Company Overview -National Australia Bank (NAB) is a financial services organization serving the customers in Australasia. The Company offers banking and financial services ranging from private wealth, investment advisory, to business and institutional banking. The Company’s business segments include Australian Banking; NAB Wealth and NZ Banking. In addition, other segments include UK Banking; NAB UK Commercial Real Estate (NAB UK CRE), and Corporate Functions and Other. Australian Banking offers a range of banking products and services to retail and business customers. NAB Wealth provides superannuation, investments and insurance solutions. NZ Banking comprises the Retail, Business, Agribusiness, Corporate and Insurance franchises in New Zealand. UK Banking operates under the Clydesdale and Yorkshire Bank brands offers banking services for both personal and business customers. NAB UK CRE’s portfolio business comprises approximately £5.6 billion of commercial real estate loan assets.

.png)

NAB Details

Better than estimated cash earnings performance: National Australia Bank Ltd. (ASX: NAB) reported a cash earnings rise by 6.5% yoy to $3.31 billion during the first half of 2016. The group’s revenue rose by 3.3% on a yoy basis on a cash earnings basis during the period. But revenue surged even better by 4.5% on a yoy basis without the gains from the UK Commercial Real Estate loan portfolio sale and SGA asset sales during the period. The rise in revenues were driven by the rising lending balances, better net interest margins (NIM), and solid NAB Wealth net income which offset the declining markets and treasury income. NIM enhanced by 1 basis point, driven by the repricing in home lending and deposits, which offset rising wholesale funding costs and competition from business lending.

The group’s net loss attributable to the owners fell by $5.18 billion to $1.74 billion during the period on a statutory basis, impacted by loss on demerger and Initial Public Offering (IPO) of CYBG PLC (CYBG) of $4.22 billion. This coupled with the charge of $801 million related to provisions for conduct costs pursuant to claims under the Conduct Indemnity Deed with CYBG also impacted the bottom line. Meanwhile, statutory net profit rose by 2.4% to $3.31 billion without discontinued operations.

.png)

NAB business performance (Source: Company Reports)

Decline in Bad and Doubtful Debts: The bank’s overall charge for Bad and Doubtful Debts (B&DDs) fell by 6% or $24 million to reach $375 million on yoy basis. On the other hand, the overall charges surged by 7.4% or $26 million against half year ended on September 2015, impacted by the rising specific provision charges in Australian Banking related to small number of major name exposures, coupled with rising collective provision charges for NZ Banking on the back of the ongoing challenging market conditions facing the dairy industry.

Meanwhile, the bank’s expenses also increased by 4.2%, on the back of the group’s investment in its priority customer segments and rising technology and personnel costs. The bank’s Expenses rose by 2% against the September 2015 half year.

Asset quality highlights: National Australia Bank Common Equity Tier 1 (CET1) ratio fell by 55 basis points to 9.7% as of March 2016, against September 2015 due to CYBG demerger and IPO impact. NAB estimates its CET1 target ratio to remain in the range of 8.75% – 9.25%. The bank intends to issue a new ASX listed via Tier 1 capital security, to boost its capital position. NAB also reported an interim dividend of 99 cents per share fully franked during the first half of 2016 in line with its 2015 interim and final dividends. National Australia Bank also intends to sustain its well-diversified funding profile and raised $17.7 billion of term wholesale funding during March 2016 half year.

The funds weighted average term to maturity raised by the group is 4.7 years and has a stable funding index of 89% as of March 2016. National Australia Bank quarterly average liquidity coverage ratio reached 125% as of March 2016. The ratio of the bank’s 90+ days earlier due and gross impaired assets to gross loans and acceptances reached 0.78% as of March 2016 against the 0.63% in September 2015 and 0.77% in March 2015. Meanwhile, the ratio of collective provision to credit risk weighted assets was 0.98% as of March 2016 against 0.99% as of September 2015. The ratio of specific provisions to impaired assets reached 36.4% against the 30.3% as of September 2015.

.png)

Asset quality (Source: Company Reports)

Improving customer experience: National Australia Bank’s efforts to improve its Net Promoter Score (NPS) have been showing positive results. The group also invested in technology and digital offerings to enhance its customer experience and also making process improvements to make things smooth for its customers.

Accordingly, the bank launched NAB Pay, which is the pilot of its digital hub for small banking customers called Business in One, as well as launched NAB Dash that streamlines the consumer-merchant experience. Moreover, the bank’s Personal Banking Origination Platform has been rolled out across South Australia, the Northern Territory and Western Australia. This technology allows the bank’s clients to track applications online as well as send SMS or email updates for major events. The group’s 2016 national rollout is on track.

