Company Overview: nib Holdings Limited operates as a private health insurer for Australian residents, New Zealand residents, and international visitors and students to Australia. The Company operates through the segments, including Australian Residents Health Insurance, which operates within the Australian private health insurance industry; New Zealand Residents Health Insurance, which operates within the New Zealand private health insurance industry; International (Inbound) Health Insurance, which include the Company's health insurance products for international students and workers, World Nomads Group, which is engaged in distribution of travel insurance products, and nib Options, which enables access to cosmetic and dental treatment for both overseas and also in Australia. It offers nib Travel Insurance, which include round the clock emergency assist; overseas medical and dental; medical evacuation; passport and travel documents; lost, stolen or damaged luggage, and approved medical conditions..jpg)

NHF Details

Decent Performance in FY19: nib Holdings Limited (ASX: NHF) is primarily engaged in the business of underwriting and distributing private health insurance to ANZ residents and international students as well as visitors to Australia. As on January 6, 2020, the market capitalisation of NHF stood at ~A$2.92 billion. The company announced a decent set of numbers for FY19 at the back of solid growth throughout all the business segments along with an increase in underlying operating profit (or UOP) of 9.2% to $201.8 million. Notably, the company’s earnings per share (statutory) (or EPS) rose by 11.9% to 32.9 cps. The company added that private health insurance has been playing a crucial role in Australia’s and New Zealand’s healthcare systems. In Australia, insurers finance a lion’s share of around 5 million hospital admissions (about 40% of total) and around 60% of all surgery. In FY19, nib’s arhi business managed to pay $1.4 billion in benefits for 281,757 hospital admissions and more than $373 million for dental procedures across Australia.

As a result of decent performance in FY19, the company has declared a fully franked full year dividend of 23.0 cents per share, which implies an increase from FY18 dividend of 20.0 cents per share. This consists of final dividend amounting to 13.0 cents per share. The market participants need to note that full-year dividend reflects 70% of FY19 NPAT, which happens to be consistent with the company’s dividend payout ratio of 60%- 70% NPAT. The company’s key personnel stated that considering the current market trading conditions, NHF has maintained current FY 2020 guidance, and it has reiterated arhi’s net margin which was anticipated to be around 6%. For the company, FY19 was a successful year which implies sound execution of the company’s business strategy, member-first focus and capability across the entire organisation. For FY19, the company posted a net profit after tax (or NPAT) amounting to $149.3 million, reflecting a rise of 11.8%. Its net investment income stood at $36.1 million (which was up 22.0%). The company’s performance has been delivering decent returns for its shareholders. This can be evidenced by the fact that, since listing on ASX in late 2007, the total shareholder return stood at 1,701% as compared to 66% for ASX 200.

Moving forward, there are expectations that fall in gearing ratio, decent operational capabilities and sound business strategies which primarily focuses on growing the core and economies of scope might act as tailwinds for long-term growth..png)

FY19 Results (Source: Company Reports)

Top 10 Shareholders: The following table provides a broader overview of the top 10 shareholders in NHF:.png)

Top 10 Shareholders (Source: Thomson Reuters)

Debt/Equity Ratio Falls YoY: The company’s Debt/Equity ratio stood at 0.37x in FY19, which reflects a fall from FY18 figure of 0.41x. In FY19, NHF’s long-term debt to total capital stood at 26.8%, which is lesser than FY18 figure of 29.1% and, therefore, it can be said that the company has reduced its reliance on long-term debt. Generally, lower exposure towards long-term debt places the company in a better position to make deployments towards strategic growth objectives, which could help it in achieving long-term growth.

.png)

Key Ratios (Source: Thomson Reuters)

Establishment of JV With Cigna: The group recently made an announcement about the creation of the specialist healthcare data science and services company, having a specific purpose of delivering better health outcomes generally for members as well as communities. The JV initiative between nib and Cigna Corporation would result in each contributing AUD$10 million in the start-up funding. It was added that JV would operate independently of nib and be led by Rhod McKensey. The purpose of joint venture revolves around 1) Analysing and interpreting the underlying individual disease risk, 2) Providing guidance on how risk could be best prevented, mitigated, managed or treated, and 3) Delivering healthcare programs, services and interventions which are relevant to disease risk profile.

