Company Overview - National Australia Bank (NAB) is a financial services organization serving the customers in Australasia. The Company offers banking and financial services ranging from private wealth, investment advisory, to business and institutional banking. The Company’s business segments include Australian Banking; NAB Wealth and NZ Banking. In addition, other segments include UK Banking; NAB UK Commercial Real Estate (NAB UK CRE), and Corporate Functions and Other. Australian Banking offers a range of banking products and services to retail and business customers. NAB Wealth provides superannuation, investments and insurance solutions. NZ Banking comprises the Retail, Business, Agribusiness, Corporate and Insurance franchises in New Zealand. UK Banking operates under the Clydesdale and Yorkshire Bank brands offers banking services for both personal and business customers. NAB UK CRE’s portfolio business comprises approximately £5.6 billion of commercial real estate loan assets.

NAB Core Business Contribution (Source - Company Reports)

Improved earnings, despite tough market conditions: National Australia Bank Ltd. (ASX: NAB) reported a revenue increase of 4% on a year over year basis during the third quarter of 2015. Revenues increased over 2% as compared to the corresponding period of last year, without the gains from the UK Commercial Real Estate loan portfolio sale, SGA asset sales and legal settlement gain during the quarter. But, accordingly the expenses also rose by over 4% on a year over year basis, due to investing activities across NAB’s customer segments, small legacy equity investment impairment charges as well as foreign exchange rates impact. The cash earnings surged around 9% on a year over year basis to $1.75 billion during the quarter, and improved 6% as compared to the quarterly average of the March 2015 Half Year performance. Meanwhile, the group reported a $1.85 billion of net profit attributable to the owners of the group on a statutory basis (includes treasury shares, and fair value and hedge ineffectiveness). National Australia Bank’s charge for Bad and Doubtful Debts also slumped by 15% on a year over year basis to $193 million mainly impacted by the lower charges in Australian Banking.

Key Shareholder Metrics (Source - Company Reports)

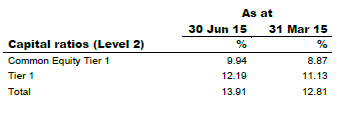

Building a flexible balance sheet, to offset the rising mortgage risk weights: The bank’s Common Equity Tier 1 (CET1) ratio improved by 107 basis points to 9.94% as at June 2015, as compared to March 2015 driven by the rights issue proceeds. The bank reiterated its CET1 target ratio in the range of 8.75% to 9.25% as per the current regulatory requirements. Meanwhile, National Australia Bank’s quarterly average liquidity coverage ratio reached 118% as of June 2015. The group finished $5.5 billion rights issue, to reposition its balance sheet and before the APRA’s declaration of rise in mortgage risk weights since July 2016.

Capital ratios performance (Source: company reports)

Enhancing its core Australian and New Zealand business: The bank improved its asset quality in Australian and New Zealand business and took initiatives to deal with its legacy issues. The bank invested on its home lending, SME and Specialized Business, to enhance its customer experience as well as improved its business banking loan portfolio and wealth business. The bank’s Wealth life reinsurance transaction delivered over $500 million of CET1 capital (another 13 basis points improvement), as well as decreased the bank’s exposure to retail life insurance. Meanwhile, National Australia bank also finished divesting its remaining balance holdings at Great Western Bank from which over $1.3 billion funds were generated, boosting the group’s CET1 capital by over 34 basis points. However, the bank sold 16.49 million shares of over 28.5% of GWB common stock. National Australia took this divestment initiative in an effort to improve its focus on its core Australian and New Zealand business. But, the group witnessed a loss of $396 million related to the GWB book value. The final offering is forecasted to result to a loss of $67 million, which would be reflected during the 2015 September results. The group will be giving more clarity on its demerger and IPO of Clydesdale Bank during the 2015 fiscal results.

Capital ratios performance (Source: company reports)

Enhancing its core Australian and New Zealand business: The bank improved its asset quality in Australian and New Zealand business and took initiatives to deal with its legacy issues. The bank invested on its home lending, SME and Specialized Business, to enhance its customer experience as well as improved its business banking loan portfolio and wealth business. The bank’s Wealth life reinsurance transaction delivered over $500 million of CET1 capital (another 13 basis points improvement), as well as decreased the bank’s exposure to retail life insurance. Meanwhile, National Australia bank also finished divesting its remaining balance holdings at Great Western Bank from which over $1.3 billion funds were generated, boosting the group’s CET1 capital by over 34 basis points. However, the bank sold 16.49 million shares of over 28.5% of GWB common stock. National Australia took this divestment initiative in an effort to improve its focus on its core Australian and New Zealand business. But, the group witnessed a loss of $396 million related to the GWB book value. The final offering is forecasted to result to a loss of $67 million, which would be reflected during the 2015 September results. The group will be giving more clarity on its demerger and IPO of Clydesdale Bank during the 2015 fiscal results.

