Kalkine has a fully transformed New Avatar.

.png)

A deep contraction in the global economy due to the containment measures for COVID-19 has increased the uncertainty surrounding future events that will lead to recovery. The restrictions imposed have hit the output, supply chains, household income, and, in turn, consumer spending, posing a big challenge to economic growth until full recovery. Considering the present COVID-19 situation around the world, anticipating the timing for ease of restrictions is highly uncertain.

Economic Outlook for Australia: The RBA issued the economic outlook in the recently released Statement on Monetary Policy, wherein it anticipates a decline of 10% in Australia GDP over the first half of 2020 and has forecasted an unemployment rate of ~10%. Headline inflation is also expected to decline largely due to the impact of lower fuel prices and free child-care. Economic outlook beyond the first half remains dependent on how long the containment measures pertaining to COVID-19 will last. As soon as the restrictions imposed on economic activity begin to relax, businesses will resume operations, leading to employment creation. Moreover, household spending will also increase as the situation stabilizes. However, deciding the timing and magnitude of these events remains a tough call due to the uncertainty about government decisions with respect to the lifting of COVID-19 related restrictions. Meanwhile, the concerned authorities are working proactively to protect the economy from deteriorating. The Reserve Bank has implemented a comprehensive package of measures to support the economy and to ensure better functioning of key financial markets. The banking system in Australia was provided additional liquidity of $50 billion by the beginning of April 2020 to support businesses and households. Moreover, the government is working to mitigate the negative impact of the virus and has provided relaxation in certain key areas of economic activity.

Inflation for the March Quarter, Majorly Driven by Food and Oil Prices: Inflation pressures had picked up a little in the March quarter, as prices went up 2.2% over the year to the March quarter, and 1.75% in underlying terms, as food prices, especially vegetables, witnessed a significant rise out of all the CPI baskets. However, oil prices fell significantly due to lower global demand and limited storage capacity, which could not be controlled by the recently announced production cuts.

What to Expect: As per the recent guidelines and expectations of RBA, with the plunge in oil prices and the temporary removal of childcare fees, year-ended headline inflation is expected to turn negative in the June quarter, for the first time since the early 1960s. Trimmed mean inflation is also expected to go down in the June quarter and is expected to be around 1.5% over the year. Therefore, in the near-term, inflation is expected to remain low due to a decline in a number of prices. However, there is a possibility of a twist with respect to headline inflation if the anticipation regarding the oil prices remaining subdued is contradicted by a rebound in the oil market. In such a scenario, the expectations of a dip in headline inflation, as stated above, become a matter of doubt.

Factors Shaping the June Quarter Figures: In the March quarter, there was a sharp decline of 6% in automotive fuel prices, which have continued into the June quarter due to subdued demand. As per the current scenario, the RBA expects automotive fuel prices to subtract one percentage point from headline CPI in the June quarter. Moreover, recent policy decisions by the government in response to the pandemic, including the introduction of free child care services from early April to end June and waiver of preschool fees, are expected to reduce CPI inflation by around 1.5% in the June quarter. Deferment of private health insurance premiums will lead to lower medical & hospital services inflation in the June quarter. Although the housing related inflation increased slightly in the March quarter, reduced demand for rental properties and rent reductions will impact the rent inflation for the quarter. Moreover, demand for newly built dwellings is also expected to remain weak which will again impact housing inflation.

In the retail sector, prices increased in the March quarter for non-durable household goods such as toilet paper and cleaning products, as consumers started hoarding essential products. Food products also witnessed a rise in prices as a result of increased demand from consumer stockpiling and supply disruptions due to bushfires and drought. Prices for cereal products such as pasta and rice and meat products remained high. As the above products form the essential daily requirements of the households, prices for such baskets will mostly help in driving the inflation up..png)

Consumer Durables and Food Price Inflation (Source: RBA)

Recovery in Different Scenarios: In the baseline scenario, which involves the relaxation of domestic activity restrictions over coming months, with most of these restrictions lifted by the end of the September quarter, as described by the RBA, activity and employment will begin to recover in the second half of the year, which is likely to provide a gradual uplift to inflation, due to slower growth in wages and labour costs, low demand for housing and weak rent growth.

