Company Overview - Oil Search Limited is engaged in the exploration, development and production of oil and gas fields. The Company's main asset is its 29% interest in the PNG LNG Project, a liquefied natural gas (LNG) development operated by ExxonMobil PNG Limited. Its segments include PNG oil and gas, PNG LNG Project, Middle East and North Africa (MENA) oil and gas, and Other. In addition to the PNG LNG Project, the Company has interests in, and operates all of, PNG's producing oil fields. Approximately 20% of PNG LNG Project gas is sourced from its operated oil fields. It also has exploration interests in the Middle East and North Africa, focused on oil opportunities. The Kutubu and Moran fields are key producers for the Company, contributing more than 90% of the Company's total oil production, as of December 31, 2014. The Company has drilled 59 wells.

.png)

OSH Details

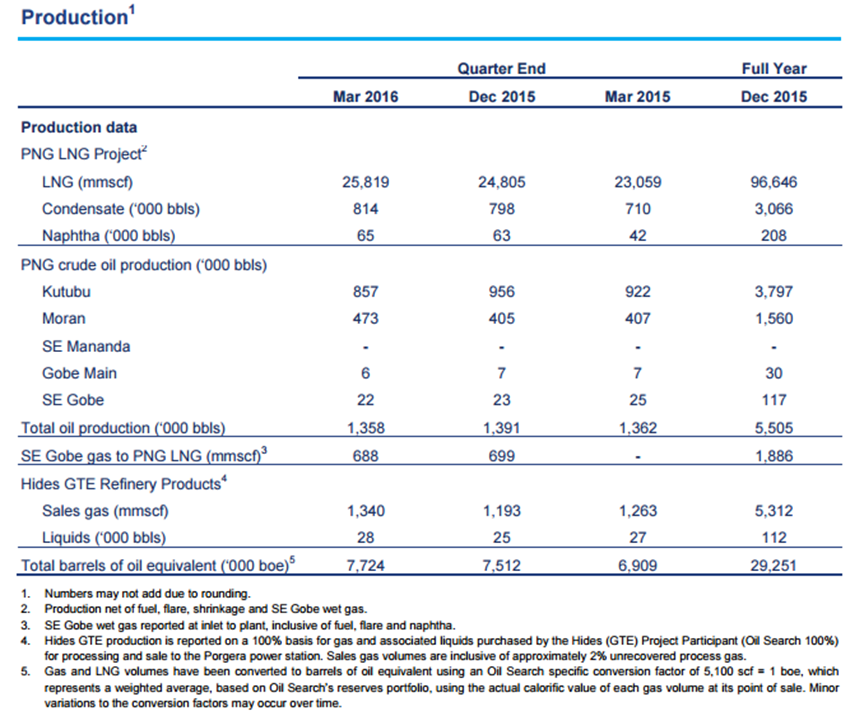

Rising production partly offset revenue pressure: Oil Search Limited (ASX: OSH) reported a rise in production by 3% to 7.72 mmboe during the first quarter of 2016 as against 7.51 mmboe in fourth quarter of 2015. Total sales increased by 13% from 7.08 mmboe in prior quarter to 7.97 mmboe. For the PNG LNG Project, the group delivered an annual production of 8 MTPA (which is 16% above nameplate) during the first quarter of 2016, indicating better levels of facilities uptime. Meanwhile, the Production net to Oil Search from the PNG LNG Project reached 5.94 mmboe (25.8 bcf of LNG and 0.88 mmbbl of liquids). On the other hand, the revenues plunged over 9% on a yoy basis to $313.1 million due to pressure from average realized LNG as well as oil prices pressure. The LNG and gas sales rose by 18% while liquids sales improved by 2%. However, the fall of average realized LNG and gas price to US$6.84 per mmBtu and the average realized oil to US$34.76 per barrel posed pressure to the revenues.

March quarter performance highlights (Source: Company Reports)

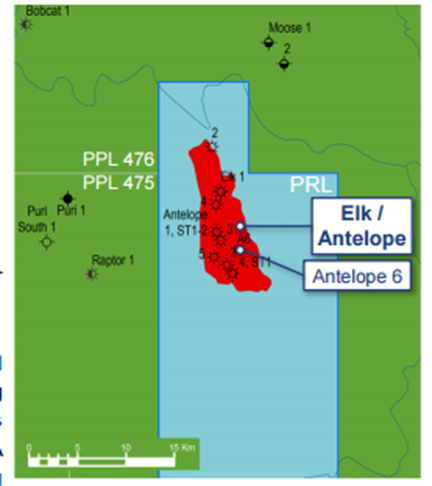

Positive exploration highlights: The group’s testing of the Antelope 5 and Antelope 6 appraisal wells was finished indicating solid reservoir quality and connectivity in the main, crestal area during the March quarter. Recently, the group updated that its Antelope 6 was plugged and abandoned (P&A’d) while the HA115 rig was demobilized to Herd Base. The group is considering to drill Antelope 7 by second half of 2016. Moreover, its Rig 103 was also rigged up for drilling the Strickland 1 exploration well in April. Strickland 2 was spudded this month and the group is drilling ahead, having a planned total depth of 890 meters.

