Kalkine has a fully transformed New Avatar.

Company Overview: Nine Entertainment Co. Holdings Limited is an Australia-based company, which is engaged in television broadcasting and program production, and digital, Internet, subscription television and other media sectors. The Company operates in two segments: Television, which includes free to air television activities, and Digital, which includes Nine Digital Pty Limited and other digital activities. Its brands include Nine Network Television, Nine Digital and Other Businesses. Its Nine Network Television includes Channel 9 and 9HD. Channel 9's content includes a combination of international and locally produced programs with stars, events, dramas, reality and entertainment shows. Its Nine.com.au is an online source of news, sport, entertainment and lifestyle content. It also sell Microsoft's suite of advertising products across Australia and New Zealand. Its Other Businesses include CarAdvice, Literacy Planet, Pedestrain.tv and RateCity.

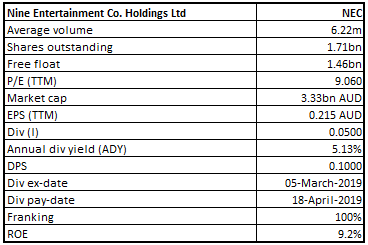

NEC Details

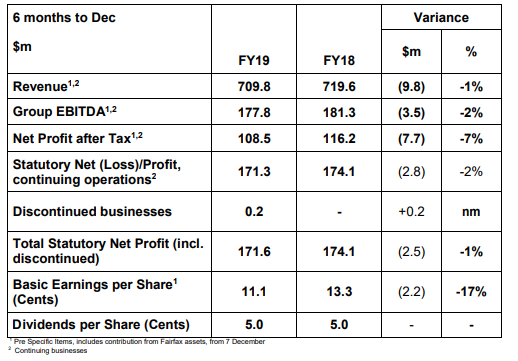

Decent Performance in 1HFY19 Despite Tough Market Conditions: Nine Entertainment Co. Holdings Limited (ASX: NEC) is a mid-cap media and entertainment company with the market capitalisation of ~$3.33 billion as on 23 May 2019. The company operates mainly through six business segments, i.e., Television, Nine Digital, Domain Group, Metropolitan Media, Radio, and Stan, which accounted for about 79.2%, 12.2%, 2.3%, 4.1%, 1.0%, and 1.2%, respectively, of 1HFY19 total revenue. The company has witnessed a compound annual growth rate (CAGR) in revenue of 1.6% from FY14 to FY18 while NPAT encountered a CAGR of 38.0% during the same period which further builds the confidence in the company’s long-term growth strategy. Recently, the company released its 1HFY19 results wherein its net profit after tax (on a statutory basis) stood at $172 million, exhibiting a marginal fall of 1% on the previous corresponding period. The company stated that weakness in Free-to-air (FTA) market got offset by strong FTA share as well as double-digit cost reduction and NEC witnessed a growth of 39% in the Digital & Publishing EBITDA which was supported by >50% growth with respect to both Metro Media and 9Now. There were approximately 1.5 million active subscribers at Stan which reflects a growth of over 60% over the span of 12 months and there are expectations that Stan would move into profit from the fourth quarter. The top management of NEC reflected favourable views with respect to the merger with Fairfax and stated that diverse suite of assets is reaching more Australians each week as compared to any other local media company.

Further, the management stated that approximately 55% of the revenue is from the stable base of broadcasting while 45% is coming from the businesses which are in strong long-term growth markets. This means that the company has been growing EBITDA via more demanding operating environment and it is also investing for the future of the business.

