Company Overview: OncoSil Medical Ltd (ASX: OSL), formerly known as NeuroDiscovery Ltd, is a medical device company, which focuses on the development of brachytherapy for the treatment of pancreatic and liver cancers in Australia. The headquarter of the company is situated in North Sydney, Australia and the group is being currently headed by Mr. Daniel Kenny – Chief Executive Officer and Managing Director. It offers various treatment options for patients with pancreatic cancer including surgery, external radiation therapy, chemotherapy, and chemo-radiation therapy. Its lead product includes OncoSil, a brachytherapy device that emits beta radiation and is implanted directly inside the cancerous tumor during an endoscopic ultrasound guidance procedure. It is progressing towards the commercialization of the product. The device is currently undergoing clinical studies in leading academic sites globally. The clinical data will be used for regulatory submission within targeted markets including Europe, the United States, Australia, and Asia.

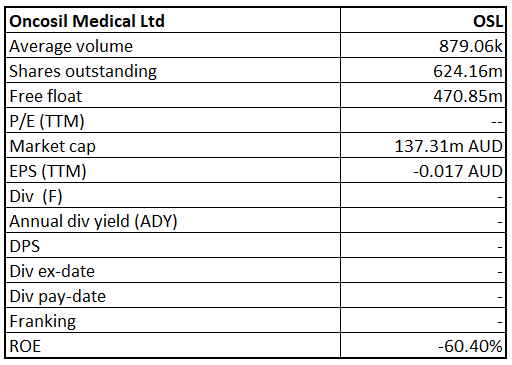

OSL Detail

Huge opportunity starting with the appointment of IQVIA: OncoSil Medical Ltd (ASX: OSL) has recently appointed IQVIA as its Market Access and Reimbursement advisor for the OncoSil devices in European markets including France, UK, Germany, and the Nordic countries. IQVIA is an NYSE-listed global leading provider of advanced analytics, technology solutions, and contract research services to the life sciences industry. The appointment of IQVIA represents a significant milestone for the Company commercialization strategy. As per the agreement, IQVIA will work in collaboration with the Company to develop a strategic and effective approach to commercialization of the OncoSil device in key EU Markets. Moreover, IQVIA will support the company to undertake detailed feasibility assessments, pathway specifications, and market penetration activities in the lead up to OncoSil Medical receiving CE Mark Certification and first commercial use of the OncoSil device in patients. Hence, we expect that this appointment will provide a huge opportunity in the Company’s commercialization strategy in anticipation of securing CE Mark approval and moving into the early commercialization of its device over the coming months.

.png)

Commercial Journey of the Group (Source: Company Reports)

Clinical – progress with patient recruitment and encouraging study data: In July 2018, the group successfully completed patient recruitment for its PanCO study across all participating sites in Australia, UK, and Belgium with 50 patients. Of these 50 patients, 41 patients were successfully implanted with the OncoSil device and found excellent Local Disease Control Rate (DCR) of 100% for Week 8 and 87% for Week 16. It demonstrates the future trials wherein the company will be able to explore its clinical study options in resectable, borderline resectable and locally advanced pancreatic cancer indications. However, DCR is not a formal endpoint of the PanCO or OncoPac-1 studies but it is a widely reported statistic in the pancreatic cancer literature. Additionally, 6 patients have effectively experienced surgical resection with the medicinal intent, showing the capacity of the OncoSil device, in combination with chemotherapy to take patients from an inoperable to an operable state. It exhibits significant opportunity for OncoSil to become standard of care in a combination of Chemotherapy. Other than this, 9 patients achieved a Partial Response of defined as a reduction in a tumor longest diameter of at least 30% from the baseline. Based on aforesaid facts, we expect that the group has immense opportunity in years to come because of receiving a positive outcome from its PanCO clinical trial which suggested that the medical device product OncoSil is safe, secure and can be deployed through endoscope without inconveniences and can reduce tumor ailment when combined with chemotherapy.

