Company Overview: Noni B Limited is engaged in retailing of women's apparel and accessories. The Company operates within the women's fashion retail sector in Australia through a national network of boutique stores under the brands of Noni B and Liz Jordan. It also operates Queens park and Events brands. The Company creates its products, which are manufactured under contract by third-party suppliers. It offers various types of dresses, such as day dresses, evening dresses, maxi dresses and print dresses; tops, such as T-shirts, shirts, kaftans, tanks and tunics; knitwear, such as cardigans, sweaters and jumpers, and capes and ponchos; outerwear, such as jackets, coats, shrugs and vests; bottoms, such as pants, skirts, denim and shorts; intimates, such as bras, briefs, camisoles and slips; occasions, such as mother of the bride, desk-to-dinner, travel range and the slimming range, and accessories, such as scarves, eyewear, hand bags and fascinators. It operates through a retail network over 220 stores.

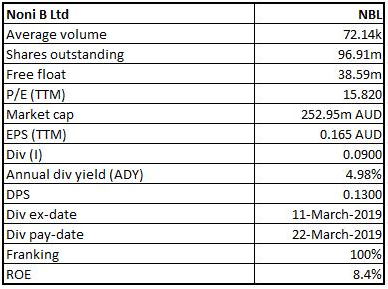

NBL Details

Anticipating Decent Top-line Growth in FY19: Noni B Limited (ASX: NBL) is an ASX-listed company whose principal activities revolve around retailing of women’s apparel and accessories. The market capitalisation of Noni B Limited stood at ~$252.95 million as on July 23, 2019. The company earlier released its report for the half-year ended December 2018 (or 1H FY19) in which it posted total group revenue amounting to $464.4 million, which reflects a rise of 140.4% on YoY basis. The company’s underlying EBITDA stood at $29.1 million, which implies a rise of 31.4% from 1H FY18. The significant rise in the sales in 1H FY19 was witnessed after the acquisition of 5 brands from Specialty Fashion Group on July 2, 2018. The company also witnessed much improved November & December trading result, and this happens to be a direct outcome of core strategies, which were implemented post-acquisition to rebuild the acquired five brands’ product range, variety and stock levels together with the enhanced emphasis on the specific customer base of each brand. The company stated that they have wrapped up the majority of the integration which was required throughout the group. This included consolidating the supply chains, systems and reporting as well as establishing single support centre so that the learnings could be shared and NBL can be in a position to take advantage of the vast array of data. From the analysis standpoint, the company's revenue has grown at a CAGR of 34.1% over the period of FY14-FY18. Going forward, the Management expects revenue to record a Y-o-Y growth of around 132% in FY19. With this, we expect the CAGR-growth in revenue for the period FY14-FY19E at 49.7%. Based on the foregoing, we have valued the stock using Relative Valuation method, Price to Cash Flow multiple and have arrived at the target price of the stock, which is offering a double-digit upside potential (in %).

.png)

Key Numbers of 1H FY19 (Source: Company Reports)

Top 10 Shareholders: The following table provides a broad overview of the top 10 shareholders of Noni B Limited:

.png)

Top 10 Shareholders (Source: Thomson Reuters)

Decent Key Metrics: It can be said that Noni B Limited is possessing a respectable position when it comes to its key margins, which further strengthens the confidence in the company’s operational capabilities. In FY18, the company’s net margin stood at 4.6% which reflects a rise of 3.6% on YoY basis and, thus, it can be said that it’s capabilities to convert the top line into bottom line has been improved. Also, the company’s EBITDA margin stood at 10.4% in FY18 as compared to the industry median of 7%. However, the company’s net and EBITDA margin in 1H FY 2019 stood at 2.1% and 6.7%, respectively.

In 1H FY19, the company’s current ratio was 0.88x, which can be considered at respectable levels. The company stated that its cash flow has been strong and cash on hand as at December 30, 2018 stood at $64.7 million as compared to $34.1 million at the end of December 2017, resulting in the net cash position of $42.4 million.

It looks like that the company has been reducing its exposure to the debt component and this might help the overall company moving forward as it can result in stabilising the balance sheet position. In 1H FY19, Debt/Equity ratio stood at 0.19x, which reflects a fall of 35.6% on a YoY basis. Also, the company’s long-term debt as a percentage to total capital stood at 14.4%, which implies a fall of 5.3% on a YoY basis. Moreover, the company was able to convert its inventory to cash in a more efficient way than its peers as its cash conversion cycle stood at 9.9 days for 1HFY19 as compared to the industry median of 58.4 days.

.png)

Key Metrics (Source: Thomson Reuters)

Announcement About Appointment of Director: Noni B Group Limited has made an announcement about the appointment of Jacqueline A Frank as a Non-Executive Director of the company with immediate effect. The release stated that Jackie happens to be one of Australia’s most experienced media executives who has a deep background and understanding of retail and fashion sector. Moreover, she has a long track record of building, developing and maintaining brands and as the founder of the BeFrank Group consults to several local and international organisations when it comes to brand development.

