Kalkine has a fully transformed New Avatar.

Company Overview: Oil Search Limited is an oil and gas exploration and production company. The Company is engaged in the exploration for oil and gas fields and the development and production of such fields. The Company's segments include PNG Business Unit (PNG BU), Exploration and Other. The PNG BU segment is engaged in the development, production and sale of liquefied natural gas (LNG), crude oil, natural gas, condensate, naphtha, other refined products and electricity from the Company's interest in its operated assets for Papua New Guinea crude oil and Hides gas-to-electricity operations and from the Company's interest in the PNG LNG Project. The Exploration segment is engaged in the exploration and evaluation of crude oil and gas in Papua New Guinea. The Other segment includes the Company's ownership of drilling rigs, investment and development towards the Company's power strategy and corporate activities. The PNG LNG Project is a 6.9-million tons per annum (MTPA) integrated LNG project.

.png)

OSH Details

Acquired 50% interest and operatorship of 120 leases in Alaska North Slope: Oil Search Limited (ASX: OSH), having a market capitalization of about $11.8 billion, has contributed to about 13% of the gross domestic product of Papua New Guinea region and is the largest oil and gas exploration company in said region. OSH has now expanded the lease position in the eastern area of the Alaska North Slope with the acquisition of 50% interest and operatorship of 120 leases. The company is required to pay approximately US$8 million for these leases (initially 100% controlled by Armstrong). 50% of the acquisition cost has been indicated to be incurred by Lagniappe at an average of US $82 per acre. This is expected to be formally awarded by the State around mid of 2019. With the acquisition of leases, OSH will strengthen the position in Alaska and will continue to work with Armstrong under its growth strategy.

Resilient Performance: During the first half of 2018, OSH had faced issues owing to the most devastating PNG Highlands earthquake in February 2018. However, the company was still able to end 2018 on a high note. The total liquidity was reported at US $1.5bn and comprised of US $600.6 million in cash and US $900 million in undrawn credit facilities. Primarily, refinancing and higher committed bilateral bank lines helped the company. OSH also repaid the PNG LNG Project finance debt of US$332 million, and the net debt at the end of 2018 stood at US$2.7 billion.

Oil Search for the full year 2018 had delivered the total production of 25.2 mmboe and sales revenue growth of 6% to US$1.54 billion against 2017. The 2018 full year production is in line with the company’s 2018 guidance range. As the first half of 2018 was impacted significantly, the company’s total production had recovered strongly in the second half. This has been on the back of strong performance of the PNG LNG Project, which had produced at an annualised rate of 8.8 MTPA, that is its highest-ever half-year rate. Meanwhile, for the fourth quarter 2018, the company’s total oil and gas production was 7.4 mmboe, being on track as before despite the challenges witnessed owing to earthquake. There was a 16% rise in operated production to 1.0 mmboe (on a quarter on quarter basis). This growth was driven by the contribution from the Moran and Agogo fields, which resumed production in the third quarter of 2018. The earthquake remediation work was well undertaken by the group, particularly at remote sites, and the same was slated to be nearing completion.

OSH’s PNG LNG Project averaged 8.7 MTPA in terms of production during the fourth quarter and this was relatively below the levels reported in the third quarter 2018; and was owing to two minor unplanned outages at the plant. Post resolving the issues, the plant has been brought online. Nonetheless, the group could manage to deliver 6% growth in the total revenue to US $503.1 million at the back of 5% rise in sales volumes and 5% increase in the average realized LNG and gas price to US $10.96 / mmBtu. However, a 15% decline in the average realized oil and condensate price to US $64.45 per barrel was still noted given the drop in the oil prices at the global level and as predominant over the fourth quarter.