Antelope 6 appraisal wells (Source: Company Reports)

Boosting capital position: Oil Search has a strong capital position with a cash and borrowing facility of over US$ 1.7 billion. Accordingly, management indicated that it would use its cash for high yield projects to achieve double the capacity in next 10 years. However, the group also estimates that the gearing is likely to increase during the project period but might decline rapidly on completion of projects. On the other hand, OSH has a competitive advantage of generating strong production at low costs. The company has managed to report positive cash flow even at current oil prices while management expects cash flow breakeven (operational expenses and interest) in 2016 at over US$19/ bbl.

Positioning to leverage the booming LNG prospects: Oil Searchis focusing on its LNG resources and has decided to invest in projects even in the period of low oil prices and accordingly positioning itself to leverage the high-potential long term LNG growth opportunities. In fact, the LNG supply is estimated to rise by 50% in the next five years driven by Australia and Qatar. Moreover, medium to long-term demand growth in Asia looks lucrative on the back of expiry of existing long-term contracts while the group intends to leverage this oppurtunity by rising the supply from its potential PNG LNG third train and Papua LNG. The group’s PNG LNG and Papua LNG project expansion is assessed to have breakeven costs in lowest quartile in region.

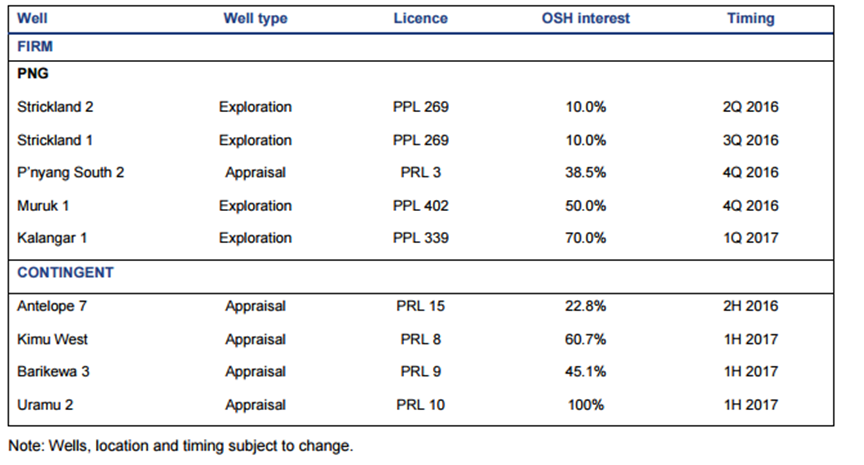

Furthermore, OSH is also planning a major near-field gas exploration campaign in 2016/2017. Oil Search has applied for nine new PNG license applications and will optimize the partnership with Total and Exxon. The group’s exploration program of Muruk (PPL 402) and Strickland (PPL 269) are maturing for drilling in 2016. The company is also preparing to drill Kalangar (PPL 339), Kimu west, Barikewa 3 and Uramu 2 in 2017. OSH is also making arrangements to drill Kimu West (PRL 8), Barikewa 3 (PRL 9) and Uramu 2 (PRL 10) in 2017.