Australian Banking Benefits (Source - Company Reports)

Segment Performance: The firm’sAustralian Banking cash earnings improved during the June quarter driven by reducing B&DD charges. The region’s revenues increased on the back of better volumes of housing and business lending, while the rising revenues were offset by the decrease in markets and treasury income as well as poor business lending margins. Meanwhile, the New Zealand banking’s cash earnings (local currency) surged during the quarter, boosted by better revenues on the back of enhanced margins and stable volumes. However, the higher expenses have partly offset the group’s overall earnings. National Australia Bank’s Wealth cash earnings performance rose driven by the increasing combined premium coupled with decrease in retail claims. On the other hand, the UK banking cash earnings continued to be under pressure during the quarter impacted by the timing of the Financial Services Compensation Scheme (FSCS) charge as well as the non-recurrence of a one-off pension scheme gain witnessed during the March 2015 Half Year results.

Asset quality Highlights: National Australia Bank’s asset quality metrics have improved during the June quarter. The ratio of the bank’s 90+ days earlier due and gross impaired assets to gross loans and acceptances decreased to 0.78% as at June 30 2015, as compared to 0.85% as at March 31 2015. The group’s ratio of specific provisions to impaired assets also declined to 35.2% as at June 2015 against the 35.5% at March 2015.

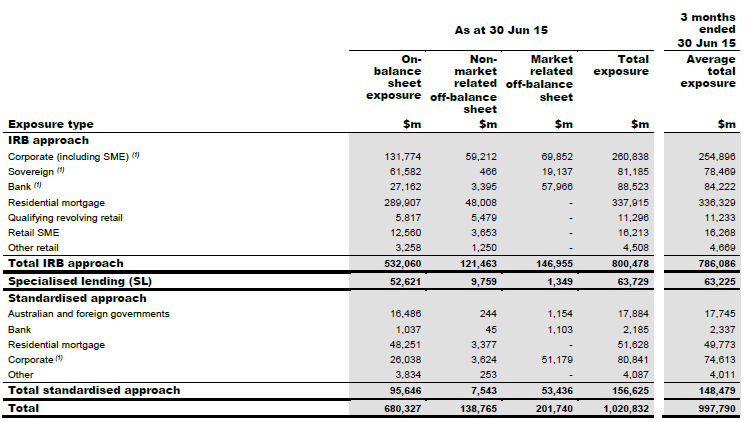

National Australia Bank’s credit risk exposure (Source: company reports)

UK Operations pressure: National Australia Bank reported that UK Prudential Regulation Authority (PRA) said that the bank needs to offer £1.7 billion capital support to Clydesdale Bank related to the possible future legacy conduct costs to realize the proposed demerger and IPO of that business, during its March 2015 half year results. The group might also incur costs related to the conduct related matters as a contingent liability. Meanwhile, the Clydesdale Bank has been operating its remediation program. The program includes the progress on its earlier business review as well as any consequent need to undertake further proactive customer contact. Accordingly, the group forecasts an additional provision with regards to the payment protection insurance which might be recognized during the finalization of the bank’s accounts during the full year 2015 results. The provision is estimated to be in the range of £290 million to £420 million, impacted by the rising costs to run the remediation program as well the past business review. The bank might also incur an extra provision in the range of £60 million and £80 million related to the interest rate hedging products as per the current compensation calculations for completed reviews(and assuming these would be stable) during the full year 2015 results.

NAB Daily Chart (Source - Thomson Reuters)

Stock Performance: The shares of National Australia Bank could not gain support even though the bank reported a better than estimated results, as the bank now expects an extra £500 million impact from its UK operations. Moreover, with the management revealing an increase in provision of £290 million and £420 million, related to Clydesdale Bank during the 2015 full year results, investors’ concerns on the bank’s earnings have raised. On the other hand, investors are hunting for high value dividend stocks given the recent sell off among the Australia stocks, and we believe that NAB stock can be an attractive investment. The stock declined over 16.67% in the last six months, as compared to the broader index fall of 11.2%. However, investors need to note that the bank has already diverted over a £1.7 billion funds under its conduct mitigation package. Moreover, the group’s June quarter performance have been pleasing despite tough market conditions, while its agriculture and resources loan defaults provision, which the bank incurred during March 2015 fiscal half were not reflected during the June quarter. Meanwhile, the stock’s correction of around 7.6% during the last four weeks, have placed it at an opportunistic entry point for investors. National Australia bank also offers attractive valuation as compared to its banking peers, and trading at a cheaper P/E of 13.36x. The group has a strong dividend yield of 6.2% while its return on equity is 10.9%. Based on the foregoing, we give a “BUY” recommendation to National Australia Bank at the current stock price of $31.17

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Please wait processing your request...

Please wait processing your request...