However, considering Australia’s progress in dealing with the outbreak, flattening of the curve and a relatively sharp decline in COVID-19 cases, the central bank also considers a scenario, wherein the restrictions may be relaxed a little sooner, providing a faster boost to the economy than the baseline scenario. In such a case, the unemployment rate could return to around 5% in a couple of years and GDP numbers would also change for the better.

Alternatively, the outcomes would be even more challenging than those in the baseline scenario if relaxation is delayed or the restrictions are re-imposed. Recovery in the unemployment rate would slow down, which will lead to more job losses and business failures.

The RBA would continue to keep funding costs low in Australia and credit available to households and businesses. It is committed to support jobs, incomes and businesses during this difficult period and will not increase the target cash rate until any progress is made towards full employment. It is confident about keeping the inflation sustainably within the 2–3 percent target band. Looking at the current market conditions and the impact on prices, as discussed above, some stocks in Australia are offering decent prospects for growth and can be a good pick at the current levels. Let us have a quick look at the performance of these four stocks.

1. Kathmandu Holdings Limited (Recommendation: Buy, Potential Upside: Low Double-Digit)

(M-cap: A$ 620.38 Million, Annual Dividend Yield: 16.41% (price correction led Div. Yield increase))

A Surge in Online Sales: Kathmandu Holdings Limited (ASX: KMD) is engaged in the retail of clothing and equipment for travel and adventure. On 5th May 2020, the company provided a business update, stating that it has witnessed a rise in online sales from the last year, with the highest growth reported in Australia. Growth strengthened over April as consumers switched to the online mode of shopping. The company’s digital infrastructure and supply chain investments over the last three years supported in ramping up online trading capabilities and distribution capacity in the face of unprecedented online demand. Recently, the company has also reopened most of its Kathmandu and Rip Curl stores in New South Wales and Queensland, with strict safety protocols. During the six months ended 31st January 2020, the company reported revenue from continuing operations amounting to NZ$363.65 million, up 56.7% on pcp.

Outlook: Going forward, the company will remain strategically focused on brand, product and customer, and will work to add further diversification across the platform, along with the continued digital transformation. The company has a business supported by iconic brands in the global outdoor and action sports market and has the capability to get through a difficult period and come out on a stronger footing.

The company enjoys an excellent position in the global outdoor and action sports segment, which is evident in the rise in online sales after the closure of physical stores. Despite a challenging external environment, the company kept up to its customers’ expectations by catering to the rising demand through its digital capabilities. As soon as the panic subsides and containment measures with respect to COVID-19 are relaxed, the company plans to open its stores and drive sales prospects for long-term growth. High-quality products along with a set of loyal customers will help the company sail through difficult times and will favourably impact its performance in the long run..png)

Valuation Methodology: EV/Sales Multiple Based Relative Valuation (Illustrative).png)

EV/Sales Multiple Based Approach (Source: Refinitiv, Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months.png)

A-VIX vs KMD (Source: Refinitiv, Thomson Reuters)

Stock Recommendation: The stock of the company gave positive returns of 41.13% in the past one month and is currently inclined towards its 52-week low price of $0.469. The stock saw a sharp decline in March due to a spike in market volatility after the outbreak of coronavirus. Since then, the stock has begun to stabilise and can be a good pick at current trading levels. Moreover, the business has demonstrated a resilient performance despite subdued demand and reported a surge in online performance, which increase the optimism regarding KMD’s performance. The company’s portfolio of excellent brands will continue to be in high demand from loyal customers. Considering the above factors, we have valued the stock using EV/Sales multiple based illustrative relative valuation method and arrived at a target price with an upside of low double-digit (in percentage terms). Hence, we give a “Buy” recommendation on the stock at the current market price of $1.010, up 15.429% on 11th May 2020.

