Kalkine has a fully transformed New Avatar.

Company Overview: National Australia Bank Limited is a business bank engaged in providing personal banking and business banking services. The Company's segments include Business & Private Banking, Corporate & Institutional Banking (CIB), Consumer Banking & Wealth Management, Customer Products & Services and NZ Banking. The Company’s Business & Private Banking focus on medium enterprises (SME) customers, which include NAB business franchise with specialized agriculture, health, Government, education and community services along with private banking and small business segment. CIB includes corporate and institutional banking businesses, fixed Income, currencies and commodities (FICC), capital financing businesses, asset servicing and international branches. Customer Products & Services include banking & wealth products, strategy, digital, NAB labs/ventures, marketing and corporate affairs. Consumer Banking & Wealth Management includes the distribution components of wealth management.

.png)

NAB Details

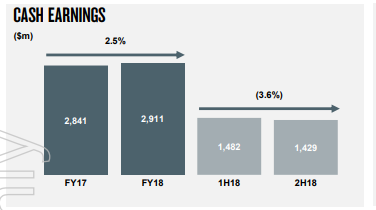

Transformation on Track Amidst Challenges in FY 2018: National Australia Bank (ASX: NAB) happens to be one of the big four banks of Australia with the market capitalization of circa $68.38 billion as of 7 February 2019. The bank had witnessed a rise in net interest income of 2.5% in FY 2018 on the YoY basis, however, the bank’s net interest margin happens to be flat and was 1.85% in FY 2018 as compared to FY 2017. On the analysis front, efficiency ratio stood at 51.9% in FY 2018 which implies the fall of 0.1% on the YoY basis and lower than the industry average of 52.0%. This reflects that the bank has been broadly efficient to earn more than its spending. We expect that the bank’s strategy of utilizing the assets would support it moving forward. The bank enjoys healthy balance sheet and strong asset quality with improved 90+ days past due and gross impaired assets to gross loans and acceptances of 0.71% as at 30 September 2018 as compared to the prior year wherein it was as at 0.70%. Moreover, the company is paying a healthy dividend regularly to its shareholders and maintains a respectable return ratio over the past few years. NAB has been maintaining stable NIMs from the past five years and, moving forward, it might improve because of lesser funding costs. Its net margin might also further improve given its focus on cost improvement initiatives.

The group also reported its first quarter 2019 updates wherein cash earnings were up 2% on 2H quarterly average but the same dropped by 3% against 1Q18. While the net margin slipped owing to challenged housing lending scenario, the expenses also fell by 3% given productivity initiatives. Overall, the revenue was more or less stable and unaudited statutory net profit moved up to $1.70 billion. Meanwhile, chief executive Andrew Thorburn and chairman Dr Ken Henry have resigned while they were under the Royal Commission radar. The group has however, indicated to restructure the base for filling in its capability gaps as NAB board member Philip Chronican, well known in the industry for good work, will serve as interim CEO.

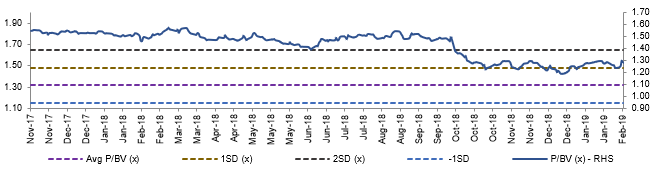

Over the past few years, the bank has witnessed a roller coaster ride when it comes to the stock performance on the back of sectorial headwind in relation to Royal Commission issue and macroeconomic factors, etc. Currently, NAB is trading at P/BV multiple of 1.26x which is below to five years’ average of 1.47x, and thus proffers an attractive opportunity to investors at the current juncture. Keeping the view of a decent outlook in the business along with mixed challenges, we have valued the stock based on 1-year forward P/BV multiple to FY20E consensus Book Value Per Share (BVPS) of $19.81; and 1-year forward P/E multiple to FY20E EPS of $2.1 (discounting the consensus EPS owing to latest commission report which might impact the bottom line numbers in near future). Given the discounted estimation in the above methodologies, we expect target price upside of single high-digit to low double-digit growth (in %). Key risks are regulatory risk, credit risk, liquidity risk, security risk, etc.

.png)

Key Financial Metrics (Source: Company Reports, Thomson Reuters)

Management’s Views on Royal Commission’s Final Report: The top management of National Australia Bank had stated that the final report would bring the changes in the industry as well as profession which would be beneficial for the customers. The bank’s management had stated that they are in the process of making sustainable as well as serious change so that the customers’ trust can be regained. It can be said that the management has maintained their focus on improving operations of the bank which could support it in the long-term and can cater to different needs of the customers. We expect that the bank’s initiatives or plans would support it in the gaining the trust of the market players. The bank would be putting the customers’ first which might provide the broader support to the bank’s operations.

How RBNZ’s Guidelines can affect NAB: Earlier, the Bank had issued a release which contained information about the recent move initiated by Reserve Bank of New Zealand. The central bank of New Zealand has plans to increase the amount of capital that includes NAB’s New Zealand subsidiary, named Bank of New Zealand (or BNZ). The changes have an aim that it would strengthen the banking system of New Zealand which would also protect the depositors by reducing chances with respect to bank failures. The new requirements happen to revolve around:

Considering the above proposals which have been made by Reserve Bank of New Zealand and with reference to Bank of New Zealand’s balance sheet as at September 30, 2018, the recommendations reflect a potential rise in the Tier 1 capital of NZ$4 billion-NZ$5 billion for the Bank of New Zealand.