.png)

December 2018 Quarter Performance (Source: Company Reports)

Major Developments: During the December 2018 (fourth) quarter, the PRL15 joint venture participants signed the Memorandum of Understanding (MoU) with the Independent State of Papua New Guinea with regard to the development of the Papua LNG Project. Under the MoU, and key terms and conditions of the Papua LNG Project Gas Agreement, the aspects on tax rates and Domestic Market Obligation have been slated for coverage. As per the plan, Government and the PRL15 and PRL3 JVs will be finalizing the Papua LNG and P’nyang Gas Agreements before the end of March 2019; and subsequently, integrated Front-End Engineering and Design (FEED) entry decision will be taken. This will set the framework for the three-train LNG expansion. Lately, ExxonMobil (on behalf of the PNG LNG Project participants) has pursued the discussions on the final mid-term tranche of 0.45 MTPA set to be marketed from the PNG LNG Project; and these negotiations have been earmarked for completion in the first quarter of 2019. The total sales under contract will be then expanded from PNG LNG to about 7.9 MTPA. With regards to the development at the PNG Highlands, drilling at the Muruk 2 appraisal well has been started in the December quarter and target reservoir is expected to be reached shortly. OSH has also completed two seismic acquisition programmes during the fourth quarter 2018, and that too in the onshore Papua Gulf Basin and Forelands region of PNG. Thus, OSH has been able to progress well on its key onshore seismic programmes despite challenging conditions. Meanwhile, Pikka B well in Alaska has also been identified to report oil presence in the target Nanushuk sands.

Future Outlook: Oil Search is scheduled to provide FY 18 financial results on 19 February 2019 and full year 2018 production costs and depreciation and amortisation charges are expected to be at the lower end of the previously projected guidance ranges of US$11.50 – 12.50 /boe and US$12.00 – 13.00/boe, respectively. The production costs for the year 2018 will have about US $65 million that OSH had to spent on earthquake recovery and repairs activities; while a part of this will be offset by insurance recoveries and remaining amount will be incurred by OSH. Other operating costs (including Hides GTE gas purchase costs, selling and distribution costs, royalties and levies, rig operating costs, inventory movements, power, earthquake donations of US$5.1 million, corporate and business development and other costs) are slated to be at the bottom of the guidance range of US$140 – 150 million. Net financing charges are expected to be in the range of US$209 and US$213 million while the full year exploration and evaluation expenditure will be US$66.4 million (related to seismic acquisition in PNG and for the geological, geophysical and general and administration activities). OSH expects total production to be in the range of 28MMboe and 31.5MMboe for full year 2019; and OSH operated PNG Oil & Gas expects to post production in the range of 4MMboe and 5.5MMboe.

.png)

Production Guidance for 2019 (Source: Company Reports)

Margins Higher than Industry Median: Oil Search Limited happens to possess decent position and the key margins might support it in driving improved performance moving forward. The company’s net margin at the end of June 2018 was 14.2% which is higher than the industry median of 10.4% and implies the company’s capability to convert its revenues into bottom line as compared to the broader industry. There are expectations that this capability would drive the company’s growth and might place it in the strong position as compared to the industry moving forward. The company’s EBITDA margin stood at 63.6% at the end of June 2018 which is higher as compared to the industry median of 33.9%. The company’s return on equity or ROE and current ratio at the end of June 2018 stood at 1.6% and 1.09x, respectively. Also, the company’s net margins have showcased significant improvement in the past three years to FY 2017 (FY 2015-FY 2017). In FY 2015, the company’s net margin stood at -2.5%, while it was 20.9% in FY 2017.