2. Santos Limited (Recommendation: Buy, Potential Upside: Low Double-Digit)

(M-cap: A$ 10.1 Billion, Annual Dividend Yield: 3.39%)

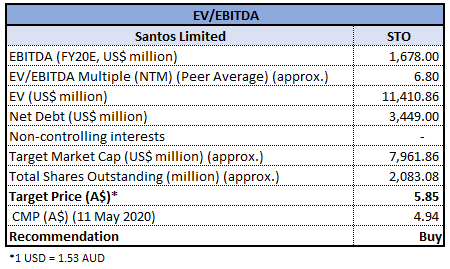

Strong Balance Sheet Position: Santos Limited (ASX: STO) is engaged in the exploration and the production of gas and petroleum. During Q1FY20 ended 31st March 2020, the company reported a strong operating performance, with free cash flow amounting to US$265 million, highest Cooper Basin gas production in 9 years, and GLNG (Gladstone LNG) produced at an annualised rate of 6.4 mtpa. In a lower oil price environment, the company ensured that production levels from its current assets are relatively steady for the next four or five years without any new growth projects. During the first quarter, the company’s oil assets performed well with strong realised prices for the period.

Outlook:In response to COVID-19, the company has taken strict financial measures to mitigate the risk to performance. Capital expenditure for 2020 is now expected to go down by US$550 million and cash production costs by US$50 million.

In a low oil price environment, oil players across the world have faced several challenges due to a massive decline in demand and prices. Santos Limited possesses a disciplined, low-cost operating model, which will help the company to maintain a stable ground during challenging times. The company has laid a strong foundation to fight the current environment and is well-positioned to leverage the opportunities when the market recovers. While the RBA does not talk about a possible recovery in oil prices and the subsequent impact on headline inflation, a scenario where the oil market rebounds in the near term will be a relief to the world’s oil players and the economy as a whole.

The company’s performance in the first quarter has laid a strong base for future performance and will help it to derive the best benefits out of such a scenario..png)

Valuation Methodology: EV/EBITDA Multiple Based Relative Valuation (Illustrative)

EV/EBITDA Multiple Based Approach (Source: Refinitiv, Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

A-VIX vs STO (Source: Refinitiv, Thomson Reuters)

Stock Recommendation: The stock of the company gave positive returns of 9.23% in the last one month and is currently trading below the average of its 52-week low and high of $2.730 and $9.070, respectively. The company has a strong balance sheet with more than US$3 billion of liquidity and significant pricing protection for 2020, with around 70% of 2020 forecast production volumes comprising of either fixed price domestic gas sales contracts or oil hedged at an average floor price of US$39/bbl. Its low-cost operating model will continue to act as a key growth driver for Santos Limited. Although the stock price has been under pressure due to oil market conditions and has also declined in response to a highly volatile market led by COVID-19, a resilient business may support a speedy recovery as market conditions improve. We have valued the stock using EV/EBITDA multiple based illustrative relative valuation method and arrived at a target price with an upside of low double-digit (in percentage terms). Hence, we give a “Buy” recommendation on the stock at the current market price of $4.94, up 1.856% on 11th May 2020.

3. Asaleo Care Limited (Recommendation: Speculative Buy, Potential Upside: Low Double-Digit)

(M-cap: A$ 553.98 Million, Annual Dividend Yield: 1.96%)

