Company Overview - Nine Entertainment Co. Holdings Limited is an Australia-based media and entertainment company. Its assets include the Nine Network, Ticketek, Allphones Arena, Mi9, as well as interests in Sky News Australia and Yellow Brick Road. The Nine Network’s content includes a combination of locally produced programs and international content arrangements, including news, current affairs, sporting events, entertainment and lifestyle programs. The Nine Network broadcasts shows, including The Voice, The Block, Big Brother and sports broadcasting content from the National Rugby League and Cricket Australia. Mi9 is an online media company reaching approximately 10.5 million active Australian online users each month through an offering that spans publishing, online services, data strategies, consumer insights and advertising technologies.

Analysis – Nine is one of the best placed media companies in Australia to drive sector consolidation. It has strong TV and online platform to leverage, capacity on its balance sheet and a stated desire to pursue acquisitions. We discuss the opportunities that it might consider going forward. We expect a further push for media sector consolidation in the coming years, in part to counter some of the structural change that is occurring across the broader industry that is impacting advertiser and audience behavior. Specifically consolidation will offer media operator benefits such as increased scale and relevance the ability to cross promote and engage audiences across platforms and for longer, the ability to leverage talent across platforms as well as delivering operational synergies. The extent of consolidation will in part be governed by whether certain proposed media sector reforms are adopted.

NEC Programs (Source - Company Reports)

NEC Programs (Source - Company Reports)

In our view, Nine is particularly well placed to acquire other platforms given (1) its strong balance sheet (2) its relatively clean starting position as only owning metro TV and online media (3 ) a powerful negotiating position given its strong TV ratings and financial outlook and (4) potential synergies it could harness through nine events.

NEC Group Revenue (Source - Company Reports)

NEC Group Revenue (Source - Company Reports)

While not a simple transaction to execute we believe an acquisition of Southern Cross Media stands out as highly value accretive for both parties and a good strategic fit for NEC by delivering it a unique national radio and TV platform. The value accretion mostly stems from an arbitrage of existing affiliate arrangements given Nine’s strong ratings and the weakness at Ten. In our view Nine could also pursue a deal with Win, which could be accretive against a backdrop of NEC’s strong bargaining position.

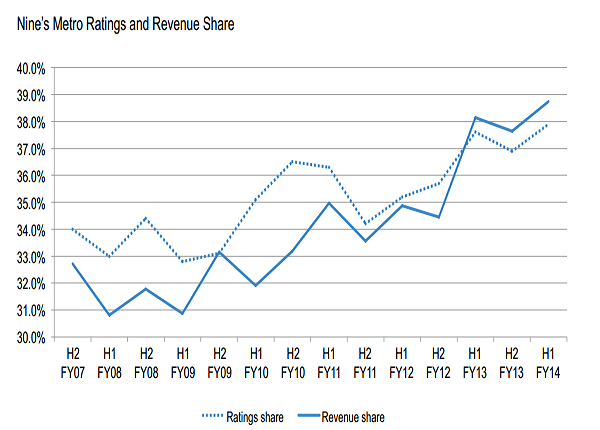

NEC Revenue Share + Ratings Share (Source - Company Reports)

NEC Revenue Share + Ratings Share (Source - Company Reports)

NEC currently operates only metro TV and online in media space. This gives it a relatively clean starting with fewer initial market power constraints than competitors. Given Nine’s strong recent performance and the corresponding weak ratings of Ten Nine is in a strong position when it comes to any consolidation of affiliates. In addition to benefits from a broader media portfolio there exists a clear overlap and potential synergies for Nine by combining a radio business with its Nine events business with radio creating a powerful platform for Nine Events to promote key events to.

NEC Events Revenue (Source - Company Reports)

NEC Events Revenue (Source - Company Reports)

As an alternative to completing a transaction with SXL, Nine could look to acquire its current regional affiliate in WIN TV. This would give it ownership and control of TV broadcast licenses in the remaining 26% of Australia where it currently doesn’t have a presence creating a national platform. Synergies could come from the streamlining of operations and possible revenue synergies with a likely offset from greater investment in the network.

Contribution to events revenue (Source - Company Reports)

Contribution to events revenue (Source - Company Reports)

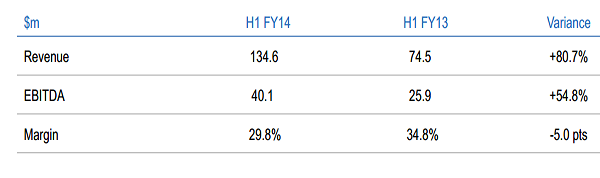

NEC announced in June the establishment of a new $825m debt facility replacing its previous term loan. The term of the new facility is split into two tranches of 4 and 5 years. One off costs of $35m are realized in FY14. These relate to write offs of previously capitalized loan establishment costs and loan early termination costs in relation to the old facility. The new facilities provide Nine Entertainment with significant undrawn capacity, increased operating flexibility to continue to deliver on their growth initiatives and substantial ongoing financing cost savings estimated at $20 million per annum.

NEC Daily Chart (Source - Thomson Reuters)

NEC Daily Chart (Source - Thomson Reuters)

NEC events business is comprised of four divisions: Ticketing & Digital Solution, Entertainment solutions, Data & Technology and Venue (Allphone Arena). In FY13 the division accounted for 11% of group revenue and 19% of group EBITDA. Ticketek is the largest division accounting for approximately 70% of events revenue. We calculate that the Australian ticketing market is worth A$270m per annum with Ticketek’s share at about 50%. Online currently accounts for 61% of Ticketek’s sales and we expect to see this shift on line continue.

Ticketek has long term ticketing contracts with 19 of the top 20 venues in Australia, with Etihad Stadium (Melbourne) the key exception given its established relationship with ticketmaster. The Brisbane Cricket Ground (The Gabba) is another exception where the venue hirer choses its own ticketing service provider. The NEC prospectus indicated a contract renewal rate of over 90% in the prior five years, with three top ten venues due for renewal in FY14. We believe Ticketek only recently resigned its agreement with ANZ Stadium and Sydney Entertainment Centre. We see the potential for NEC to export Ticketek, Softix and Nine Live businesses. We note that Softix has licensed its ticketing platform into 21 countries across Middle East, South America, South Africa and Europe and this could provide an expansion opportunity. NEC may seek out a media company to partner on the promotion side.

NEC is well positioned to leverage cyclical recovery. Nine Network should benefit from the best ratings in 8 years, a recovering ad market, the recent acquisition of Nine Perth and Adelaide and a new earnings accretive affiliate agreement with WIN. Nine events is also set to materially eclipse FY13 revenue growth of 14%. We expect NINE events growth to track above or in line with overall live industry spend in the medium to long term. Nine digital revenues will benefit from growth in the online display advertising industry overall. We put a BUY recommendation on the stock at the current price of $2.09.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...