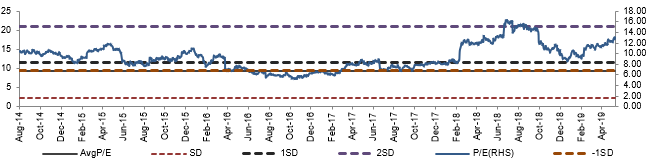

With respect to Domain, it was mentioned that the short-term outlook is defined by the growth in yield as well as lower listing volumes. The continued deployment towards growth initiatives happens to be helped by the ongoing cost discipline. The company’s dividend yield is higher than the industry median which might attract the market players towards the stock. Fundamentally, the stock looks in a decent position with a net margin of 24.0% and ROE of 9.2% in 1HFY19. We expect that the long-term outlook remains favourable for NEC led by viewership market share gains, synergistic merger with Fairfax, focus on cost optimisation strategy, and deleveraging of the balance sheet. Hence, we have valued the stock using two exemplary Relative valuation methods, P/E and EV/Sales and 1-standard deviation to five-year average P/E of 11.64x for FY20E with consensus EPS of around $0.18 and have arrived at a target price upside in the ambit of $2.0 to $2.2 (single-digit upside (in %)). Key risks are changing rules and regulation, adverse advertising market condition, intense competition, increase in compliance cost, etc.

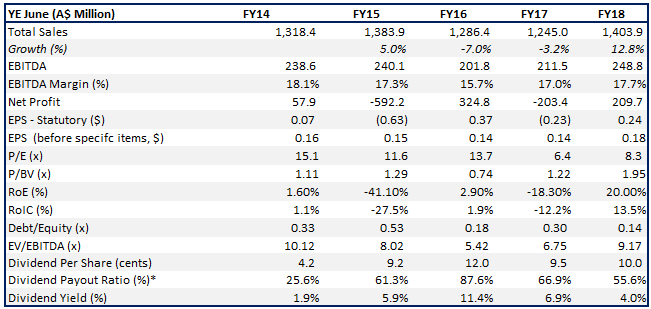

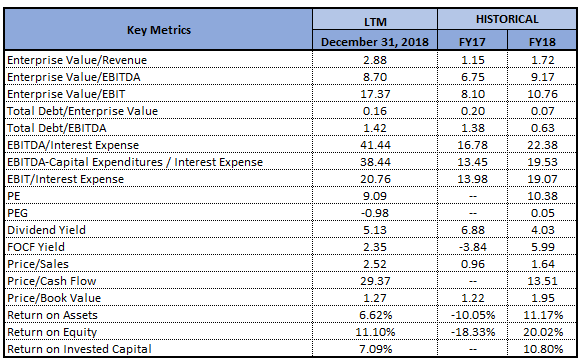

Key Financial Metrics (Source: Company Report, Thomson Reuters)

*Estimated Figures Based on EPS before specific Items

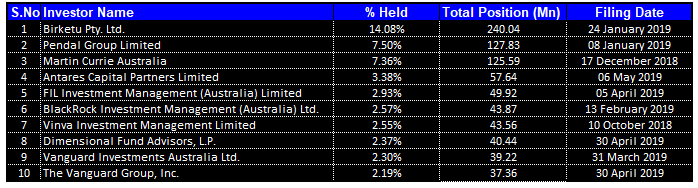

Top 10 Shareholders: The following table gives the broad picture of the top 10 shareholders of NEC:

Top 10 Shareholders (Source: Company Reports)

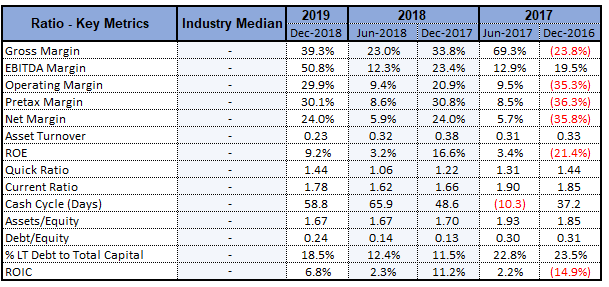

Decent Margins Position Further Strengthens Confidence in Performance: Nine Entertainment Co Holdings Ltd has been possessing decent position with respect to its key margins as its gross margin stood at 39.3% in 1H FY 2019 which implies a rise of 5.5% on YoY basis reflecting that the company is in the better position to address its operating expenses. During the same period, the company’s EBITDA margin stood at 50.8% which reflects an improvement of 27.4% on YoY basis.

Also, there has been an improvement in the current ratio of 7.7% on YoY basis in 1H FY 2019 and stood at 1.78x which reflects an improvement in its liquidity position and, thus, the company is in a better position to address its short-term obligations. The company’s Assets/Equity ratio stood at 1.67x which reflects a fall of 2.2% on YoY basis and, hence, it looks like the company’s reliance on debt, with respect to financing its assets, has reduced.

