Company Overview: Oliver's Real Food Limited is engaged in operating a organic fast food chain stores in Australia. The Company offers a range of products, including gourmet pita pockets, sushi, salads, sandwiches, organic soups and curries, gluten free and low fat muffins, fruit salad, dairy and coconut yoghurt cups, organic muesli, organic chia pods. It also offers organic drinks, organic free-trade coffee, alkaline water, organic nuts, chips and popcorn freshly squeezed juices and smoothies, organic coffee, and tea, protein bars, energy balls, organic green and edamame beans served with Himalayan salt, health and wellbeing books, CDs and DVDs. The Company operates its stores in over 20 locations along the arterial highways of Australia’s eastern seaboard, principally New South Wales and Victoria.

.png)

OLI Details

Decent Cash Receipts Scenario: Oliver’s Real Food Limited (ASX: OLI) happens to be an ASX listed company whose principal continuing activities revolve around the management of Quick Service Restaurants (or QSR) in Australia under the branding of “Oliver’s Real Food”. As on July 5, 2019, the market capitalisation of the company stood at ~A$11.78 million. The company had earlier released its results for the quarter ended March 2019 in which its Chairman Nicholas Dower stated that, in the short time, the current Board of Directors and the new executive team have been in place, and they have achieved a significant reduction in the cash burn from January to March. The company is optimistic about the initiatives which have been implemented by the new CEO and his team in order to significantly reduce the overheads and improve the store performance, and they are confident that they would be able to deliver the better news to the shareholders moving forward. The company’s key personnel also stated that they have focused the initial efforts on stabilizing the business by cutting the increased levels of the unnecessary spending and getting focused towards delivering the great experience for the customers, mainly by rebuilding team culture. It had been reflected in better customer experience as well as improved store performance.

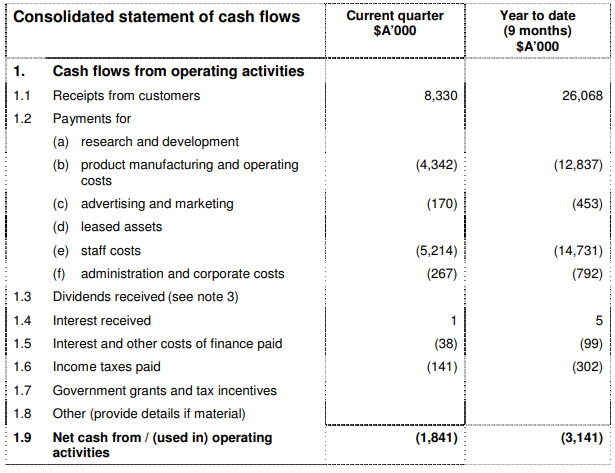

Net Cash Used in Operating Activities (Source: Company Reports)

The company’s cash receipts have been growing at the respectable levels from the past few years as they have witnessed a CAGR growth of 40.03% in the time span of FY 2016-FY 2018) and, thus, it looks like that the company, moving forward, could be able to witness respectable cash receipts to support the growth. The company’s net cash used in operating activities stood at $1.84 million and its receipts from the customers amounted to $8.33 million.

The company has closed several stores and they have dealt with the possible liabilities they represented. The reduced overhead as well as improved trading results would be ensuring that the company’s cash position would not be requiring any additional funding for foreseeable future.

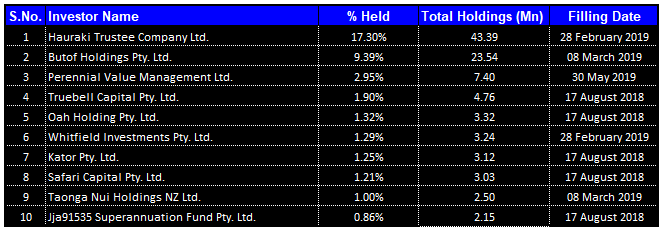

Top 10 Shareholders: The following table gives a broad overview of the top 10 shareholders of Oliver’s Real Food Limited:

Top 10 Shareholders (Source: Company Reports)

