Company Overview - Nine Entertainment Co. Holdings Limited is an Australia-based media and entertainment company. Its assets include the Nine Network, Ticketek, Allphones Arena, Mi9, as well as interests in Sky News Australia and Yellow Brick Road. The Nine Network’s content includes a combination of locally produced programs and international content arrangements, including news, current affairs, sporting events, entertainment and lifestyle programs. The Nine Network broadcasts shows, including The Voice, The Block, Big Brother and sports broadcasting content from the National Rugby League and Cricket Australia. Mi9 is an online media company reaching approximately 10.5 million active Australian online users each month through an offering that spans publishing, online services, data strategies, consumer insights and advertising technologies. In June 2014, Nine Entertainment Co Holdings Ltd announced that AMP Ltd and its related bodies corporate has ceased to be the substantial holder of the Company.

Analysis - During the AGM in November 2014, Nine Entertainment Co. (NEC) reported that FY14 has been a busy year for the Company with completion of the acquisitions of Nine Adelaide and Perth, full control of the Mi9 business, refinancing of debt facilities, and preparation to launch a new Subscription Video On-Demand service. The operating businesses witnessed positive momentum over the year with NEC finishing FY14 ahead of its Pro Forma Prospectus forecasts, reporting year-on-year growth in Pro Forma revenue of 6% and EBITDA of 5% irrespective of soft advertising market over 2H of the year.

.png) FY14 Results (Source – Company Reports)

FY14 Results (Source – Company Reports)

The Company reported improved operating performance of the Nine Network and Nine Live with the Pro Forma results for Nine Digital in line with expectations. Strong cash flow and a conservative leverage profile was further reported. The Company’s maiden dividend of 4.2 cents per share has been declared. The Company expects to commence full franking with effect from the FY15 final dividend.

The efforts to optimise the monetisation of content through more than one distribution channel, with the launch of 9news.com.au and the growth in 9JumpIn are indicative of good progress. The recent integration of TV and digital sales functions also reflects a highpoint. Then, the announcement of the formation of a Joint Venture with Fairfax Media to launch Australia’s first mainstream Subscription Video on Demand or SVOD service (“StreamCo”) in August 2014 is another eye-catching attribute. This is expected to be launched during FY15 and will offer a broad range of local and international programming to subscribers for a fixed monthly subscription fee and no minimum term commitment. SVOD is expected to grow significantly in Australia in the next decade. Quickflix Limited also advised that NEC transferred all 91,165,092 redeemable convertible preference shares it holds in Quickflix from ninemsn Pty Limited to StreamCo Media Pty Limited. Another announcement illustrated “Stan” as the brand behind this business together with details of some of the exclusive content that will be available only on Stan when it launches later in this financial year. The Company is also watchful of the Government’s discussion regarding deregulation of the media sector.

.png) Nine’s Metro Ratings and Revenue Share (Source – Company Reports)

Nine’s Metro Ratings and Revenue Share (Source – Company Reports)

The free to air business recorded EBITDA ahead of Prospectus forecasts. The Live business recorded a strong step up in earnings. Digital business continued its operational transition as per the expectations. NEC reported strong operating cash flow, up $38m (Pro Forma basis) to $272m, and a conservative leverage profile. Owing to these and that the Company refinanced its debt facilities late in the financial year, the benefits of lower interest costs are expected to be seen in FY15.

NEC also explained that differences in Statutory Reported and Pro Forma results for the 2014 financial year arose because of changes in the group operating and capital structure stemming from the IPO and acquisitions, and the impact of one-off items associated with these changes. The Company exceeded Pro Forma Prospectus forecasts in 2014 with revenue 0.8% higher, Group EBITDA 2.0% up, and Operating Free Cash Flow up 17%. Revenue increase of 5.8% resulted in growth in NPAT of 5.5%. The core television business reported Pro Forma EBITDA of $242m, which was $4m above Prospectus and $20m up on FY13. The Metro Free to Air advertising market posed challenges turning from solid growth in 1H to a decline in the last quarter. Nine’s Total People commercial ratings share across the 5 capital city stations rose by 0.9 share points. The full year metro ad revenue share of 38.7% was 0.8 share points more than the Olympic-boosted 2013 share and ahead of Prospectus. The TV costs rose by 2.9% but were $8m below Prospectus. The costs of the 2012 Olympics dropped out but this was more than offset by increases in sports rights costs and increased investment in local production. The FY14 programming costs fully reflected the increase in costs owing to the new long-term cricket and NRL contracts. The Company also increased nightly News from half an hour to an hour at an incremental $10m in annualised costs. The combination of a 4.3% increase in revenues and a 2.9% lift in costs resulted in a 9% lift in TV EBITDA to $242m as compared to 2013.