Announcement About FY19 Trading Update: Recently, Noni B Limited made an announcement about the trading update for FY19. The company stated that its total sales rose to around $864 million. Additionally, online sales continued to grow as the proportion of total sales. There are expectations that the company’s underlying EBITDA for FY19 might be in line with the guidance at around $45 million, which reflects a rise of approximately 21% over prior year’s underlying EBITDA of $37.2 million. It is important for the investors to know that underlying earnings are presented before the transaction and restructuring costs, which are related to the acquisition amounting to $9.1 million. The company also added that all the figures are preliminary and subject to the finalisation and review by the company’s auditors.

Broader Understanding Of The Online Growth: Earlier, in an investor presentation, Noni B Limited stated that its online growth has been witnessing favorable momentum at the back of strategic investment towards building and strengthening the online team. Additionally, the company improved the mobile customer experience and deployments have been made towards new digital marketing channels. The following picture provides an overview of the online sales growth:

.png)

Online Sales Growth (Source: Company Reports)

The company made the acquisition of the Millers, Autograph, Crossroads, Rivers as well as Katies brands. This was done from the Specialty Fashion Group via the purchase of assets. It was mentioned that acquired brands are engaged in the operations of retail of women’s apparel and accessories and, therefore, it enhances the product offering to the NBL’s core women’s apparel market.

What To Expect From NBL Moving Forward: Noni B Limited’s key focus and strategies consist of deployment towards the online presence, restocking the acquired brands to the optimum levels as well as product purchase price synergies. The company added that acquisition of loss-making Specialty Fashion Group brands, which involved the total consideration of $31 million in the month of July 2018 more than doubled the NBL’s size. The company anticipated restoring the acquired brands to EBITDA break-even in FY19, and now the company is expecting that they would be achieving positive EBITDA for the current year. Additionally, as can be seen from the below picture, the company’s net assets position has been improved, which might further support its balance sheet position.

.png)

Balance Sheet (Source: Company Reports)

The company’s net cash position has improved from $34.06 million in 1H FY18 to $64.6 million in 1H FY19, which strengthens its position to make deployments towards the operational capabilities. Additionally, these deployments might act as the growth catalysts moving forward.

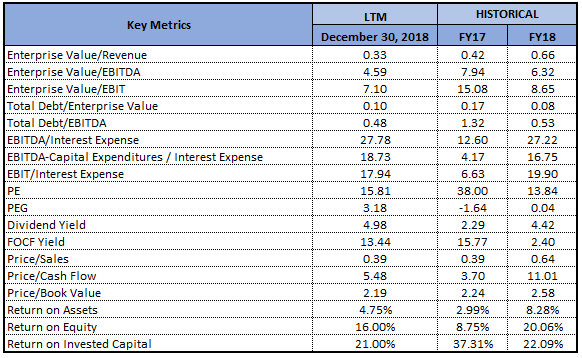

Key Valuation Metrics (Source: Thomson Reuters)

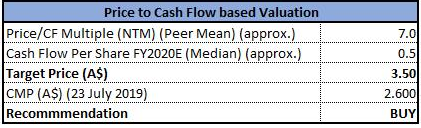

Valuation Methodologies: Price to Cash Flow based Valuation

Price to Cash Flow based Valuation (Source: Thomson Reuters), *NTM: Next Twelve Months

Note: All forecasted figures and peers have been taken from Thomson Reuters, *NTM-Next Twelve Months

Stock Recommendation: From the analysis standpoint, the company seems to be quite attractive as its top line witnessed the CAGR growth of 34.1% in the time span of FY 14- FY18 which reflects that the company is possessing sound capabilities to generate revenues and there are expectations that these capabilities might support long-term growth. Also, the turnaround witnessed in the company’s bottom line performance in the time frame of FY14- FY18 is worth noting. These factors might attract the attention of market players. During FY15-18, the company’s cash from operating activities witnessed the CAGR growth of 61.80% and, therefore, it can be said that NBL is possessing strong operational capabilities. Meanwhile, the stock has delivered the return of -3.33% in the span of the previous six months, while in the time span of three months, the returns stood at -5.78%. The stock is presently trading towards its 52-week lower levels of $2.310 with PE multiple of 15.82x, proffering a decent opportunity for accumulation. Based on the foregoing, we have valued the stock using Relative Valuation method, Price to Cash Flow multiple and have arrived at the target price of the stock, indicating double-digit upside potential (in %). Hence, we give a “Buy” recommendation on the stock at the current market price of A$2.600 per share (down 0.383% on 23 July 2019).

NBL Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...