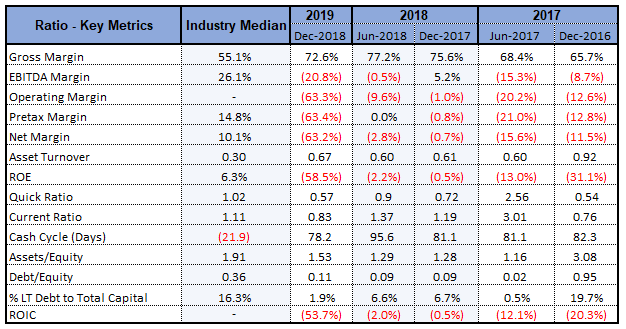

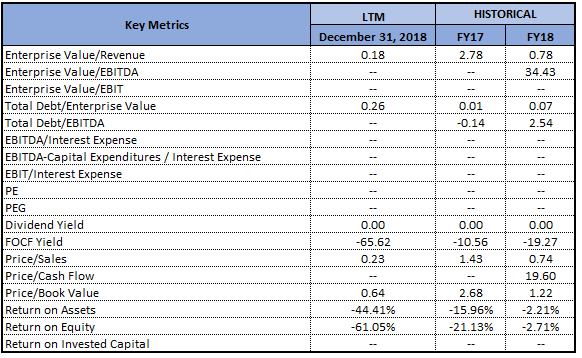

Overview of Key Financial Ratios: Oliver’s Real Food Limited is having a respectable position with respect to its key financial ratios as its gross margin stood at 72.6% in 1H FY 2019, which is higher than the industry median of 55.1%. In FY 2018, its EBITDA margin stood at 2.3%, which implies a rise of 14.7% on the YoY basis.

Key Metrics (Source: Thomson Reuters)

Coming to the leverage ratios, the company’s Debt/Equity ratio stood at 0.11x in 1H FY 2019, which is lower than the industry median of 0.36x and, thus, it looks that the company has a deleveraged balance sheet as compared to the broader industry median. The company’s long-term debt as a percentage to the total capital stood at 1.9%, which implies a fall of 4.8% on the YoY basis and, therefore, it can be said that the company has been reducing its exposure to long-term debt with respect to the total capital. The reduction of the debt levels might help it in stabilizing its balance sheet moving forward and, thus, placing it well to achieve long-term growth.

Appointment of CFO: Oliver’s Real Food had earlier made an announcement about the appointment of David McMahon as the permanent CFO of the company. David happens to be a qualified accountant, and his experience spans over 30 years in the various senior financial roles, which includes Woolworths, Atlantic Pacific Foods, Global Procurement Services and Transfield Constructions.

Announcement About Subsidiary Liquidations: As per the release dated March 13, 2019, the Board had advised that it had finalized the liquidation of the 4 subsidiaries, each of whom housed Oliver’s trading store which had been previously closed. The release stated that the subsidiaries that have been placed into voluntary liquidation are Oliver’s Horsham Pty Ltd, Oliver’s Dubbo West Pty Ltd, Oliver’s Albury North Pty Ltd, and Oliver’s Coomera Pty Ltd. The company stated that the store closures and the subsequent liquidations happen to be part of the ongoing commitment of the new Board to return OLI to profitability. The result of the liquidations would be to stem unnecessary cash outflows as well as eliminate the contingent liabilities which would otherwise continue draining the ongoing operations.

