Kalkine has a fully transformed New Avatar.

Company Overview: National Australia Bank Limited is a business bank engaged in providing personal banking and business banking services. The Company's segments include Business & Private Banking, Corporate & Institutional Banking (CIB), Consumer Banking & Wealth Management, Customer Products & Services and NZ Banking. The Company’s Business & Private Banking focus on medium enterprises (SME) customers, which include NAB business franchise with specialized agriculture, health, Government, education and community services along with private banking and small business segment. CIB includes corporate and institutional banking businesses, fixed Income, currencies and commodities (FICC), capital financing businesses, asset servicing and international branches. Customer Products & Services include banking & wealth products, strategy, digital, NAB labs/ventures, marketing and corporate affairs. Consumer Banking & Wealth Management includes the distribution components of wealth management.

.png)

NAB Details

Housing, Business Lending Aided National Australia Bank in FY 2018: National Australia Bank Limited (ASX: NAB) ended FY 2018 by generating net interest income or NII of $13.4 billion (on cash earnings basis) which implies the YoY growth of 2.3% after considering a decrease of $246 million during the year. This decrease got offset by movements in the economic hedges with regards to the other operating income. If this movement is excluded, a 4.2% rise in the NII was noted that got underpinned by the robust momentum in the business and housing lending volumes as well as lower liquidity and funding costs. However, the effect of the repricing which was done in the prior period and improved lending margins in New Zealand also aided the bank’s NII. This repricing was done in the business as well as housing lending portfolios in Australia. In our view, National Australia Bank Limited ticks most of the boxes that investors expect from banking companies. It has strong and stable NIMs, growing deposits and transactional accounts along with increasing lending business and decent dividend payout ratio in the range of 73% to 94% over the past few years. Therefore, we believe that NAB can sustain high P/BV multiple in years to come and reward the investors as the group chases to achieve APRA’s ‘unquestionably strong’ capital benchmark of 10.5% in an orderly manner by 1 January 2020 from 10.2% at the end of FY18. Currently, NAB is trading at PE multiple of 11.89x, which is marginally below peers, signifying undervalued scenario at the current juncture. Hence, we have valued the stock using 1 -year forward P/BV multiple and have arrived at the target price that may see an upside of the mid-single-digit to low double-digit with a higher side ascribing a valuation of 1.48x FY20E P/BV.

Key Financial Metrics:

.png)

Source: Company Reports, Thomson Reuters

Average Interest Earning Assets Underpinned Business and Private Banking’s NII: National Australia Bank’s business and private banking generated net interest income amounting to $5.5 billion which implies the YoY growth of 5.4% and was helped by the average interest-earning assets, net interest margins or NIMs and customer deposits. The average interest earning assets of the division was mainly supported by the robust business lending. However, NIMs were primarily helped by the repricing initiatives as well as favourable deposit costs whereas customer deposits were supported by the bank’s priority of focusing on quality deposits. Hence, we assume that the bank will continue to improve its average interest earning assets on the back of moderate rise in lending business in years to come.

.png)

Business and Private Banking division’s revenues and margin (Source: Company Reports)

What Has Been Prompting NAB for Increased Investment: National Australia Bank stated that the primary focus of higher investment revolves around the Best Business Bank. The bank has been focusing on the building as well as improving the ability to approve loans which might help it in the approval of approximately 80% of the SME loans. It plans to do so within 24 hours. With respect to the transaction accounts, the bank plans to work for the same day on-boarding. Moreover, it plans to expand the offerings of QuickBiz and is also working towards customer service by leveraging the digital capabilities.

A Quick Look at Consumer Banking and Wealth Division: The net interest income of National Australia Bank’s consumer banking and wealth division amounted to $3.9 billion which reflects a rise of 2.1% on the YoY basis because of elevated levels of customer deposits as well as average interest-earning assets. The division witnessed a decline in the NIMs of 7 bps or basis points because of the competitive pressures as well as changes which have been done in the housing lending product mix. The division’s net investment income witnessed a decline of 3.9% in FY 2018 on the YoY basis because of the margin compression as well as lower income. Further, the consumer banking and wealth division saw margin compression because of the business mix shift towards products which generate lower margins.

.png)

Consumer Banking and Wealth Division’s cash earnings (Source: Company Reports)

Analyzing the Impact of Market and Non-market Revenues on Corporate and Institutional Banking Business: National Australia Bank’s corporate and institutional banking division garnered net interest income amounting to $1.8 billion in FY 2018 which implies a fall of 4.6% on the YoY basis. If viewed from the broad perspective, this division witnessed stable result because of the elevated non-market revenues coupled with lesser credit impairment charges. However, these positive impacts were offset by the increased investment spending as well as lesser market revenues. The bank’s division recorded gross loans and acceptances amounting to $91.4 billion in FY 2018 reflecting the growth of 3.9% which implies a rise in corporate finance lending of $4 billion. Additionally, the division also saw a fall in other lending amounting to $2 billion which was mainly in mortgage segment. Notably, the business lending, corporate finance as well as other lending makes up gross loans and acceptances for the corporate and institutional banking division.

Asset Quality Remains Strong and Provisioning Remains Prudent: NAB’s asset quality remains strong across the portfolio with business lending witnessing an improvement in 90+ DPD plus gross impaired assets to 0.71% in FY18 from 0.70% in FY17. It was mainly driven by the rise of 90+ DPD assets but partially offset by the reduction of impaired assets during the year. Under the current scenario, we presume that asset quality trends remained benign in the short run.

