Company Overview: Mount Gibson Iron Limited is a producer of iron ore products. The Company's principal activities include mining and shipment of hematite iron ore at Koolan Island in the Kimberley region of Western Australia; mining of hematite iron ore deposits at the Extension Hill mine site in the Mid-West region of Western Australia and haulage of the ore through road and rail for sale from the Geraldton Port, and exploration and development of hematite iron ore deposits at Koolan Island and in the Mid-West region of Western Australia. The Company operates through two segments: Extension Hill and Koolan Island. The Extension Hill segment includes the mining, crushing, transportation and sale of iron ore. The Extension Hill mine is located in the Mt Gibson Ranges. The Koolan Island segment includes the mining, crushing and sale of iron ore. The Company's Koolan Island hematite mining operation is located approximately 140 kilometers north of Derby in Yampi Sound, Western Australia..png)

MGX Details

Decent Top-line and Bottom-line Growth in FY16-19: Mount Gibson Iron Limited (ASX: MGX) is primarily involved in mining and processing of hematite iron ore at the Extension Hill mine site in the Mid-West region of Western Australia, as well as haulage of the ore via road and rail for export from the Geraldton Port. The company’s overall objective is to maintain and grow long-term profitability through the discovery, acquisition, operation and development of mineral resources.

Looking at the past performance over FY16 to FY19, total revenue and net income of the company have grown with a CAGR (compounded annual growth rate) of 5.74% and 15.62%, respectively. Group’s total revenue improved from $244.9 Mn in FY16 to $289.5 Mn in FY19, and net income improved from $86.3 Mn in FY16 to $133.4 Mn in FY19.

The company is determined to achieve its key business objectives for the financial year 2020, which include continuing the ramp-up of ore production at Koolan Island to maximise cashflow and capitalise on favourable market conditions, and progress the airstrip development to enable direct flights in the second half of 2020. It plans to complete the contracted program of low-grade sales from Extension Hill and seeks further extension opportunities. It focuses on cost optimization across its existing business and maintains the yield on the group’s cash and investment reserves. It is expected to continue to evaluate acquisition opportunities in the resources sector..png)

Historical Performance of MGX (Source: Company Reports)

