R&D tax incentive scheme.

Progress Made in December 2018 Quarter: The Chief Executive Director of OncoSil Limited named Mr. Daniel Kenny had stated that they reached a crucial milestone in the United States now that FDA had confirmed that data from non-US PanCO clinical study happens to satisfy safety requirements to proceed to full pivotal study in the United States under IDE or Investigational Device Exemption. Mr. Kenny also added that CE Marking review is undergoing in Europe and it also added that it is complex and challenging and it would be taking time to conclude. As per the December 2018 Quarter release, the company had also wrapped up the patient recruitment for US OncoPaC-1 clinical study and nine patients have been enrolled and OncoSil™ device has been implanted in all these patients.

Mr. Kenny had also added that the British Standard Institute (BSI) had confirmed that CE Marking happens to be in the final phase of the review assessment and that there are expectations of a positive recommendation. The company was possessing the cash balance amounting to $13 million at the end of December 2018.

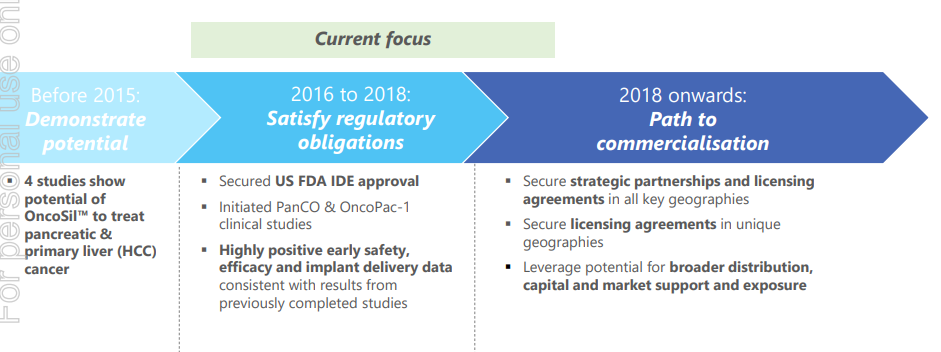

OSL Reached Potential Value Inflection Point: The annual general meeting presentation had demonstrated that OncoSil Medical happens to be at a potential value inflection point and it is at the robust position to realize the OncoSil™ device’s value. The company stated that between 2016-2018, the company had maintained its primary focus towards the satisfaction of the regulatory obligations. Moving forward from 2018, they would be on the path of commercialization. OncoSil Limited would now be focusing on securing the strategic partnerships as well as licensing agreements in all key geographies. Moreover, the company would be leveraging the potential for broader distribution, capital and market support as well as exposure.

Path to Commercialisation (Source: Company Reports)

Positive Results from OSL’s PanCO Study: In the release dated October 25, 2018, OncoSil Limited’s Chief Executive Director named Mr. Daniel Kenny had stated that the results from PanCO study Interim Analysis are positive and the analysis reflects clinically relevant as well as statistically significant results in numerous important clinical endpoints. He also added that resection data happens to be suggestive of the potential to “convert” the selected patients from initially inoperable status to surgically resectable as well as potentially curative state. This happens when OncoSil™ is utilized along with chemotherapy.

The finding happens to be supportive of future studies of OncoSil™ device as part of a neoadjuvant treatment strategy in resectable and/or borderline pancreatic cancer. The release highlighted that one of the key findings from Interim Analysis happens to be of Local Disease Control Rate (or DCR) which is of 88% at Week 16 in Per Protocol (implanted) population.

Key Updates About OSL: In November 2018, OSL had made an announcement that in accordance to ASX Listing Rule 3.10A, 1,538,462 loan shares which were subject to the voluntary escrow entered into by the employees under the Employee Loan Share Plan, have been released from escrow on November 19, 2018. Also, earlier, the company had made an announcement related to the appointment of Mr. Michael Bassett as the Non-Executive Director. He happens to have more than 25 years of experience when it comes to capital markets, and he has also been on senior management roles at Australia’s leading fund management as well as investment banking firms.

Drivers for Future: As demonstrated in AGM presentation, OncoSil Medical happens to have a clear strategic path, and there are expectations that the company would be aided by the experienced management team as well as strong clinical and commercial pedigree. The company happens to be at the potential value inflection point, and there are multiple paths to commercialization. Moreover, moving forward, there are expectations that the company would work towards securing the strategic partnerships as well as licensing agreements with regards to all the key geographies as well as towards securing the licensing agreements in unique geographies. This could act a catalyst for the company going forward.

The company is in a strong position for the commercialization which is backed by a broad technology platform, healthy clinical results, EU regulatory approval as well as significant unmet clinical need. There happens to be a global commercial opportunity of more than $2 billion, and there are 130,000 cases p.a. in the US and EU alone. Also, over 70,000 of these might be benefited from OncoSil. The company’s potential pricing amounting to US$25,000 per patient reflects more than $2 billion global market opportunity. Moreover, the sector has also encountered mergers and acquisitions (or M&A), and the company stated that there were more than A$2 billion of acquisitions in February 2018. The global pharmaceutical players are being attracted towards early-stage Australian biotech.

Stock Recommendation: In the last one year, the stock has risen 30.77% but is trading well above its 52-week low level of $0.115, and still signifies an attractive opportunity for the investors to acquire the stock at the current juncture. A technical indicator, Exponential Moving Average or EMA has been applied on the daily chart of OncoSil Limited and default values were used for the purposes. After careful observation, it was noticed that the stock price has crossed the EMA and had trended upwards after the crossover signifying the bullishness. As a result, there are expectations that the company’s stock might witness a rise moving forward.

Fundamentally, the company is expected to be largely benefited by its strong position from the commercialization point of view, multiple paths which it has towards commercialization, and with the help of a strong management team. Also, BSI had made a confirmation that CE Marking is in the final phase of review and the company might witness positive recommendation which could drive growth moving forward. Another factor which could support OncoSil Medical is its robust liquidity position which provides headroom for further growth prospects and to meet the short-term obligations. Amidst all these growth-driving factors, the company is exposed to certain financial risks like market risk as well as credit risk. The company’s stock has delivered the return of -8.11% in the span of past 6 months and, in the time frame of the previous three months, the stock’s return was -5.56%. Given the backdrop of aforesaid facts and current trading level, we give a “Speculative Buy” recommendation on the company’s stock at the current market price of A$0.170 per share.

.png)

OSL Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...