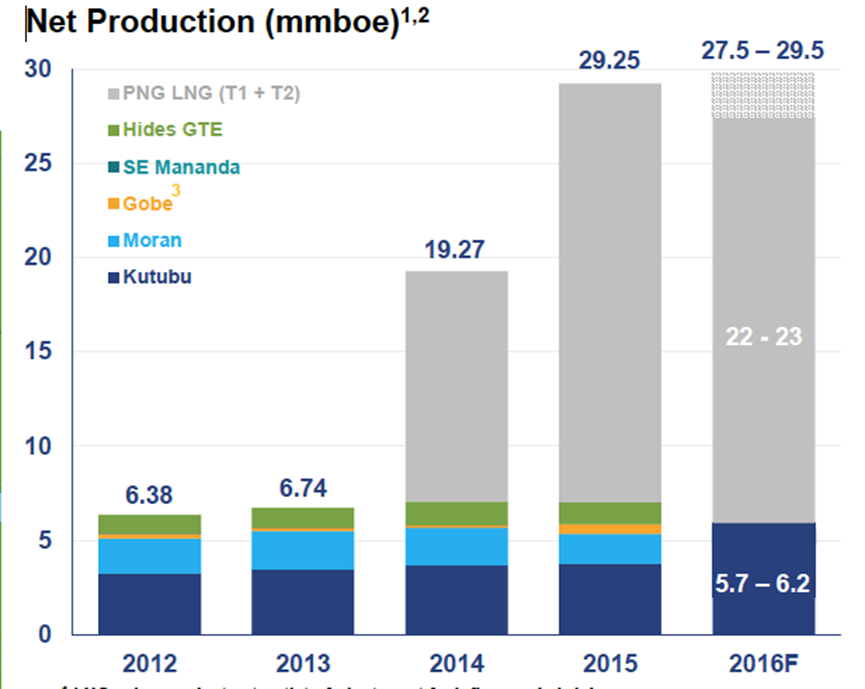

Net production forecasts and performance highlights (Source: Company reports)

Potential PNG LNG Project expansion progress highlights: The group has been making efforts over a possible expansion of the PNG LNG Project as well as the proposed Papua LNG Project development. Moreover, the group believes that the potential integration of these two major potential developments would enable them to maximize value as well as help them to minimize high-cost infrastructure duplication in PNG. Management intends to continue to make efforts to achieve its development activities at lower costs as well as generate operational synergies and enhance the future prospects. Meanwhile, the PNG Government, which has equity in PNG LNG expansion as well as Papua LNG, could deliver solid benefits via generating maximum shared value through this next phase of LNG development in PNG.

Both projects are expected to have an expected gross undeveloped 2C contingent gas resource base of over 10 tcf (gross). The group is confident that there is enough resource to deliver two 4 MTPA LNG trains, while having an option of a third expansion train, which are dependent on further proven resource.

Competitive Edge:Oil Search possesses its interests in PNG LNG and Elk-Antelope resources and at major NW Highlands and Gulf Province exploration licenses, placing the group at a unique position against its peers. Moreover, the group is also well positioned to back its operators, ExxonMobil and Total. OSH also build a track record of strong operating experience, while developed strong government, community and landowner relationships. Meanwhile, the PNG Government comprises equity in both the projects and would also be a major beneficiary of cost-effective and timely development. The group has been delivering its Integrated LNG projects across the globe (Trinidad, Egypt and Qatar).

Guidance:Oil Searchestimates an annual production of 27.5 – 29.5 mmboe for 2016. The group maintains its PNG LNG production forecasts rates in the range of 7.5 and 7.9 MTPA (gross).

OSH is also making preparations for drilling at its P’nyang field while the P’nyang South 2 well is forecasted to spud by end of 2016. OSH is also making preparations to start a planned independent re-certification of gas reserves in the Hides, Angore and Associated Gas fields, by the second half of 2016. This would offer more clarity regarding its volume of 1P gas availability which would be able to back the group’s high-value PNG LNG expansion.

Future exploration or appraisal prospects (Source: Company Reports)

Stock performance: The shares of OSH corrected over 14.7% in the last six months (as of May 17, 2016) as the group’s merger efforts with Woodside Petroleum have failed. On the other hand, management has recently clarified investors that they would continue to pursue acquisition by assessing objective and merits. Moreover, the company is currently taking steps on the basis of the volatile oil prices for the next six to 12 months and accordingly controlling its costs. Management even “defended” its dividend policy of paying out 35%-50% of its core profit and clarified that it remains favorable balance between returns to shareholders as well as holding flexibility for reinvesting in potential projects. On the other hand, OSH recovered over 11.9% (as of May 17, 2016) in the last four weeks driven by the strong recovery in the oil prices. Accordingly, the group’s performance in the coming quarter might also improve as the average realized prices would recover. OSH also planned major near-field gas exploration/appraisal for this year and next year, and the positive outcome from these activities would further boost the stock.

The group’s several initiatives in 2015 to recalibrate costs as well as plan capital spend would generate benefits this year and this would enhance its operational efficiency. Based on the foregoing, we reiterate our “Buy” recommendation on this dividend yield stock at the current price of $7.03

.PNG)

OSH Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...