Company Overview - National Australia Bank (NAB) is a financial services organization serving the customers in Australasia. The Company offers banking and financial services ranging from private wealth, investment advisory, to business and institutional banking. The Company’s business segments include Australian Banking; NAB Wealth and NZ Banking. In addition, other segments include UK Banking; NAB UK Commercial Real Estate (NAB UK CRE), and Corporate Functions and Other. Australian Banking offers a range of banking products and services to retail and business customers. NAB Wealth provides superannuation, investments and insurance solutions. NZ Banking comprises the Retail, Business, Agribusiness, Corporate and Insurance franchises in New Zealand. UK Banking operates under the Clydesdale and Yorkshire Bank brands offers banking services for both personal and business customers. NAB UK CRE’s portfolio business comprises approximately £5.6 billion of commercial real estate loan assets.

.png)

NAB Dividend Details

Built strong Wealth Business: National Australia Bank Ltd. (ASX: NAB) built a strong wealth business from the last three years by offering superannuation, investment and insurance solutions to retail, corporate and institutional clients. The group’s wealth business is among the major financial advisers in Australia which operates under brands like JBWere, JANA, MLC, and Plum. Therefore, National Australia Bank is investing further $300 million into its superannuation platforms, advice and asset management business during the coming four years to further improve its customer solutions. Meanwhile, the solid Wealth business of NAB contributed to the group’s long term partnership with Nippon Life, a leading life insurers. As a result, the bank made an agreement to sell 80% of its Wealth’s life insurance business to Nippon Life Insurance in October 2015.

Improving penetration of banking business: National Australia Bank is gaining market share in its core banking business as the group’s investments over the past few years have paid off. National Australia Bank has been focusing on SME segments, a major trend in banking business and also further added 330 bankers on the frontline. The bank also expanded its capabilities in its import segments like SMEs, micro-business, debt free and mortgage customers. Moreover, NAB’s Personal Banking business delivered a strong performance during fiscal year of 2015 and posted a revenue growth of 7.3% on a year on year basis. The bank’s Personal Banking products are accessed via several channels, like NAB, NAB Broker, nabtrade and UBank. In addition, the Australian Banking also comprises Fixed Income, Currencies and Commodities (FICC), Capital Financing, Asset Servicing and Treasury. Meanwhile, NAB also built a decent international reach with presence in several geographies like Hong Kong, Beijing, Shanghai, Singapore, Tokyo, Osaka, Mumbai, London and New York.

.png)

Fiscal year of 2015 business performance (Source: Company Reports)

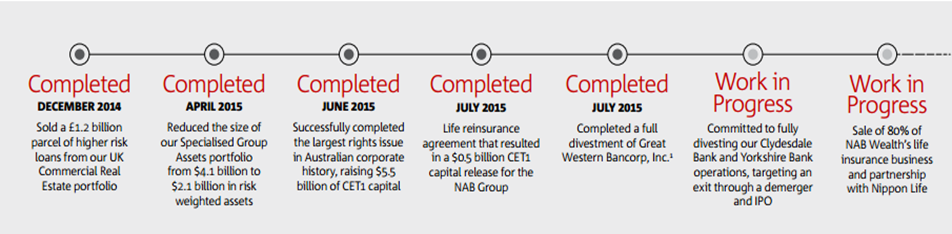

Boosting Balance Sheet: The bank is continually strengthening its capital position and accordingly raised over $5.5 billion of capital via rights issue to comply with the APRA regulations as well as withstand volatility in the markets. Moreover, NAB divested its US subsidiary, Great Western Bancorp as well as decreased stake in its UK commercial real estate exposure by selling higher risk loans for £1.2 billion, on the back of slowdown in UK coupled with solid regulatory imposts after the GFC. Meanwhile, the demerger as well as the proposed Initial Public Offering (IPO) of its Clydesdale and Yorkshire banks in the UK, is estimated to be finished by this year further boosting NAB’s capital position. The bank even decreased the size of its Specialized Group Assets portfolio from $4.1 billion to $2.1 billion in risk weighted assets. National Australia Bank is offloading 80% of its Wealth’s life insurance business for $2.4 billion to Nippon Life Insurance Company and released $0.5 billion of CET1 capital for this agreement. The bank’s Common Equity Tier 1 Capital ratio improved to 10.24% as of September 2015, as compared to 8.87% in March 2015. Meanwhile, National Australia Bank delivered strong statutory return on equity rise of 100 basis points to 13.1% as compared to prior corresponding period. Cash return on equity surged 40 basis points to 12.0% during the fiscal year of 2015 as compared to the prior corresponding period.