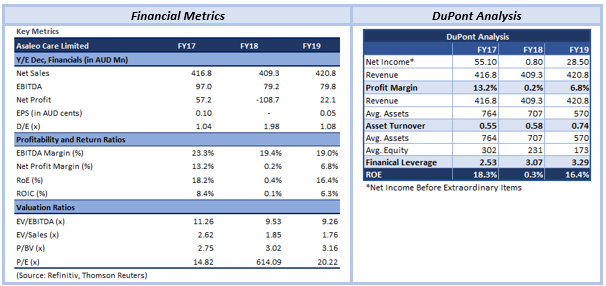

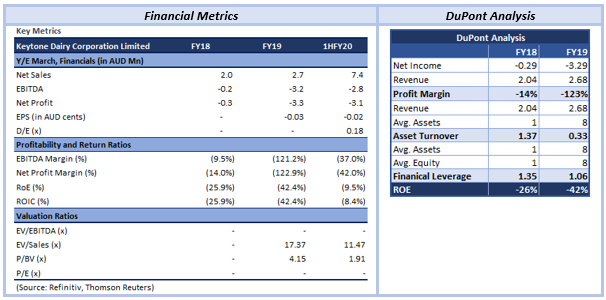

Robust Development Pipeline: Asaleo Care Limited (ASX: AHY) manufactures, markets, distributes and sells personal care and hygiene products. During the year ended 31st December 2019, the company reported revenue amounting to $420.2 million, up 3% on the prior corresponding year. Underlying EBITDA and underlying NPAT stood at $82.4 million and $31.7 million, respectively. Net profit from continuing operations increased substantially and stood at $28.5 million. During the year, the company increased investment in sales and marketing to drive future growth and is committed to bring to market world-leading innovation, research and technology, marketing materials and a pipeline of new product development for its key brands.

Outlook: During FY19, the company strengthened its balance sheet by selling the Australian Consumer Tissue business, hence reducing its debt. In 2020, the company aims to build on this momentum to launch more new products, continued investment in brands and delivering on new contract wins. For FY20, the company expects underlying EBITDA to be in the range of $84 - $87 million.

The company’s Retail segment delivered strong revenue growth during the year, with volume and value growth across most of the categories. Amid the rising impact of coronavirus, the preference for hygiene products has increased, signalling sales growth prospects. With the changing requirements of consumers, the sector calls for introduction of new products to cater to the rise in demand. Asaleo Care’s growth in FY19 was driven by increased brand investment and new product launches from a strong development pipeline, including TENA Discreet and Ultra-Thin Pads launched under the incontinence retail segment. With increasing awareness and need for cleanliness and sanitary products, Asaleo Care’s products are expected to remain in high demand. From a macro perspective, prices of these products are expected to have a positive near-term impact on inflation.

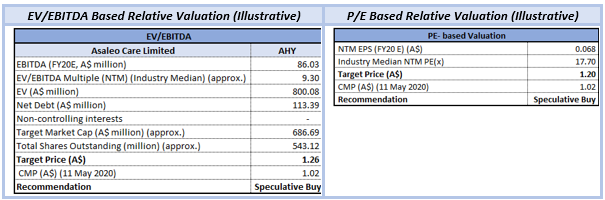

Valuation Methodologies:

