Company Overview: Oil Search Limited is an oil and gas exploration and production company. The Company is engaged in the exploration for oil and gas fields and the development and production of such fields. The Company's segments include PNG Business Unit (PNG BU), Exploration and Other. The PNG BU segment is engaged in the development, production and sale of liquefied natural gas (LNG), crude oil, natural gas, condensate, naphtha, other refined products and electricity from the Company's interest in its operated assets for Papua New Guinea crude oil and Hides gas-to-electricity operations and from the Company's interest in the PNG LNG Project. The Exploration segment is engaged in the exploration and evaluation of crude oil and gas in Papua New Guinea. The Other segment includes the Company's ownership of drilling rigs, investment and development towards the Company's power strategy and corporate activities. The PNG LNG Project is a 6.9-million tons per annum (MTPA) integrated LNG project.

.png)

OSH Details

LNG Demand Expected to Grow at ~4.5% p.a. to 2030: Oil Search Limited (ASX: OSH) has an engagement in the exploration for oil and gas fields and the development and production of such fields. The company reported a decent set of numbers for the period ended June 30, 2019 (1HFY19), wherein revenue increased by 39% to US$776.9 million as compared to the previous corresponding period. Net Profit after tax for the period increased by 105% on pcp to US$161.9 Mn. Operating cash flows for the period increased by 72% on pcp to US$418.5 Mn, reflecting higher sales and average realised LNG and gas prices in H1FY19, partially offset by higher production costs. The Board of Directors declared an interim dividend of 5 US cents per share with record date and payment date on September 4, 2019 and September 24, 2019, respectively. Looking at the past performance over FY16 to FY18, total revenue of the company has grown with a compound annual growth rate (CAGR) of 11.5%, and the bottom-line grew at a CAGR of 94.9% over the same period. Total revenue improved from $1,235.908 Mn in FY16 to $1,535.761 Mn in FY18, and net profit improved from $89.795 Mn in FY16 to $341.202 Mn in FY18.

Due to lower product sales, total revenue for the September’19 quarter reduced from the previous quarter. However, with a decent outlook for the gas market in the coming decade, it is expected that the company will see an uplift in the number of contracts, expansion in the new market and production ramp-up in the coming times. Moreover, 2019 PNG optimization activities are expected to boost operated production from Q4FY19. As per the report, there was an increase of 15% in LNG demand in H1FY19 as compared to H1FY18, and it is expected to grow at ~4.5% per annum to 2030. Spot price has softened due to unseasonably mild North Asian weather and new supply entering the market, validating PNG LNG strategy to execute mid-term contracts, i.e., long-term 6.6 MTPA, mid-term 1.3 MTPA, spot less than 1 MTPA. Significant gas discovery at Muruk 2, NW of hides, etc., are expected to help the company to maintain and expand its supply in the long run.

.png)

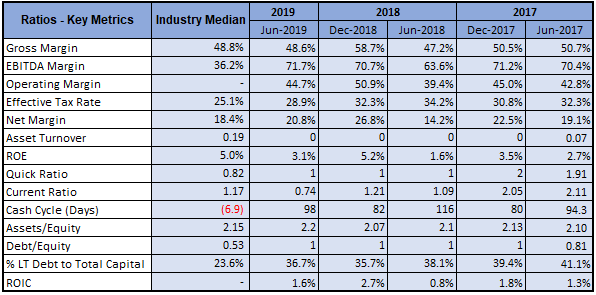

H1FY19 Key Financial Metrics (Source: Company Reports)

September’19 Quarter Key Highlights: Total revenue for the period stood at US$361.1 Mn as compared to US$378.9 Mn in the previous quarter, reflecting lower product sales and timing of shipments with three LNG cargoes on the water at the end of the quarter, weaker global oil prices and a higher proportion of condensate, relative to oil in the product mix. During the period, 29,595 billion Btu of LNG from the PNG LNG Project (net to Oil Search) was sold, which was 6% lower than sales volumes in the second quarter of 2019. In total, the company delivered 26 LNG cargoes, which comprised 18 cargoes sold under long-term contracts, 5 cargoes under mid-term sale and purchase agreements, and 3 cargoes on the spot market, as compared to 28 cargoes sold in the previous quarter. At the end of the period, three cargoes were on the water as compared to two at the end of the second quarter of 2019.