Solid personal banking business: The group’s Personal Banking customer revenue rose by 10.2% yoy to $2.439 billion for the half year ended on 2016, and increased by 4% as compared to the second half of 2015. Business banking revenue rose by 2% as compared to the same period of last year, as the group’s enhanced tools led to better loan growth in its major segments and consequently improved margins during the March 2016 half year. The bank also delivered a competitive SME NPS score for the six months ended on March 2016 as compared to its major bank peers.

National Australia Bank continues to focus on its core Australian and New Zealand businesses which generated a Banking cash earnings rise of 5% yoy to $2,694 million. The segment’s revenues increased by 4% on the back of better lending volumes and improved NIM, while expenses rose by 6% driven by performance based incentive normalization, Enterprise Bargaining Agreement salary increases and rise in project and technology costs. However, B&DD charges fell by 7% yoy to $341 million, due to decrease in collective provision charges.

.png)

Personal banking business performance (Source: Company Reports)

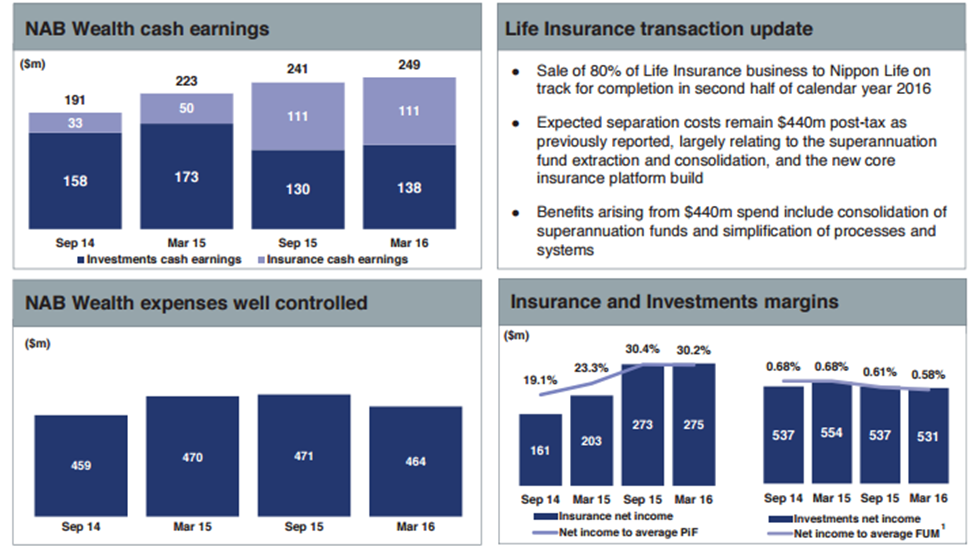

Enhancing wealth business performance: The bank continued to deliver a solid Wealth cash earnings for the first half of 2016, which rose by 12% to $249 million backed by the solid Insurance results, and has been growing since 2013. Net income enhanced by 4% on the back of better Insurance premiums and pricings along with enhanced claims expense and stable lapse performance. However, the expenses were controlled by 1%, on the back of decrease in technology and project costs which partly offset rising number of financial planners. Meanwhile, the group’s sale of 80% of its Life Insurance business to Nippon Life is on track and estimates to finalize it by the second half of the year.

Moreover, the bank also intends to leverage the potential opportunity of its Investments and Superannuation business by enhancing the customer experience as well as by building a closer relationship with its banking operations.

Improving wealth business performance (Source: Company Reports)

Outstanding dividend yield: The shares of National Australia Bank Ltd. (ASX: NAB) have been consolidating in the last six months and slightly rose by 2%. NAB rallied over 7.8% in the last three months (as of May 06, 2016) while delivered an outstanding performance in the last four weeks by increasing 10.6% as the group delivered a better than expected first half of 2016 performance. NAB’s efforts to enhance its personal banking and wealth business would continue to support the stock in the coming months.

Moreover, the bank’s Bad and Doubtful Debts fell during the period even though the New Zealand division’s Bad and Doubtful Debts increased. But, the group is also planning to make a provisioning for future dairy impairments for its New Zealand division despite the recovering New Zealand economy. Moreover, NAB is also generating a good dividend yield. Based on the foregoing, we give a “BUY” recommendation on the stock at the current price of $28.45

.PNG)

NAB Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2016 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Please wait processing your request...

Please wait processing your request...