.png)

Asset Quality and Provisioning (Source: Company Reports)

What Affected New Zealand Banking Division in FY 2018: The New Zealand Banking division of NAB witnessed the robust performance in FY 2018 in comparison to FY 2017 because of the higher revenues which were aided by elevated margin levels as well as strong growth in the lending. These favorable factors got partly offset by increased investments. The division’s net interest income witnessed the YoY growth of 9.2% to $1.8 billion in FY 2018. During the same period, its average interest earnings assets rose 5% YoY on the back of favorable momentum in the housing as well as business lending. The division’s customer deposits were well-supported by the term as well as demand deposits.

Healthy Dividend Payout Ratio: From the past few years, National Australia Bank has managed to maintain its healthy dividend payout ratio with 100% franking facility. In FY 2014, the bank’s dividend payout ratio stood at 93.8% and finally, in FY 2018 the payout ratio was 94.1%. However, in FY15, FY16, and FY17, the payout ratios were 79.5%, 80.8%, and 79.4%, respectively. In our view, the bank will maintain its dividend payout ratio in the range of 73%-94% in the upcoming period as the group focuses on building a more sustainable business through exceptional customer services, prudent investment towards customer satisfaction, and improving its core business despite headwinds in the banking sector.

.png)

Healthy Dividend Payout Ratio (Source: Company Reports)

How Does Future of NAB Looks Like: The banking environment in the Australian economy has been witnessing lots of regulatory challenges and macroeconomic pressures which might derail their performance moving forward. The management of National Australia Bank stated that the Royal Commission has highlighted some of the situations where the bank has not been able to treat the customers with respect as well as care. However, the bank has been working to win the confidence and trust which they have lost.

In H2 FY18, National Australia Bank has recognized customer-related remediation which amounted to $360 million and consists of the compensation as well as refunds. Amidst the challenging environment, the management of the bank is favorable about the economic outlook. The management stated that robust economic growth in the Australian region is underpinned by the mining exports, government infrastructure spending as well as favorable momentum in the non-mining business investment. However, the factors like lower investor demand as well as weaker housing prices would be impacting the performance overall banking industry. The business fundamental of National Australia Bank is expected to remain sensitive primarily to the regulatory pressures which could weigh on the lending activities of the bank.

What to Expect from NAB Moving Forward: National Australia Bank encountered significant customer remediation expenses along with the restructuring costs. The bank is expected to work towards winning back the customer confidence. The management of the bank stated that the executive remuneration has been simplified as well as target reward outcomes have been reduced. It added that from FY 2019, 97% of the total staff would be rewarded under the bank’s plan named “Group Variable Reward Plan.” The mortgage brokers would not be eligible for volume bonus payments, and the commissions would be based upon the draw-downs.

National Australia Bank has been working at a rapid pace to fix the issues. It has managed to come up with a new centre which focuses on the customer remediation. The bank has been working with Australian Securities and Investments Commission or ASIC towards helping the customers with respect to the adviser service fees.

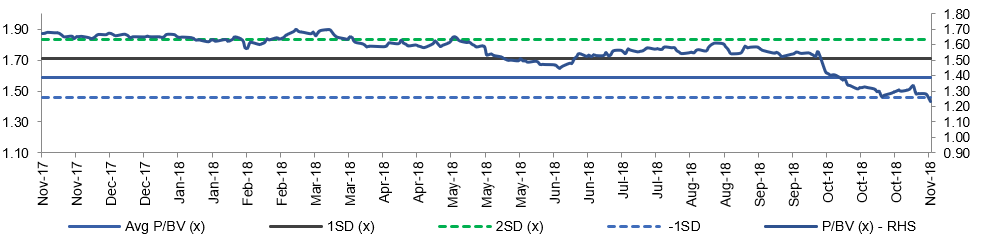

P/BV Band (Source: Company Reports and Thomson Reuters)

Stock Performance and Outlook: In last three months, the stock has been down by around 15.62% and is trading close to its low levels while being in an oversold region. The technical indicators i.e., Relative Strength Index or RSI has been used on the daily chart to track the movements in the stock price of National Australia Bank. We have considered the default values. As per the observation, the 14-day RSI has reached the oversold zone and, thus, a rebound is expected. The stock might create a bullish momentum. Moreover, robust economic growth as well as initiatives to regain the customers’ confidence are expected to support the performance of NAB moving forward. Additionally, if the increased investments pay off, the bank might witness strong growth. Based on decent fundamentals with growing deposits and transactional account along with increasing lending business and maintaining decent dividend payout ratio in the range of 73% to 94% over the past few years, we believe that NAB can sustain high P/BV multiple and reward the investors as the group chases to achieve APRA’s ‘unquestionably strong’ capital benchmark of 10.5% in an orderly manner by 1 January 2020 from 10.2% in FY18. Currently, NAB is trading at PE multiple of 11.89x, which is marginally below peers, signifying undervalued scenario at the current juncture. Hence, we have valued the stock using 1 -year forward P/BV multiple and have arrived at the target price that may see an upside of the mid-single to low double-digit per cent with a higher side ascribing a valuation of 1.48X FY20E P/BV. Based on the foregoing, we give a “Buy” recommendation on the stock at the current market price of $ 23.880.

.png)

NAB Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Please wait processing your request...

Please wait processing your request...