Key Metrics (Source: Thomson Reuters)

Synergistic Acquisitions – support top-line growth in the long run: On December 7, 2018, Nine Entertainment Co. Holdings Limited got merged with Fairfax by the acquisition of all the outstanding shares in Fairfax, in return for the issue of 0.3627 shares in Nine and 2.5 cents per Fairfax share. Also, on November 5, 2018, the company made the acquisition of the remaining 40.78% of shares of CarAdvice.com Pty Ltd which it did not already own for the cash consideration of $26.5 million. There are expectations that these acquisitions could support NEC moving forward and might help it in delivering the returns to the shareholders. Also, on December 14, 2018, the controlled entity of NEC named Domain Holdings Australia Limited, via partially owned subsidiary (Commercial Real Estate Media Limited) had made the acquisition of 100% interest in Commercialview.com.au Limited, which is an Australian commercial property portal, for the consideration of $8.2 million in the newly issued CREM shares as well as $1.9 million in cash. Hence, we believe that the aforesaid strategic acquisitions will support its top-line growth in the long run.

Trading Update for Q3 FY 2019: With respect to Broadcasting, FTA revenue in Q3 FY 2019 witnessed a rise of 4%. The company stated that FTA market happens to be soft and Nine’s share has been growing. Coming to the Digital & Publishing business, Metro Publishing revenue witnessed a rise of 3% in Q3 FY 2019 and there was growth in both print as well as digital advertising. While Stan witnessed continued growth in the subscribers, Domain has been improving the cost profile.

Unloading of Australian Community Media And Printing: Nine Entertainment had confirmed that it had signed an agreement for unloading of the Australian Community Media and Printing business (or ACM), which is anticipated to be wrapped up by June 30, 2019. ACM would be acquired by the company controlled by interests associated with Antony Catalano and Thorney Investment Group. This transaction is subject to the customary terms for such sale. The cash proceeds are anticipated to be approximately $115 million, subject to the post-completion adjustments. Out of this figure, $10 million would be paid in the span of 12 months. The company intends to utilise the funds towards the reduction of the indebtedness. Additionally, Nine would receive up to $10 million of advertising on ACM properties over the time frame of 3 years from the completion.

ACM and Nine also entered into arrangements which preserve commercial relationships that have existed during Nine’s ownership of the business. The top management of Nine had stated that the unloading of ACM is aligned with the strategy to exit the non-core businesses and to focus towards Nine’s portfolio of high-growth, digital assets.

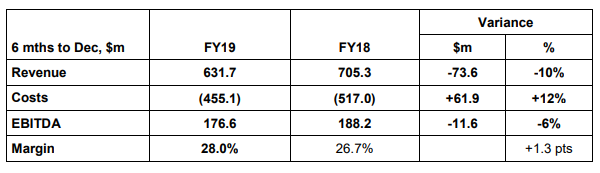

The Decline in Costs Witnessed in Broadcast Traction: Nine Broadcasting division posted EBITDA amounting to $177 million on the revenues of $632 million for 1H FY 2019. In more difficult FTA market, Nine held or grew share in each month except in November-December when cricket-related comparables impacted. Overall, Metro FTA share for the half stood at 39.3%. The division’s reported costs witnessed an improvement of 13% or $62 million for six months. The considered move away from cricket was the reason for much of this change as the company refocused its summer sport to tennis.

Broadcast Business (Source: Company Reports)

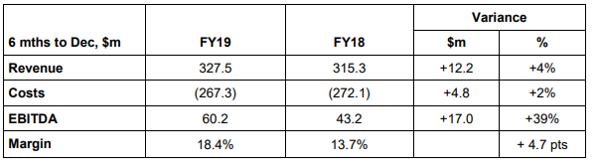

Understanding Digital & Publishing Business: The company’s Digital & Publishing business posted revenue amounting to $328 million and the combined EBITDA stood at $60 million which reflects a rise of 39% for the half. Metro Media witnessed overall revenue growth of 4% after experiencing single-digit declines for the span of 3 years. Metro Media’s ongoing focus towards costs have resulted in a decline of approximately $6 million. With respect to Metro Media, in a recent Macquarie Australia Conference, it was mentioned that premium content is enabling core focus on growth in the readership and subscription, helped by the advertising with growing margins.