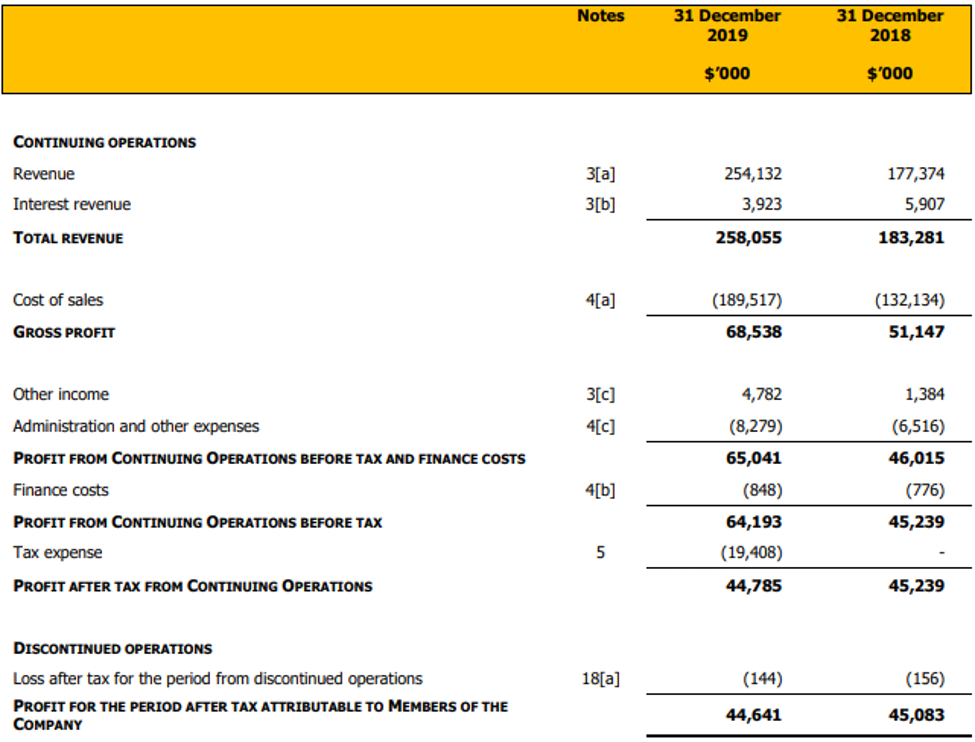

H1FY20 Key Highlights for the period ended December 31, 2019: The group reported a net profit after tax of $44.641 million, as compared to $45.083 million in the previous corresponding period. On a pre-tax basis, the group realized a net profit before tax from continuing operations of $64.193 million as compared to $45.239 million in the previous corresponding period. This result can be attributed to the ramp-up of ore production and sales volumes from the high-grade Koolan Island mine in the Kimberley region, strong iron ore pricing, receipt of the first biannual partial-refund of historical rail access charges relating to third party usage of the Perenjori to Geraldton railway line and opportunistic sales of remnant low-grade material stockpiled at the closed Extension Hill mine in the Mid-West.

Group ore sales for the period came in at 2.8 million wet metric tonnes with sales revenue amounting to $254.132 million. Revenue comprised $230.146 million Free On Board (FOB) revenues and $23.986 million in shipping freight services.

During the half-year period, the Group achieved an average realized price for Koolan Island high-grade iron ore fines product at US$83/dmt FOB after grade and provisional pricing adjustments and penalties for impurities, whereas remnant low-grade material sold from the Mid-West realized an average price of US$35/dmt FOB for lump and US$28/dmt FOB for fines. The weighted average realized price received for all products sold (after including provisional pricing adjustments and net foreign exchange hedging gains) stood at $83/wmt FOB in H1FY20, as compared to $73/wmt FOB in the FY19 during which standard direct-shipping-grade ore (DSO) from the now completed Iron Hill Deposit in the Mid-West accounted for the majority of ore sales.

H1FY20 Income Statement (Source: Company Reports)

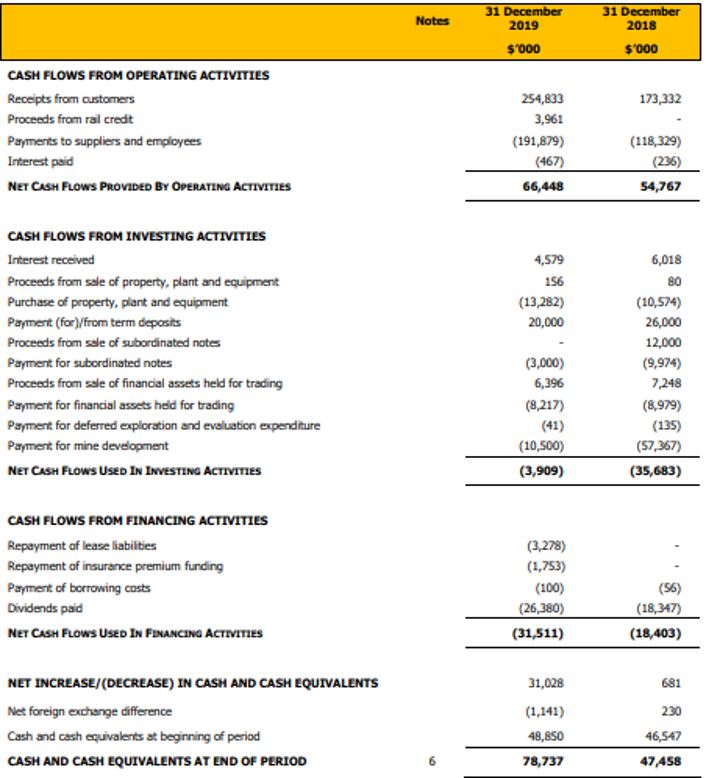

Cash Reserves at the end H1FY20 Stood at $397.86 Mn: Cash reserves (inclusive of tradeable investments and term deposits) as on December 31, 2019, was reported at $397.856 million, an increase of $13.325 million over the half-year. This can be attributed to a positive underlying operating cashflow (inclusive of working capital movements, head office administration and capital expenditure) of $35.126 million along with payment of the $26.380 million cash component of the fully franked final dividend to shareholders for the financial year 2019 and interest income of $4.579 million.

Group’s current assets and current liabilities at the end of the period were reported at $454.000 million and $74.444 million, respectively. The current liabilities include $6.728 million current lease liabilities as a result of adopting AASB 16 Leases.