Sale volumes for oil, condensate, and naphtha decreased by 3% to 1.02 mmbbl, as compared to the previous quarter. The average oil and condensate price realized during the period decreased by 13% to US$59.54 per barrel, mainly due to a weaker period for global oil prices and a different product mix, with higher condensate volumes relative to crude oil during the mooring buoy disruption. The average price realised for LNG and gas sales was reported at US$9.44/mmBtu, a 2% increase than the previous quarter. This can be attributed to a three-month lag between the spot oil price and LNG contract prices.

Total Sales revenue from LNG, gas, oil and condensate for the quarter was reported at US$361.1 Mn, a 5% decrease than the previous quarter. Other revenue comprising rig lease income, infrastructure tariffs, electricity, refinery and naphtha sales, increased from US$9.8 Mn to US$10.1 Mn.

Company’s liquidity position at the end of the quarter stood at US$1.18 Bn, comprised of cash and undrawn credit facility of US$547.3 Mn and US$635.7 Mn, respectively. During the period, the company executed US$300 Mn of one-year corporate credit facilities, increasing the Company’s revolving credit lines to US$1.2 Bn. From these credit facilities, US$470 Mn was drawn down to help fund Alaskan Option payment of US$450 Mn and the payment of interim dividends of US$76.2 Mn. The company ended the quarter with US$3.59 Bn of debt outstanding, relating to the PNG LNG project finance facility and corporate debt, as compared to US$3.12 billion at the end of the previous quarter.

.png)

September’19 Quarter Key Sales Metrics (Source: Company Reports)

Total PNG LNG Production for YTD till Sep’19 Improved By ~19.8% on PCP: Total production for the period stood at 6.8 million barrels of oil equivalent (mmboe), marginally lower than the previous quarter. This can be attributed to the reduction in rates of liquids loading for the short term following the detection of damage to one of the mooring chains at the Oil Search-operated offshore liquids loading facility in the Gulf of Papua. However, repair work on the damaged chain was completed in mid-October, and standard loading operations were reinstated, and production ramped up to normal rates.

Contribution from the PNG LNG Project stood at 6.2 mmboe net to the company based on an annualized gross production rate of 8.3 MTPA for the period.

.png)

September’19 Quarter Key Production Metrics (Source: Company Reports)

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together form around 35.18% of the total shareholding. Mubadala Investment Company PJSCand Capital Research Global Investors hold maximum interest in the company at 12.89% and 7.59%, respectively.

.png)

Top 10 Shareholders (Source: Thomson Reuters)

A Quick Look at Key Metrics: Gross margin for H1FY19 stood at 48.6%, in-line with the industry median of 48.8%. EBITDA margin and net margin for H1FY19 stood at 71.7% and 20.8%, better than the industry median of 36.2% and 18.4%, respectively, which implies decent fundamentals for the company.

Key Metrics (Source: Thomson Reuters)

Recent Updates:

In September 2019, the PNG Cabinet reviewed and validated the Papua LNG Gas Agreement. It passed key legislative changes required under the agreement in mid-October. The PRL 3 Joint Venture and the PNG Government are committed to ensure the proposed integrated three-train LNG development and proceed into the Front-End Engineering and Design (FEED) phase as soon as possible.

In another update, work is under progress to optimize the Pikka Unit development. Additionally, potential debottlenecking opportunities for the full field development facilities were reviewed, which could increase throughput from 120,000 barrels of oil per day (bopd) to up to 150,000 bopd. A partial sell-down of the Company’s Alaskan equity interest is expected to complete in mid-2020 prior to the Final Investment Decision (FID) on the Pikka Unit development.

In early October 2019, the company informed the market that Dr Keiran Wulff, OSH’s Executive Vice President, Alaska and President of Oil Search Alaska, is expected to replace Peter Botten as Managing Director on February 25, 2020. Mr. Botten is expected to remain with the company until August 25, 2020, and support the project as the PNG LNG, P’nyang and Papua LNG Joint Venture partners move towards an FID on LNG expansion in PNG.