Announcement of Lowest Premium Change: After the approval from Federal Minister for Health, NHF would be increasing health insurance premiums by an average of 2.90% from April 1, 2020. The company’s key personnel have stated that record low premium increase implies the company’s commitment towards keeping health insurance affordable.

Decent Growth in UOP in arhi Business: As per a recent presentation to Macquarie Securities Private Health Insurance Meetings, the company updated about its arhi (or Australian Residents Health Insurance) business. In FY15, arhi business posted UOP amounting to $71.9 million while in FY19 the figure increased to $149.5 million, reflecting a CAGR of 20.1%. .png)

5 Year Performance of arhi Business (Source: Company Reports)

In another release, the company stated that, though NHF has been expanding and diversifying, its “flagship” arhi business managed to account for the bulk of the total group earnings, as the business has contributed $149.5 million or just under 75% of the group UOP (or underlying operating profit).

Well-Positioned to Tap Opportunities: NHF’s net investment income witnessed an improvement of $1.5 million on the back of favourable equity performance in its growth portfolio. There has been a decrease in the gearing ratio that implies a rise in retained earnings as part of the company’s planned organic capital accumulation. The following image describes the company’s performance with respect to its key metrics:.png)

Key Parameters (Source: Company Reports)

The company witnessed a rise of 2.6% in FY19 on the YoY basis in its net cash flow from operating activities and, therefore, it can be said that NHF is possessing decent operational capabilities. Notably, the company’s dividend payout ratio has been improved by 150 basis points (or bps) in FY19 on the YoY basis and, thus, it looks like NHF has improved its focus on delivering returns to its shareholders. At the end of FY19, the company’s cash at bank and cash on hand stood at $124.2 million which reflects a rise from FY18 figure of $88.7 million. Considering a reduction in the company’s gearing ratio and increased cash, there are expectations that the company is capable enough to tap the opportunities which might arise moving forward.

What to Expect From NHF: The group has reaffirmed the financial year 2020 (or FY 2020) underlying operating profit guidance of a minimum $200 million (and statutory operating profit of minimum $180 million). In FY19, the company added that overall hospital inflation stood at 3.2% that represents a combination of the episode growth as well as episode price inflation and the significant risk equalisation contribution. As was expected, mental health waiver played a significant role in inflation, with regards to utilisation and costs per episode. However, the impact is anticipated to moderate in FY 2020. On February 24, 2020, the company plans to release FY 2020 interim results. The company stated that there are anticipations that the financial conditions as well as performance in other Group businesses might be consistent with recent years. Moreover, the ordinary dividend payout ratio is expected to come in the range of 60% – 70% of the full-year NPAT..png)

Guidance for FY 2020 (Source: Company Reports).png)

Key Valuation Metrics (Source: Thomson Reuters)

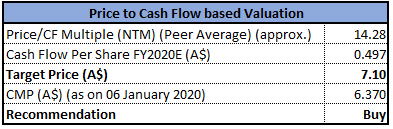

Valuation Methodology: Price to Cash Flow Based Valuation

Price to Cash Flow Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: In the span of the previous one year, the company’s stock has delivered a return of 23.03%. The company’s objectives when it comes to managing capital revolve around safeguarding the ability to continue as a going concern. This is because it plans to continue to provide returns for the shareholders and benefits for other stakeholders. Moreover, it plans to maintain an optimal capital structure so that cost of capital can be reduced. Between FY15- FY19, the company’s net premium revenues have witnessed a CAGR of 9.39% while gross margin has encountered a CAGR of 18.58%. During the same period, its NPAT has witnessed a CAGR of 18.66% which can be considered at decent levels. Based on the foregoing, we have valued the stock using a relative valuation method, i.e., P/CF multiple, and arrived at a target price of lower double-digit growth (in percentage terms). Hence, we give a “Buy” recommendation on the stock at the current market price of A$6.370 per share (down 0.624% on 06 January 2020).

NHF Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...