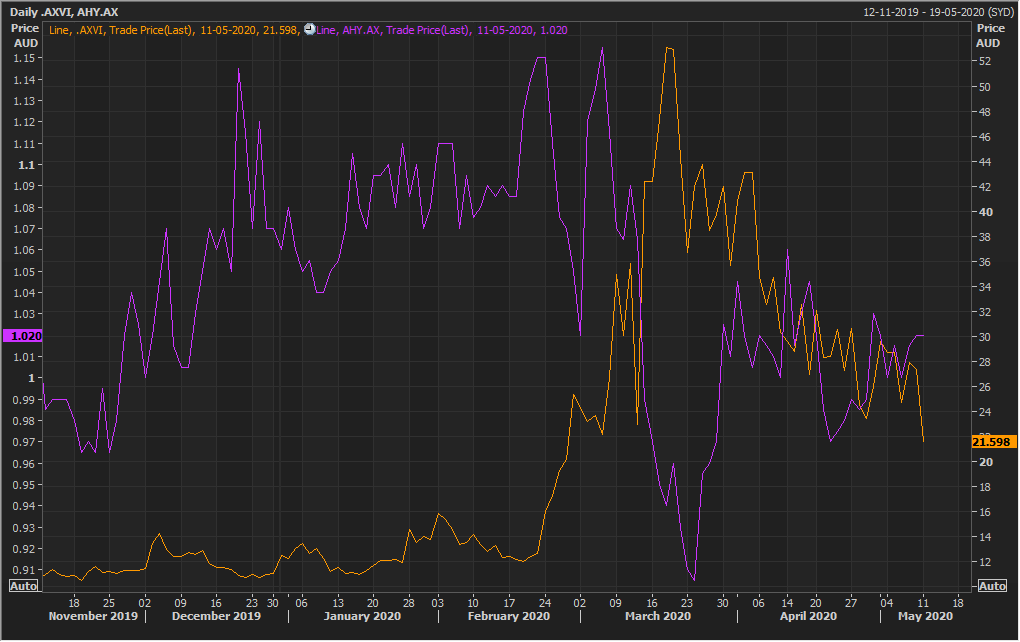

A-VIX vs AHY (Source: Refinitiv, Thomson Reuters)

Stock Recommendation: The stock of the company corrected by 5.12% in the past 3 months. The company has a strong portfolio of essential consumer products and focuses on innovation, driven by consumer insight. It possesses a pipeline of world-leading research, development and innovation, that will act as a key catalyst for growth. After witnessing a steep fall due to a spike in market volatility, the stock has demonstrated impressive recovery on the back of the resilient nature of the business and robust fundamentals. The company’s business rides on the wheels of continued innovations and development initiatives and has decent prospects for growth, going forward. We have valued the stock using P/E and EV/EBITDA multiple based illustrative relative valuation method and arrived at a target price with an upside of low double-digit (in percentage terms). Hence, we give a “Speculative Buy” recommendation on the stock at the current market price of $1.020 as on 11th May 2020.

4. Keytone Dairy Corporation Limited (Recommendation: Speculative Buy, Potential Upside: Low Double-Digit)

(M-cap: A$ 75.29 Million)

Robust Increase in Demand: Keytone Dairy Corporation Limited (ASX: KTD) is an established manufacturer and exporter of formulated dairy products and health and wellness products. During the quarter ended 31st March 2020, the company reported record quarterly sales, approximately 20 times higher than those of the prior corresponding quarter. The company’s business was positively impacted by COVID-19, with demand for its products rising substantially. The company continued to grow its Asian and Chinese businesses, with substantial new orders from China, including repeat and larger orders from Walmart China. Sales revenue for the quarter was reported at $8.7 million, as compared to $0.5 million reported in pcp. Total customer cash receipts increased to $8.4 million.

The company has recently released an announced about binding commitments for a placement raising $12.5 million, to accelerate its growth initiatives, including sales and marketing of key products, execution of strategic acquisitions, working capital requirements, etc. In addition, the company has also entered into an agreement to acquire AusConfec Pty Ltd for $2.25 million, adding to its product development capabilities and expanding its client base.

Outlook: The company is set to cater to the demand for dairy products, which has increased approximately four times than prior to the outbreak of COVID-19. Results of the rise in demand will be reflected in the coming quarters, as the company commenced operations at its second manufacturing facility to meet the additional demand. Moreover, the company will shortly re-launch its KeyDairy Whole Milk and Skim Milk Powders to better align with customer trends and boost sales.

While the global market has been a victim of various challenges due to COVID-19, the company has been classified as an essential service by the Australian and New Zealand governments and has continued to sustain its impressive growth without disruption. The demand trend continued into the June quarter, with KTD recording significant orders in the first weeks of April 2020 in excess of $A5.2m, due to be filled in the next quarter. Therefore, with favourable industry trends amid the pandemic, the company seems well-positioned to drive growth with a growing distribution footprint, development of its suite of own-branded products, and additional roll-out of a significant new product development pipeline. Moreover, the rise in prices for food and non-alcoholic beverages during the March quarter, signal an optimistic future for the company. This, in turn, will positively impact food inflation in the near-term.