Elevated Operating Expenses Weighed Over NAB’s Consumer Banking and Wealth Segment: The cash earnings of Consumer Banking and Wealth Segment encountered the YoY fall of 5.8% to $1.53 billion because of higher operating expenses. However, it got partially offset by the growth in the balance sheet as well as repricing benefits with regards to housing lending portfolio. The bank’s operating expenses witnessed the rise of 4.7% to $3.04 billion largely because of increased investments. The segment’s risk-weighted assets encountered the rise of 1.0% to $79 billion because of growth in the housing lending volume.

.png)

Consumer Banking & Wealth (Source: Company Reports)

Credit Quality Improvement Supported NAB’s Corporate and Institutional Banking: National Australia Bank’s corporate and institutional banking segment’s cash earnings witnessed the rise of 0.4% on the YoY basis to $1.54 billion on the back of improvement with respect to credit quality. This got partially offset by a rise in the operating expenses. The bank stated that the revenues of corporate and institutional banking was broadly flat in FY 2018 on the YoY basis because of the unloading of private wealth business in the Asia, lesser trading income as well as bank levy’s full-year impact.

.png)

Corporate & Institutional Banking (Source: Company Reports)

New Zealand Banking’s Cash Earnings Supported by Increased Revenues: National Australia Bank’s New Zealand Banking segment witnessed a rise in the cash earnings of 6.7% to NZ$1 billion because of a rise in the revenues. However, it got partially offset by a rise in the expenses because of increased investments towards the business. This segment’s total risk-weighted assets witnessed the rise of 5.9% to NZ$61.2 billion.

.png)

New Zealand Banking (Source: Company Reports)

Balance Sheet Growth, Repricing Benefits Supported Business and Private Banking Segment: The cash earnings of Business and Private Banking Segment witnessed a YoY rise of 2.5% to $2.9 billion in FY 2018 on the back of growth in the balance sheet as well as benefits with respect to repricing in the lending portfolio. This got partially offset by elevated operating expenses as well as increased credit impairment charges.

The segment’s net interest income witnessed the YoY rise of 5.4% to $5.53 billion largely because of average interest earning assets, customer deposits as well as net interest margins. The division’s risk-weighted assets encountered a rise of 3.6% to $116.2 billion on the back of a rise in gross loans as well as acceptances.

Business and Private Banking (Source: Company Reports)

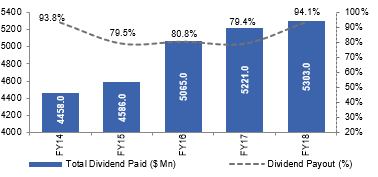

Higher Dividend Yield Compared to Broader Industry: National Australia Bank had declared the final dividend amounting to 99 cents per fully paid ordinary share which happens to be 100% franked. The bank keeps on adjusting DRP (or Dividend Reinvestment Plan) on the periodic basis. The bank had been consistent in declaring the dividends from the past few years. In FY 2018, it declared the dividend per share of $1.98. Since the bank had been declaring dividends at the consistent pace, we believe that it might attract the market players. The consistency clearly reflects that the bank had been focusing towards the benefits of the shareholders. Additionally, the bank happens to possess annual dividend yield of 8.04% which is higher than the broader industry (Banking Services) median of 6.4% which reflects that the bank has been efficient in declaring dividends as compared to the broader industry which could be a key catalyst for NAB moving forward.

Consistency in Dividends (Source: Company Reports)

Drivers for Future: Moving forward, National Australia Bank had stated that its transformation plan happens to be on track as well as it is making progress at the good pace despite challenging operating environment. In FY 2018, the bank had made significant deployments which are focused on giving better customer experience as well as reliable and resilient technology. The bank had also maintained its focus towards the agenda of simplification. In FY 2018, NAB had simplified its product offering. It stated that IT applications have witnessed a fall of 5% while 3% have been migrated to Cloud which led to the creation of flexible as well as lower cost technology platforms.

The bank stated that there are expectations of cumulative cost savings amounting to at least $1 billion by 30 September 2020, since the bank have been simplifying and automating the processes, reducing the procurement and third-party costs as well as they are getting closer to the customers with flatter organizational structure. We expect that the cost savings would support NAB moving forward and would also positively impact the margins. On the economic front, the outlook with respect to New Zealand as well as Australian economy is optimistic. The robust growth with regards to the population as well as lower unemployment has been limiting the risks from slowing housing cycle.

Historical P/BV Band (Source: Company Reports)

Stock Recommendation: In last six months, the stock has fallen 11.2% and is trading at decent PE multiple of 12.23x, indicating undervalued scenario at current juncture. From the technical analysis front, a technical indicator, Moving Average Convergence Divergence or MACD has been applied on the daily chart of National Australia Bank, and default values were used for the purposes. After careful observation, it was noticed that the MACD line has crossed the signal line and is trending in the upward direction signifying the bullishness. This reflects that the stock might witness upward momentum moving forward. Moreover, Exponential Moving Average or EMA has been applied and default values were used for the purposes. It was noticed that the stock price has crossed the EMA is trending in the upward direction which also signifies bullishness.

On the other hand, moving forward, the bank is expected to be supported by its cost-saving initiatives as well as stable NIMs. The bank is expected to be supported by the automation of the processes. Moreover, the higher dividend yield as compared to the broader industry might also act as a tailwind moving forward. Keeping the view of a decent outlook in the business along with mixed challenges, we have valued the stock based on 1-year forward P/BV multiple to FY20E consensus Book Value Per Share (BVPS) of $19.81; and 1-year forward P/E multiple to FY20E EPS of $2.1 (discounting the consensus EPS owing to latest commission report which might impact the bottom line numbers in near future). Given the discounted estimation in the above methodologies, we expect target price upside of single high-digit to low double-digit growth (in %). In view of the above backdrop of facts, we give a “Buy” recommendation on the stock at the current market price of A$24.930 per share (up 1.259% on 7 February 2019).

NAB Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...