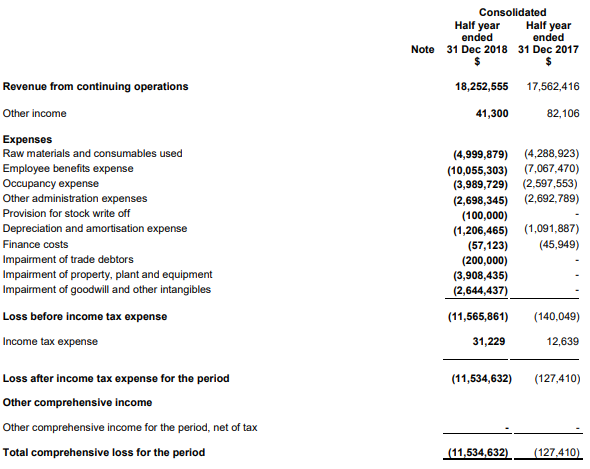

OLI Witnessed A Rise in Revenue in 1H FY 2019: Oliver’s Real Food Limited had already released its results for the half-year ended December 2018 in which its revenue amounted to $18.3 million, which implies a rise of 3.9% from $17.6 million in the half year to December 2017. The company stated that earnings before depreciation, amortisation, interest, tax and impairments (or EBITDAI) were a loss of $3,553,042. The loss for the consolidated entity after providing for income tax and impairments stood at $11,534,632 as compared to December 31, 2017 loss of $127,410.

Statement of Profit or Loss and Other Comprehensive Income (Source: Company Reports)

Oliver’s Real Food Limited operated a total of 28 company-owned quick service restaurants throughout the half-year. The company stated that the sales revenue, though marginally higher than the previous year, was lower than the company’s internal forecast. Also, EBITDA was short of the forecast. The shortfalls with regards to both Revenue and EBITDA are attributed to several factors. The primary factors include the following:

(a) Weakness in the retail spending generally in the Christmas and holiday period, with trading in Oliver’s stores not as strong as was anticipated.

(b) Roadworks diversions at the flagship stores which negatively impacted the performance in the key stores, especially in peak trading period.

(c) Bringing forward the planned refurbishment of the flagship store at Wyong, which resulted in the reduced trading for the 12 days period in December.

What To Expect From OLI: In the release dated May 29, 2019, Oliver’s Real Food Limited reported its third quarter (January to March 2019) results wherein it incurred a trading loss amounting to around $1.8 million. The Board had informed the stakeholders that remedial actions which have taken have had desired impact as the anticipated trading position for quarter April-June 2019 is anticipated to be a breakeven, which happens to be a significant turnaround, and which has eliminated the cash burn. Additionally, this position forms a solid foundation for the future and a return to the profits.

The company stated that it would post a trading loss for the 2019 financial year amounting to approximately $5.3 million, all of it incurred prior to the actions as well as initiatives of the current Board and new senior management team. The Board is confident, and they have addressed major issues, and it stated that they have a sound platform now from which to work, with positive cash flows anticipated for the balance of this year. The Board is of the view that the 2020 financial year would witness a return to the profits and with it the ability to pursue numerous exciting and potentially viable opportunities.

Key Valuation Metrics (Source: Thomson Reuters)

Stock Recommendation: In the letter to shareholders dated May 29, 2019, the company stated that even though a 2019 financial year loss of $5.3 million is hardly a good result, it is better than it would have been under control of the old Board and Management. The company also added that the speed of current improvements happens to be a credit to the new team and a result of very long days as well as seven-day weeks. Considering that most of the major cost-cutting and savings are now factored, the total attention is focused towards the improved store performance and better margins.

From the analysis standpoint, it can be said that the company is possessing decent revenue-generation capabilities which are evident from its top-line CAGR growth of 41.26% in the time frame of FY 2015- FY 2018 which might help it achieving the long-term growth and can also help it in gaining traction among the market participants. Also, the company is possessing remarkable operational capabilities as can be seen from the CAGR growth of 95.74% in its cash from operating activities. We expect that the company’s revenue generation and operational capabilities place it well to achieve respectable growth moving forward. Also, considering the company’s major cost-cutting and savings initiatives and its focus towards improved store performance and better margins, we presume that the company has potential to grow further.

Coming to the company’s stock performance, it has posted the return of -47.78% in the span of previous six months while, in the time frame of past three months, the returns stood at 74.07%, which reflects that the stock is quite volatile. It is presently trading below the average of 52 weeks high and low levels of $0.09. Hence, in the view of aforesaid facts and current trading level, we give a “Speculative Buy” recommendation on the stock at the current market price of A$0.047 per share.

OLI Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...