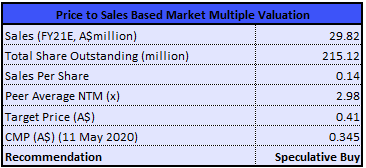

Valuation Methodology: Price to Sales Based Market Multiple Valuation (Illustrative)

Price to Sales Based Market Multiple Valuation (Source: Refinitiv, Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

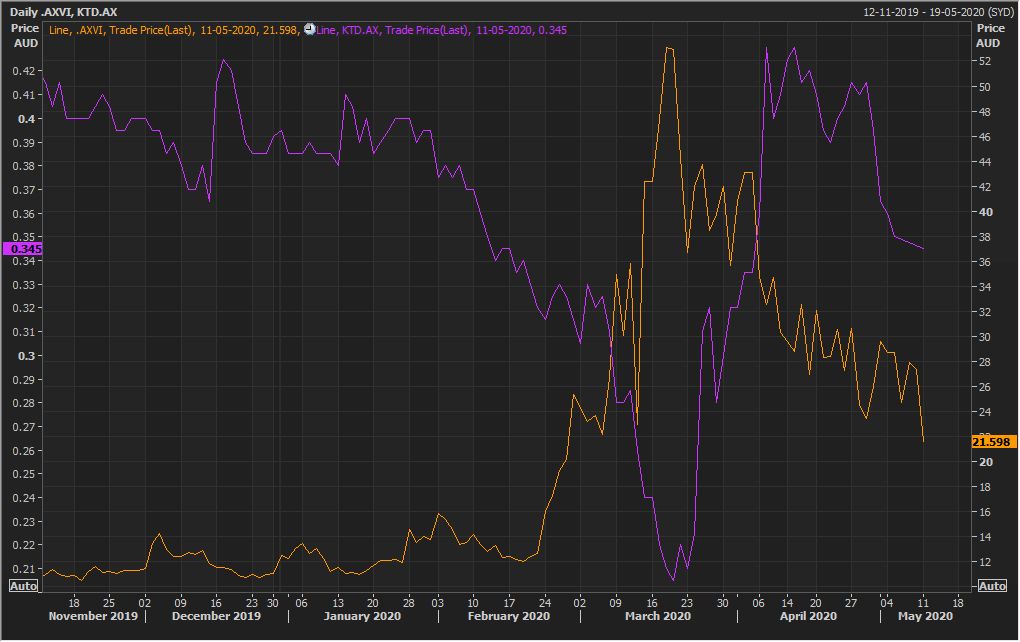

A-VIX vs KTD (Source: Refinitiv, Thomson Reuters)

Stock Recommendation: The stock of the company corrected by 20.45% and 21.35% in the last 6 months and1 year, respectively. As discussed in the above section, the company has seen a positive impact on the business after the outbreak of coronavirus, as demand for its products continued to rise substantially. After the market reacted to the outbreak, the stock price experienced a decline in the first place. However, as the situation improved, the stock picked an excellent pace and has shown favourable recovery since then. Moreover, the increase in demand across the dairy industry and a strong business position will act as key catalysts for driving growth, going forward. We have valued the stock using Price/Sales based market multiple and arrived at a target price with an upside of low double-digit in percentage terms. For the purpose, we have considered the peer group - Bega Cheese Ltd (ASX: BGA), Freedom Foods Group Ltd (ASX: FNP), United Malt Group Ltd (ASX: UMG), A2 Milk Company Ltd (ASX: A2M), Bubs Australia Ltd (ASX: BUB), and Beston Global Food Company Ltd (ASX: BFC), which comes under Food Processing segment. Hence, we give a “Speculative Buy” recommendation on the stock at the current market price of $0.345, down 1.429% on 11th May 2020.

.JPG)

Comparative Price Chart (Source: Refinitiv, Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...