Company Overview – Nufarm Limited is a chemical product manufacturer. The company produces and markets agrochemicals to farmers to protect their crops. Its products include herbicides, insecticides and fungicides. Nufarm’s products are used to protect crops against damage caused by weeds, pests and disease. The company also sells seeds and seed treatment products including canola, sorghum and sunflower crops. It also provides marketing and technical support services. The company’s manufacturing and marketing operations are based in Australia, NZ, Asia, Europe and Americas.

Analysis – Nufarm Limited along with its subsidiaries produces and sells crop protection product worldwide. The company manufactures and sells herbicides and pesticides to protect crops from damage due to weeds, pests and diseases. The company also owns marketing rights of Monsanto’s round up brands of herbicides in Australia and NZ. Nufarm operates through two reportable segments namely crop protection and seed technologies.

The crop protection segment manufactures crop protecting products used by farmers to protect their crops from weeds, pests and other diseases. The segments product line includes herbicides and pesticides. It offers glyphosate, phoenixes, other herbicides, insecticides and fungicides among others. The seed technologies segment engages in the sale of seeds and seed treatment products. It focuses on seeds such as canola, sorghum and sunflower seeds.. The company seed business is carried out under the name Nuseed. In August 2012 Nuseed launched Roundup TRANSORB X, glyphosate herbicide on the NZ market.

The company owns manufacturing and marketing facilities across several geographies including Australia, New Zealand, Asia, The Americas and Europe. The company’s North America business region includes Canada, US, Mexico and the Central American countries. The south American business region includes Brazil, Argentina, Chile Uruguay, Paraguay, Bolivia and the Andean countries. The company also has several marketing partnerships worldwide. Nufarm established manufacturing and marketing collaboration with Excel Crop Care Ltd in India and F&N Joint Venture in Eastern Europe.

The company operates a number of subsidiaries across the world. Some of the key subsidiaries of the company include Nufarm Australia Ltd, Crop Care Australasia Pty Ltd, Croplands Equipment Pty Ltd, Nufarm S.A., Nufarm GmbH & Co KG, Nufarm Agriculture Inc, Nufarm NZ Limited, Nufarm Americas Inc and Nufarm K.K. among others.

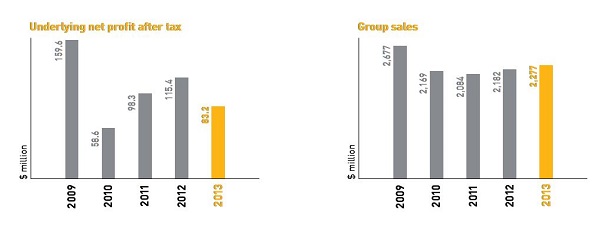

Source - Thomson Reuters

Source - Thomson Reuters

At its September result NUF flagged a strong start to the year particularly driven by Brazil and Australia. As expected conditions have been less favourable in eastern Australia with a dry October in QLD and Northern NSW in particular. This has depleted soil moisture levels and has created unfavourable conditions for the current summer crop plant. While Australia in first quarter is up versus the previous corresponding period, it has not performed to the level that NUF anticipated back in September. The Brazilian crop protection market continues to see strong growth driven by expansion in the cropping acres, higher investment in inputs and increased pest pressures in parts of the Soybean Crop. Europe and North American first half profit is expected to be below the previous corresponding period but this is also a quiet time of the year seasonally.

Source - Thomson Reuters

Source - Thomson Reuters

|

Price |

Price % Change |

|

Close: |

4.09 (24-Jan-2014) |

3M: |

(14.97%) |

|

52 Wk High: |

5.83 (25-Feb-2013) |

6M: |

(9.11%) |

|

52 Wk Low: |

3.85 (18-Apr-2013) |

1Y: |

(25.64%) |

Nufarm provided guidance for first half 2014 Earnings Before Interest & Tax (EBIT) of around $50-$60 Million, in the previous corresponding period it was $47 Million. The key contributor to this increase will be growth in Brazil, with the major swing factor attached to near term conditions and product demand in Australia. Nufarm expects earnings growth at the fill year. It has refinance its syndicated debt facility for a term of 3 years. Nufarm continues to benefit from increasing geographic and product diversification. However ANZ remains the largest contributor. In this key market the FY14 trading is currently exceeding previous corresponding period.

As Nufarm is exposed to the demand from the agricultural sector of the economy, the weather can create enormous year to year volatility in sales. The risk is in our view somewhat mitigated by the group’s broad geographic exposure.

In FY13 Australia and New Zealand suffered from a difficult seasonal and trade environment throughout the year. Australia’s condition remains challenging in the first few months of FY14 in a number of key cropping regions. Dry weather in north western and northern regions of NSW and in QLD persisted. The low moisture level has meant there was little demand for herbicides and consequently higher levels of inventory. However we still expect the ANZ to recover from FY2013.

Asian crop protection sales were flat compared to the previous corresponding period. NUF notes that Asia is tracking in line with expectation over the last few months, NUF has pointed out in September that Asia is expected to be down due to the margin pressure on glyphosate. In FY13 North America crop protection sales increased by 10% to $516 Million with both the US and Canada showing big improvement with sales compared to the previous corresponding period. While NUF notes that the autumn weather patterns were normal in US and Canada in the first few months of FY14, it expects US to be down on a previous corresponding period basis due to the phasing issues.

In Europe sales grew by 8% to $468 million with underlying EBIT up a very impressive 32% to $57 Million in FY2013. One of NUF’s major synthesis plants in Europe was shut down for general maintenance in the first quarter which resulted in lower phenoxy herbicides sales. We expect only very modest growth in Europe in FY14 given the need for consolidation and some further investment. South America was also a standout performer for NUF in FY 2013 with sales up 30% to $431 Million and the underlying EBIT more than doubled the previous corresponding period. The trend continues in the first few months of FY14 with Brazil crop pro2tection market experiencing strong growth. This is supported by a combination of expanded cropping acres, a higher investment in inputs and increased pest pressures in parts of the Soybean Crop. The loss of roundup agreements has not had a material negative impact on earnings. A few months into the new arrangement, NUF points out that its Australian glyphosate business will not suffer from the loss of the Roundup brand and they are seeing good support from its distribution customer base.

Source - Company Reports

Source - Company Reports

|

Dividend |

|

|

|

|

Yield |

1.777778 |

FY |

Payout Ratio |

31.37875 |

FY |

|

|

1.397669 |

5yr Av |

|

90.86742 |

5yr Av |

With difficult summer likely to impact earnings and working capital levels, we would see weakness around this period and recommend BUY on this stock with a longer term buying opportunity at the current c;osing price of $4.09.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...