H1FY20 Cash Flow Statement (Source: Company Reports)

Important Updates:

(a) The Group has an entitlement to receive a partial refund (capped at a total of ~$35 million (subject to indexation)) of historical rail access charges from the Mid-West rail leaseholder, Arc Infrastructure, based upon the future usage by certain third parties of specific segments of the Perenjori to Geraldton railway line. This entitlement has a time limit expiring in 2031, with receipt of this potential future refund is not certain and is fully dependent on the volumes railed by third parties on the specified rail segments. MGX received the first payment of $3,961,000 (for first six-month period), in September 2019. The entitlement payment is due for every six months and is currently accruing as a receivable at a rate of ~$2.0 million per quarter.

(b) In October 2019, MGX informed the market about the appointment of Mr. Mark Mitchell as Chief Operating Officer (COO) of the company, following the retirement of Mr. Scott de Kruijff, long-serving senior operational executive. In December 2019, the company disclosed the appointment of Mr. Ding Rucai as a Non-Executive Director of MGX.

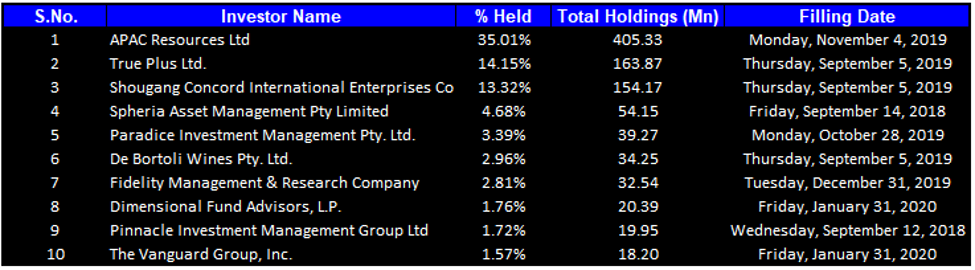

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together form around 81.38% of the total shareholding. APAC Resources Ltd and True Plus Ltd. hold maximum interests in the company at 35.01% and 14.15%, respectively.

Top 10 Shareholders (Source: Thomson Reuters)

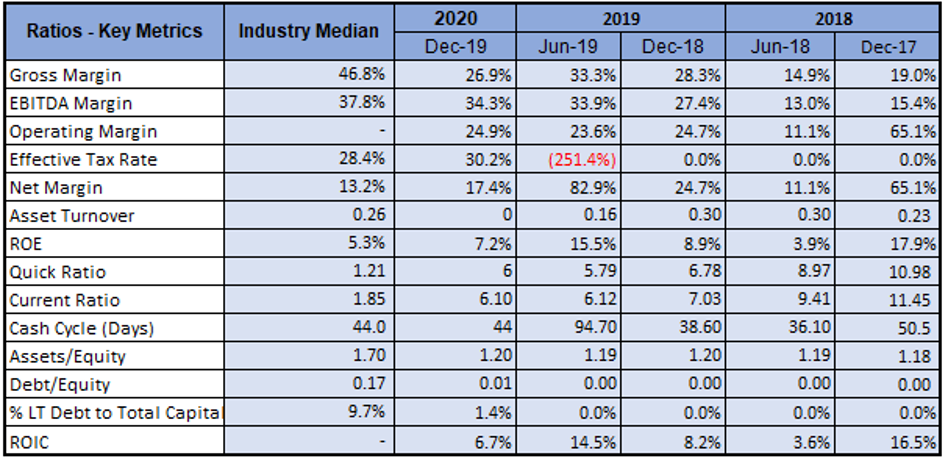

A Quick Look at Key Metrics: Its EBITDA margin for H1FY20 stood at 34.3%, better than the result in H1FY19 at 27.4%. Its net margin for H1FY20 stood at 17.4%, better than the industry median of 13.2%, implying decent fundamentals for the company. ROE for H1FY20 stood at 7.2%, better than the industry median of 5.3%, which implies that the company generated a better return for its shareholders.

Its current ratio for H1FY20 stood at 6.10x, better than the industry median of 1.85x, which implies that the company is in a good position to address its short-term obligations. Its debt to equity multiple for H1FY20 stood at 0.01x, lower than the industry median of 0.17x.

Key Metrics (Source: Thomson Reuters)

Key Risks: The company is susceptible to certain risks such as foreign currency risk, interest rate risk, credit risk, commodity price risk and liquidity risk.

Koolan Island Outlook: In January 2020, operations were interrupted by extreme cyclone-related weather, however, with no further major weather impacts, ore sales volume guidance for the current financial year remains unchanged. The company is progressing over the new all-weather airstrip toward its target of commencing direct jet flights to and from Perth.