Timeline of the last one year events (Source: Company Reports)

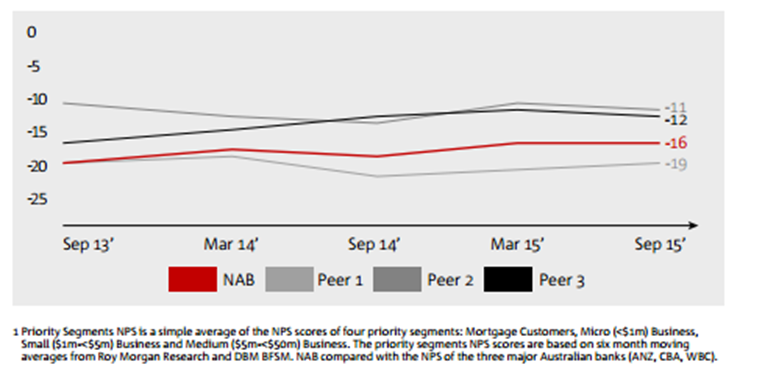

Focusing on Customer Service: The group has been focusing on enhancing customer experience for its financial products leading to a rise of over 500,000 customer’s sales and service experiences per annum. For instance, NAB Village at Docklands in Melbourne is an innovative space which offers the group’s customers and community partners to connect with clients, as well as work between meetings and learn from each other. As a result, around 25% of the members have already began a banking relationship with the bank to access NAB Village. Meanwhile, the bank’s Employee engagement score rose by 10 percentage point during the 2015 fiscal year as compared to 2014. During 2015, the bank enhanced the turn-around times for clients by enabling slight modifications to their mortgages as well as decreased the time for approving simple business loans. NAB also decreased the paper work required from clients who are applying for simple business loans, equipment finance and commercial cards. On the other side, NAB is also investing on technology to cater the rapidly changing digital trends and clients preferences. Some of the group’s initiatives include Personal Banking Origination Platform (PBOP) 3 pilot, NAB Connect4 upgrades, NAB StarXchange5 pilot and NAB Prosper6. Moreover, the bank reported a development of its in house innovation center named NAB LABS as well as building a $50 million fund for the next three years, to support the investments in emerging payments and technology companies. Meanwhile, National Australia Bank is adopting the Net Promoter System (NPS) for the first year, to understand its strength in its customers’ advocacy and consequently enable the group to improve its customer solutions. Priority segments net promoter score reached -16 in fiscal year of 2015, as compared to -18 in fiscal year of 2014.

Priority Segments Net Promoter System against the bank’s peers (Source: Company Reports)

Stock Performance: The shares of National Australia Bank have been under pressure from the last six months and fell over 16.83% (as of January 08, 2016) on the back of tight regulations, intensifying competition as well as economic slowdown. Moreover, National Australia Bank has been undergoing several changes in the Board over the last one year with the CEO of NAB, Michael Chaney being replaced by Ken Henry. Ken joined the Board in the month of November during 2011 after serving as Secretary of the Commonwealth Treasury for over a decade as well as a member of the Board of the Reserve Bank of Australia. Ken showcased strong understanding of financial and regulatory environments as well as on issues and challenges faced by the financial institutions in the current rapidly changing environment. On the other hand, National Australia Bank delivered a decent net profit attributable to the shareholders increase of 19.7% year on year in fiscal year of 2015. The bank has been raising capital to boost its balance sheet and even divesting or offloading its non-core assets. This move by NAB would help the bank to focus more on its core segments across its Personal and Business Banking businesses, in which the bank has a competitive edge over its peers. The bank has built specialization capabilities in several diverse fields like Agribusiness and Health. National Australia Bank is also building its online capabilities to enhance its processes and policies across the business and intends to further focus on technology simplification, process excellence as well as the bank’s digital footprint across the world. Meanwhile, management reported that the Australian economy would continue to be mixed during this year, wherein the mining investments would continue to decline while other growing sectors, especially the service and tourism sectors performance might improve. Good momentum is also expected from the retail banking marketing and pricing growth strategy with regards to new customers, loan growth and customer deposits amidst intense competition. Given the entire scenario, the management has estimated a moderate GDP growth of 2.3%. However, the bank estimates a better GDP during next year at 3.2%. We believe that investors can leverage the current low levels of National Australia Bank to enter the stock given the improving long term prospects in the overall Australian economy and thus the bank’s projections. Moreover, the bank is trading at cheap valuation with a P/E of about 11x. In addition, NAB has an outstanding dividend yield of 7.1%. Based on the foregoing, we give a “BUY” recommendation on the stock at the current price of $27.42

NAB Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2016 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Please wait processing your request...

Please wait processing your request...