Digital & Publishing Business (Source: Company Reports)

Understanding Performances of Domain and Stan: Domain had posted flat revenues in the cyclical operating environment, specifically in the key markets of Sydney as well as Melbourne. The core digital revenues witnessed a rise of 5% and the residential revenue encountered an increase of 9%. The costs encountered a rise by less than 4% on a reported basis, and savings from print and other initiatives were deployed in continuing to develop growth drivers of the business.

Stan posted strong period with respect to the sign-ups and the active subscribers stood at approximately 1.5 million. The robust subscriber growth, along with price rise reflects that Stan is anticipated to exit FY 2019 with positive profit run-rate, and there are anticipations of net positive EBITDA contribution in FY 2020.

Rise in Dividends Might Help in Gaining Traction: Nine Entertainment Co Holdings Limited had declared dividends per share amounting to 5.0 cents in 1H FY 2019 (as shown in the table below) and was flat on the YoY basis. The total dividend paid stood at $85 million as compared to Nine’s dividend of $44 million in 1H FY 2018. This rise in dividends might attract the attention of the market players moving forward. Additionally, for FY 19, the company has forecasted the dividend of 10 cents (fully franked), equating to a yield of approximately 6%. The annual dividend yield of the company is about 6.04% on a five-year average basis (FY14-18). Currently, the annual dividend yield of the company happens to be at 5.13% which is higher than the industry median (Median & Publishing) of 4.0% that reflects that the company is shelling out better dividends as compared to the broader industry. Thus, it looks like that the dividend-seeking investors might consider the stock.

Dividends per share (Cents) (Source: Company Reports)

What To Expect From NEC Moving Forward: In the recent Macquarie Australia Conference, with respect to Broadcasting, NEC had stated that this business aims to hold profitability through the cycle with the help of share gains as well as by focusing on cost. The Domain business is focused on building Australia’s leading digital destination with respect to the property via listings, editorial as well as associated consumer solutions. In the Macquarie Australia Conference, it was also mentioned that the overall positive momentum is anticipated to continue. Nine is anticipating to post Pro Forma Group EBITDA on a continuing business basis of at least $420 million, equating to the growth of at least 10% on FY18 like-basis result of $385 million.

With respect to Broadcasting, the company stated that FY 2019 FTA costs are anticipated to be down by 4% and further cost reductions are also expected in FY 2020 and beyond.

Key Valuation Metrics (Source: Company Reports)

Coming to Digital & Publishing, the company stated that Broadcast Video On Demand (BVOD) market is expected to grow at more than 25% for the span of at least next 3 years and 9Now has been dominating the share. In Digital & Publishing, the company would continue to pursue simplification as well as cost efficiencies throughout the portfolio.

Historical P/E Band (Source: Company Reports)

Stock Recommendation: The stock of Nine Entertainment Co. Holdings Limited had delivered a good return of 11.75% in the span of previous one month while, in the span of the last three months, the returns stood at 16.07% which can be considered at decent levels. There are expectations that Digital and Publishing would continue to grow through H2 FY 2019 and into FY 2020 because of top-line growth as well as further cost efficiency gains with respect to Metro Media and continuing strong growth at 9Now.

Additionally, there are expectations that the company might be supported by an improvement in liquidity levels (as evident from 1H FY 2019 - current ratio) and lesser reliance on debt when it comes to funding the assets (as can be seen from Assets/Equity ratio for 1H FY 2019).

There are expectations that positive momentum would continue at Group level in FY 2020 and, as a result, we have valued the stock using the two Relative valuation methods, P/E and EV/Sales and 1-standard deviation to five-year average P/E of 11.64x for FY20E with consensus EPS of around $0.18 and have arrived at target price upside in the ambit of $2.0 to $2.2 (single-digit upside (in %)). Hence, considering the aforesaid parameters and decent long-term outlook, we give a “Buy” recommendation on the stock at the current price of A$1.985 per share (up 1.795% on 23 May 2019).

NEC Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...