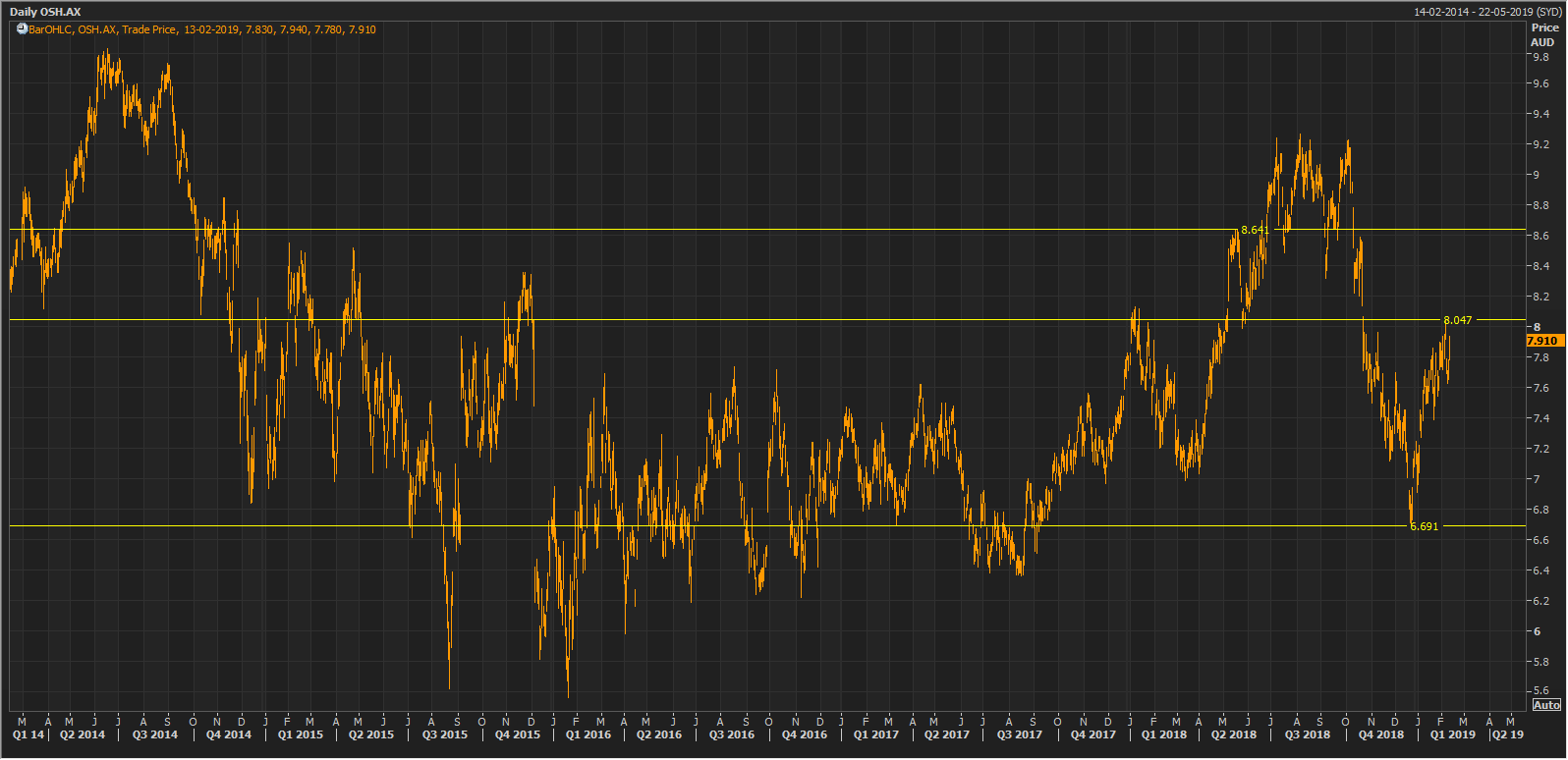

Stock Recommendation: OSH stock has risen 2.65% in one month as on February 12, 2019. The company’s stock is trading at A$7.91 and has an immediate support at $6.7 and resistance around $9 level. From technical standpoint, Exponential Moving Average or EMA has been applied on the daily chart of Oil Search Limited and default values were used for the purposes. After careful observation, it was noticed that the stock price has crossed the EMA and is trending in the upward direction. This reflects the bullish momentum and, thus, further builds confidence that the company’s stock price might witness a rise moving forward. Otherwise also, OSH had posted resilient performance in the fourth quarter and had ended 2018 with decent liquidity position. The company will post FY 18 financial result on 19th February 2019. Meanwhile, OSH stock along with other energy stocks are showing positive strength given the oil price scenario, driven by significant OPEC production cuts, with Saudi Arabia’s plan to reduce the March crude output. Further, the oil prices saw an uptrend on the back of hopes on U.S.-China bilateral trade talks. Given the above backdrop and company’s position to regain a healthy performance in terms of volumes etc. in 2019, a single digit stock price upside is expected in next 12-24 months and we give a “Buy” recommendation on the stock at the current price of $7.91.

OSH Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...