As per media reports on “Paris Aligned Investment Report”, which examines oil and gas investments that would be required under different climate change scenarios, including a “Paris-aligned” scenario, OSH was ranked in the top quartile for climate change transition risk. In another achievement, the company was included in the Dow Jones Sustainability Index (DJSI) World and DJSI Australia, for the third successive year, in the month of July 2019. This can be attributed to the company’s performance in the areas of risk management, social reporting, and corporate citizenship and philanthropy. Additionally, the company achieved a ‘Leading’ rating in the Australian Council of Superannuation Investors’ (ACSI) annual review of the level of ESG reporting by ASX200 listed companies, released in August 2019.

Key Risks: The company is susceptible to certain risks such as financial and liquidity risks (pricing risk and risks associated with future operating and capital costs requirements), operational risks (production decrease, safety and environmental and cyber security), reserves, resources and development risks (reserves decline and replacement, reserves and resource estimates and project development and execution), external and stakeholder risks (legislative and regulatory risks, climate change, risks associated with political, community and other stakeholders), etc.

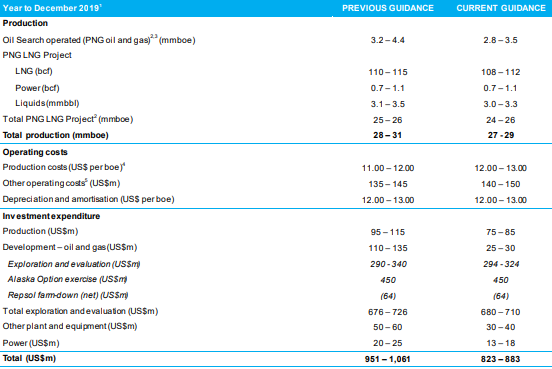

What to Expect: Due to the loading issue, FY19 production guidance for the company has been revised from 28 – 31 mmboe to 27 – 29 mmboe. Unit production costs are expected to be in the range of US$12 - 13/boe, reflecting the lower production base, costs associated with the repairs to the mooring buoy and lower insurance receipts for earthquake remediation activities. Other operating costs have also risen from the previous US$135-145 Mn to US$140-150 Mn, due to lower operator overhead recoveries, SE Mananda site restoration provisions and execution costs incurred for the Alaskan Option and sell-down process.

Capital cost guidance has been reduced materially due to the deferral of spending on FEED activities for LNG expansion and adjusted work programs on the company’s operated assets.

FY19 Guidance Update (Source: Company Reports)

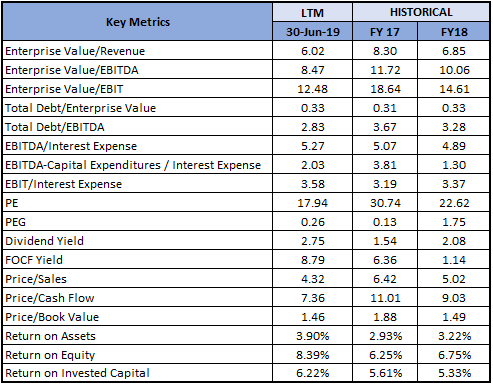

Key Valuation Metrics (Source: Thomson Reuters)

Valuation Methodology: Price to Cash Flow Multiple Approach (NTM):

.png)

Price to Cash Flow Multiple Approach (Source: Thomson Reuters), *NTM-Next Twelve Months

Note: All forecasted figures and peers have been taken from Thomson Reuters, *NTM-Next Twelve Months

Stock Recommendation: Oil Search Limited’s share generated a positive YTD return of 4.76% and is trading below the average of 52-week high and low of $8.460 and $6.300. On the technical analysis front, the stock retraced from the Fibonacci retracement level of 61.8% on October 10, 2019, which suggests a probability for the continuation of an upward trend. Company’s first-half financial performance stood better than the previous corresponding period. With a decent long-term LNG outlook and the company’s expansion program into new markets, it is expected that the company will be able to boost its earnings in the coming years. Looking at the business prospects over the long-term, we have valued the stock using a relative valuation method, i.e., Price to Cash Flow multiple, and arrived at a target price of single-digit growth (in % term). Hence, we give a “Buy” recommendation on the stock at the current market price of A$7.180 per share, down 1.238% on October 30, 2019.

(1).png)

OSH Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...