Extension Hill Outlook: The company confirmed an extension of sales from low-grade stockpiles at Extension Hill until the end of April 2020, due to strong prevailing prices and demand. Because of site closure and rehabilitation activities, the Mid-West closure provision has reduced to $9,973,000 as on December 31, 2019, as compared to $11,636,000 in the previous corresponding period.

What to expect: As per the release, following the extension of the low-grade sales program from the Mid-Wes, the company has anticipated total iron ore sales for FY20 at 4.8–5.3 Mwmt at an average group cash cost of $70-75/wmt FOB. The sales guidance for Koolan Island remains unchanged at 2.7–3.0 Mwmt of high-grade DSO, with site cash costs of $77-82/wmt FOB reflecting the impact of wet season rains and all waste stripping activity which is highest in the first two years of the mine life. Moreover, sales of 2.1-2.3 Mwmt of low-grade material at a cash cost of $40-45/wmt FOB can be expected from the Mid-West.

Note: Group cash costs include all operating, sustaining capital, royalties and corporate costs, and are reported FOB. Site cash costs include royalties, sustaining capital expenditure and corporate cost allocations, and are reported FOB.

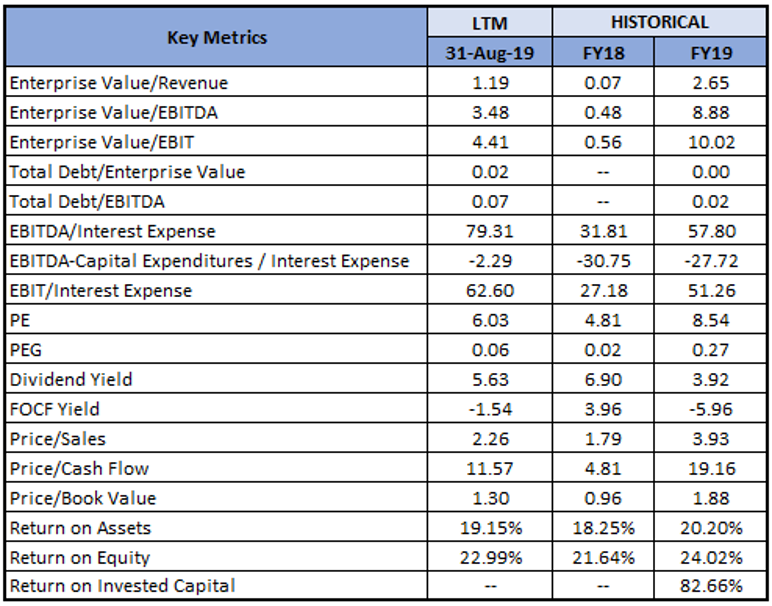

Key Valuation Metrics (Source: Thomson Reuters)

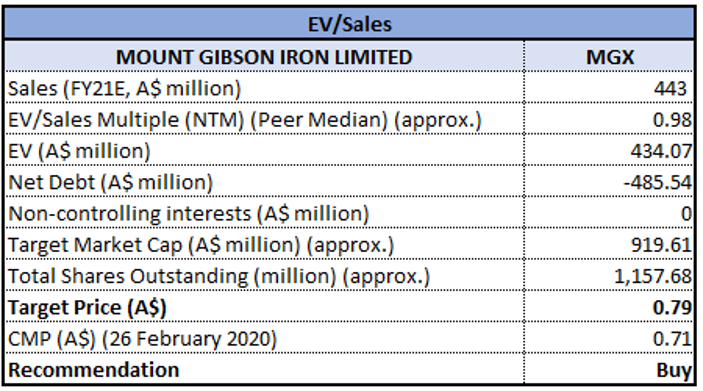

EV/Sales Based Relative Valuation

EV/Sales Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: MGX’s stock posted positive one-year return of 2.10%, while in the span of last 3-months, it plunged by 10.98%. Currently, the stock is trading close to its 52-week low of $0.640, proffering an opportunity for accumulation. The group has enough funds, as well as access to further equity and debt sources to operate and sell iron ore from its operations and to advance its growth objectives. It aims to grow its cash reserves while continuing to pursue an appropriate balance between the retention and utilisation of cash reserves for value-accretive investments. Considering the company’s business model, H1FY20 performance, profitability margins, important updates, outlook, FY20 guidance and current trading levels, we have valued the stock using EV/Sales Based relative valuation method and arrived at a target price of lower double-digit upside (in % terms). Hence, we give a “Buy” recommendation on the stock at the current market price of $0.71, down 2.74% on February 26, 2020.

MGX Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...