.png)

Substantial tumour volumetric reduction (Source: Company Reports)

Strategic partnership and license agreement will support organic and inorganic growth: At present, the group focuses on to securing its strategic partnerships and licensing agreements with 15 leading cancer centres in all key geographies. In our view, this strategic partnership bodes well for the company as it would enable infusion for the commercialization of its products in the selected countries. Hence, we expect that this strategic partnership will provide the long-term growth path in the key geographies areas i.e., EU and US; and unique geographies such as China, Japan, and India.

.png)

Partnering with leading cancer centres (Source: Company Reports)

Highly Experienced Team: The company has a highly skilled executive management team with deep understanding of biopharma sector. The members of its senior management team have over 20 years of experience in the global drug and device development field and possess an in-depth understanding of the specific industry, products and geographic regions they cover, which we believe enables them to support and provide guidance to its employees and grow its business. Currently, the group is headed by Mr. Daniel Kenny – current CEO & Managing Director. He has a sound track record to work in Global Pharmaceutical and Medical Device sector and has proven to be a key contributor to drive the business of various industry leaders such as Roche, Allergan and Baxter. Hence, we expect that the team will continue to work towards refining the manufacturing and supply chain processes to prepare for commercial and clinical needs. This includes having hot calibration runs with key trial centres and hospitals.

.png)

Highly experienced management team (Source: Company Reports)

Decent performance in FY18 will support execution of Business Objectives: The Company completed several milestones during FY18 that include successfully completion of recruitment for its PanCO study globally, submitted a detailed clinical report on the required safety and performance data for the OncoSil device to the British Standards Institute (BSI), and fulfilled BSI’s supplemental data request with respect to our CE Mark application. The company for FY18 reported a 22.3% growth in revenues from ordinary activities to $ 4,592,503. However, loss for the Group after providing for income tax increased by 21.7% and amounted to $ 8,539,542 in FY 18 over the prior year. It was mainly impacted by higher R&D expenses and foreign exchange loss during the period. Cash and financial assets balance as at 30 June 2018 was $15.2 million and the group received R & D Tax Refund of $4.4 million for FY18 (2017: $3.4 million). Early positive study data results have been consistent with previously completed studies. In March 2018, the company raised $ 12.7 Mn through institutional placement. The main objective of this fund is to spend for completing the preliminary phases of its PanCO and OncoPac-1 trials, support European commercialization and commence a global, registration-directed randomized controlled trial under an Investigational Device Exemption from US FDA, and other business developments such as innovation, licenses, etc. As of 30 June 2018, the company has a decent cash position with zero debt facility. The current ratio stood at 11.46x in FY18, representing adequate liquidity to fulfill any shortcoming liability in near future. No dividends were proposed or paid during the period.

.png)

FY18 – Consolidated Profit and Loss Statement (Source: Company Reports)

Positive Outlook: In our view, the company has a lot of potential to grow further at the back of decent cash position with nil debt facility, strong partnership with 15 leading cancer centres around the globe and positive results received to date of its clinical trials for the treatment of advanced pancreatic cancer. Hence, we expect that the Company will be able to commercialize its medical devices into the targeted market over the next 12 months.

.png)

Clinical pathway overview and outlook (Source: Company Reports)

Stock Performance: The stock has generated returns of 62.96% in last six months and is poised to move higher from the current levels. After correcting from the recent highs of $0.245 and taking support at the crucial level of $0.165, the stock has staged a sharp V-shaped recovery. The level of $0.220 may form a resistance level for the stock and breakout may take the price higher again. At the current juncture, major technical indicators such as relative strength indicator is not showing any sign of significant weakness in the price. Further, the stock is trading above its short-term moving average indicating chances of an upside. Given the backdrop of aforesaid facts along with financial performance and its capital position, the stock has room to grow from the current levels and therefore we give a “Speculative Buy” recommendation on the stock at the current market price of $ 0.220.

.png)

OSL Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...