Company Overview - NEXTDC is engaged in the development and operation of independent data centers in Australia. As a provider of Data-Centre-as-a-Service, it is focused on helping its customers efficiently manage their information technology (IT) infrastructure stored in its data centers. Through its data centre management portal, ONEDC, one can manage entire service with it, across multiple data centre facilities, in real-time, from any Web-enabled device. It is also available as an app for iPhone. ONEDC provides real-time information about each rack, including current power consumption against allocation; balance of power drawing against A and B feeds; rack temperature, and log of access history, including person, date and time. In December 2013, NEXTDC announced that the solar array on its M1 data center in Port Melbourne is operational.

Analysis - NEXTDC (NXT), the provider of Data-Centre-as-a-Service, has been in discussion since it came out with its financial results for 1H15 ended 31 December 2014. The result has shown to beat the consensus. Particularly, the Company witnessed strong net sales growth yielding positive EBITDA and operating cash flow. The first period of positive EBITDA with $3.0 million (first positive figure ever recorded) was achieved in comparison to $3.4 million loss of 1H14 while the operating cashflow was $2.2 million in comparison to $3.9 million outflow in 1H14. The Company also reported statutory net loss of $5.8 million as opposed to $7.3 million net loss witnessed in the half year ended 31 December 2013. NXT has a cash and term deposits of $62.3 million at 31 December 2014. The market capitalization of the Company has been found to be $486.75 million.

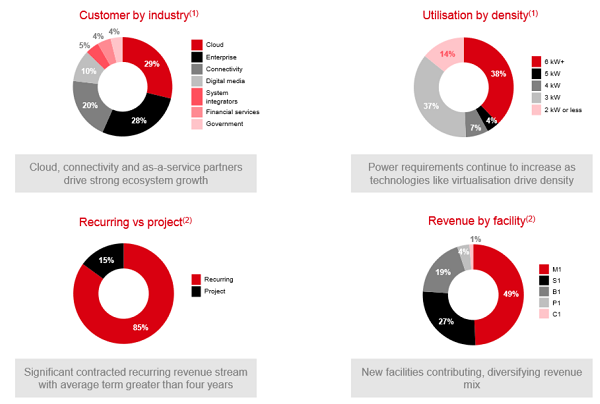

1H15 Highlights (Source – Company Reports)

NXT reported that its data centre revenue surged 134% to $26.7 million in comparison to $11.4 million reported in 1H14. 164% increase in new sales of 2.5MW from 940kW of 1H14 was another high point. The 2.5MW of power contracted included 1MW to an international customer for S1 Sydney. As understood, the international customer is contracted to take 1 MW of capacity at initial stage and can be allowed to take up 1.4 MW (term of the contract is three years). The Company further stated that billing with regards to the contract is believed to start from April 2015, which will help contributing to FY16 earnings.

118% rise in interconnection to 2,198 as at 31 Dec 2014 were over 1,006 reported in prior corresponding period. 48% rise in annualised contracted recurring revenue to $51.8 million and 35% rise in annulised unweighted pipeline to $172 million have been reported. Addition of further capacity in S1 Sydney and P1 Perth seems to be beneficial. Further, NXT highlighted that Project Plus is expected to enhance the originally planned network capacity of 35.35MW to about 42MW. The Company reported that the financial performance has been indicative of contribution from all five operating data centres. There was no data centre development revenue earned during 1H15. In terms of the facility capacities and contracted utilization, the third data hall was reported to be under construction which is capable of adding 2.8MW with regards to S1 Sydney. For P1 Perth, the first data hall expanded to 1.4MW while the second data hall is under construction which will add a further 1.4MW. At C1 Canberra, additional rack ready capacity has been added.

During the AGM last year, the Company charted a positive outlook in view of the bettering performance of its channel partners. Specifically, channel sales through Telstra have been estimated to be upgraded in 2H15 which seems to be a good sign. NXT’s partnership with Telstra aids Telstra customers to move IT infrastructure into NXT’s data centre facilities. Further, NXT highlighted benefits emanating from the growing market with factors such as the fixed cost nature of its business. Overall, what we see is that the 1H15 results emphasize on the changeover NXT has been able to achieve to a profitable growth level from mere development level.

Lift in Revenue and Utilization Levels (Source – Company Reports)

Among other developments, the Company also recently announced for the signing of an agreement with Microsoft for direct cloud connectivity to Microsoft Azure via ExpressRoute from NXT’s data centres in Melbourne, Sydney, Brisbane, Canberra and Perth. The ExpressRoute service is expected to be available from NXT data centres starting Q2 of calendar year 2015. This service would result in high-end security, lower network costs and better performance and reliability as it connects NXT customers to Azure through high-speed, secure, and low latency fibre connection. This entire arrangement would help both the companies integrate the cloud and data centre strategies. NXT is primarily expected to benefit from new opportunities of hybrid cloud computing models.

Industry and Market Drivers (Source – Company Reports)

The Company is poised to benefit from increasing demand for data centre capacity. This demand seems to be steered by exponential growth in internet traffic and the inclination towards hybrid solutions. The evaluation of opportunities utilizing higher density spaces within the current infrastructure is a part of NXT’s continual efforts. This seems to provide a competitive edge over peers.

Diversified Recurring Revenue Model (Source – Company Reports)

With the aforementioned strong results, the Company has updated its guidance and the outlook now provided by NXT is quite encouraging with current utilization levels and further expansion anticipated for new client contract base in 2H15. FY15 is expected to be characteristic of total new sales ranging between 3.4MW and 4.0MW reflecting a good surge from 2.1MW of FY14. The data centre revenue is expected between $55 million and $60 million while we noted that FY14 witnessed $30.4 million revenue only. The capital investment on plant and equipment is anticipated to be between $35 million and $42 million. The fixed costs excluding power and consumables are estimated to be between $44 million and $46.5 million which is a slight increase from $42.6 million of FY14. FY15 EBITDA is expected to be between $6 million and $8 million as opposed to the $16.1 million underlying EBITDA loss in FY14. Although, the Company has not paid dividends during the last 12 months in view of the earlier results, the situation may change given the current trend of upsurge.

Of course, we understand that NXT needs to be wary of risks related to revenue ramp-up, operational failures due to unexpected service disruptions and/or outages, technology, and competition from existing or new entrants to the data centre segment. Further, the Company looks to execute its strategy well but we also note that about 60% of the planned capacity is still to be sold indicating a lot more effort required to move up the ladder.

FY15 Outlook (Source – Company Reports)

Nonetheless, the operational leverage along with improved quality of earnings under the shed of promising industry outlook seems to be advantageous for the Company. We expect that NXT is moving towards a positive momentum phase through FY15 given the evolving and favorable ecosystem entailing new contract wins, and recent developments and agreements.

NXT Daily Chart (Source - Thomson Reuters)

In view of the aforementioned, we put a BUY recommendation for this stock at the current price of $2.41.

.png)

.png)

.png)

.png)

Please wait processing your request...

Please wait processing your request...