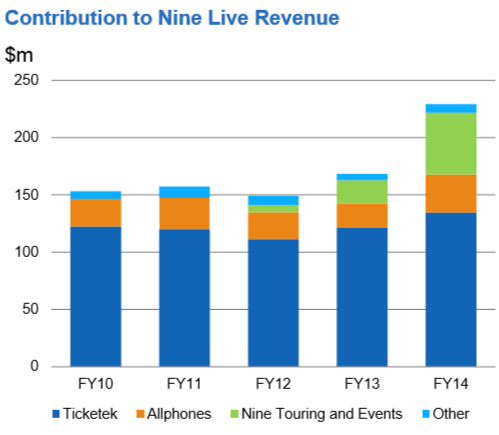

The Nine Live business recorded a strong year with revenue increase by 36% and EBITDA increase by 19% on the prior corresponding period.

Contribution to Nine Live Revenue (Source – Company Reports)

Contribution to Nine Live Revenue (Source – Company Reports)

The core ticketing business, Ticketek, was the largest contributor. Growth has been driven by one of the new businesses, Nine Touring and Events accounting for 24% of Live revenue, up from less than 5% in FY13.

.png) Ticketek’s Ticket Volumes (Source – Company Reports)

Ticketek’s Ticket Volumes (Source – Company Reports)

Underlying revenue growth for Nine Digital of 7% was underpinned by very strong growth in search and video revenues. Nonetheless, it was partially offset by a decline in display ad revenue. Underlying EBITDA was down by around 15% indicating a shift in advertising to lower margin third party inventory along with costs associated with increased product investment. As part of the terms of NEC’s acquisition of Microsoft’s 50% interest in the business, FY15 may be affected by changes to its commercial arrangements witnessing revenue and earnings decline.

.png) Nine Digital Results (Source – Company Reports)

Nine Digital Results (Source – Company Reports)

Operating Free Cash Flow result constituted an 87% Group EBITDA conversion rate, which compares favorably with the 76% Prospectus forecast and the 79% recorded in FY13. Net debt at the end of June was $537m. The Company has an $825m facility following the June refinancing. Going forward, NEC aims to target a 40% Free to Air revenue share by the end of CY15. The content line up – the Cricket World Cup, a UK Ashes Series, the Rugby World Cup, a new season of the Block and the Gallipoli mini-series, will boost the momentum. Then, recent announcements of plans to broaden the touring business base into International Sports and Exhibitions and hosting some of Europe’s best soccer teams in an off season tournament will offer some highpoints. The Company also intends to co-promote the Imperial War Museum exhibition. Stan is expected to offer unlimited access to thousands of hours of entertainment including first-run exclusives, award-winning TV shows, classic catalogue, blockbuster movies and an exciting slate of kids content.

NEC Daily Chart (Source - Thomsown Reuters)

Under FY15 guidance and with an expectation to have a modest growth in second half after few jitters in the first, the Company is confident to deliver ratings and revenue share improvements. NEC expects first half Net Profit after Tax of $85 - $90m. Based on the free to air market growth assumption of 1 to 2% in the second half, full year EBITDA is expected to be at least in line with $311m reported last year. The bottom line will benefit from ~$25m of interest cost savings owing to the new debt facilities. The Company expects to report growth in full year NPAT of ~10%. NEC’s half and full year guidance excludes a one-off profit of approximately $5m on the sale of its HWW business. Further, government’s pending decision on removal of the 75% TV audience reach rule may play a role for NEC along with any intention of acquiring either Southern Cross Media or WIN Corp.

Accordingly, we put a

BUY recommendation for this stock at the current price of $1.905.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Please wait processing your request...

Please wait processing your request...