Company Overview: Mount Gibson Iron Limited is a producer of iron ore products. The Company's principal activities include mining and shipment of hematite iron ore at Koolan Island in the Kimberley region of Western Australia; mining of hematite iron ore deposits at the Extension Hill mine site in the Mid-West region of Western Australia and haulage of the ore through road and rail for sale from the Geraldton Port, and exploration and development of hematite iron ore deposits at Koolan Island and in the Mid-West region of Western Australia. The Company operates through two segments: Extension Hill and Koolan Island. The Extension Hill segment includes the mining, crushing, transportation and sale of iron ore. The Extension Hill mine is located in the Mt Gibson Ranges. The Koolan Island segment includes the mining, crushing and sale of iron ore. The Company's Koolan Island hematite mining operation is located approximately 140 kilometers north of Derby in Yampi Sound, Western Australia.

MGX Details

FY19 NPAT Improved by ~34.6% on Previous Year: Mount Gibson Iron Limited (ASX: MGX) is involved in mining of hematite iron ore in the Iron Hill deposit at the Extension Hill site in the Mid-West region of Western Australia, and haulage of the ore via road and rail for export from the Geraldton Port; reconstruction of the Koolan Island main pit seawall, in the Kimberley region of Western Australia, with ore sales targeted to resume in early 2019; treasury management; and the pursuit of mineral resources acquisitions and investments. Looking at the historical performance, company’s top-line improved from $194.8 Mn in FY17 to $289.5 Mn in FY19, and its bottom-line improved from $26.3 Mn in FY17 to $133.4 Mn in FY19. Earnings per share also witnessed a decent improvement from 2.41 cents in FY17 to 11.98 cents in FY19.

FY19 was proved to be a decent year in terms of operational transition as the Company’s Mid-West operations wound down, and Koolan Island became the principal longer term source of production and revenue, following the successful restart of ore sales from Main Pit in late April 2019. The performance of the company was assisted by the spiking iron ore prices as compared to the last year.

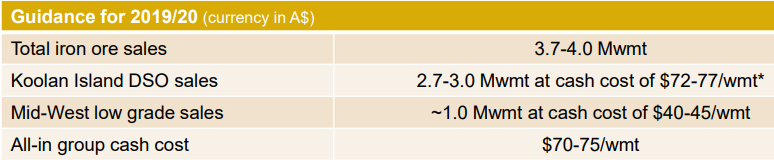

The company aims to grow long-term profitability with the activities related to discovery, development, operation and acquisition of mineral resources. Going forward, the company expects total iron sales to be in the range of 3.7-4.0 Mwmt, where Koolan Island direct shipping ore (DSO) sales is expected to be between 2.7-3.0 Mwmt at cash cost of $72-77/wmt, Mid-West low grade sales is expected to be in ~1.0 Mwmt at cash cost of $40-45/wmt, and All-in group cash cost to be in the range of $70-75/wmt, for FY20.

.png)

FY19 Operating Result (Source: Company Reports)

FY19 Key Highlights (for the period ended on June 30, 2019): Total iron ore sales for the period was reported at 3.2 Million wet metric tonnes (Mwmt), comprising 2.93 Mwmt of direct-shipping ore (DSO) and 0.24 Mwmt of stockpiled low-grade material, as compared to 3.6 Mwmt in FY18. Profit before tax (PAT) from all operations was reported at $70.5 Mn, as compared to $34.8 Mn of PAT before insurance settlement proceeds. Net profit after tax for the period was reported at $133.4 Mn after recognition of deferred tax assets totaling $62.9 Mn, as compared to $99.1 Mn in the previous year. The reported profit before tax (including discontinued operations at Tallering Peak) for the period was reported at $70.5 Mn, which was well in excess of the result of $34.8 Mn in the previous year (excluding the Koolan Island business interruption insurance settlement). This result can be attributed to a 41% increase in average realized prices and the commencement of high-grade sales from Koolan Island in late April 2019.

Group’s average cost of sales increased from $44/wmt FOB (Free on Board) in FY18 to $50/wmt FOB in FY19. This was due to an increase in royalties of approximately $2/wmt arising from higher realized prices, transitional impacts of reduced production and wind-down costs in the Mid-West operation prior to the commencement of low grade sales program later in the year, and operating costs associated with the commencement of high grade sales at Koolan Island. Site cash costs for the Mid-West operations, including low grade sales, averaged $39/wmt FOB for the year, in-line with the guidance. Site cash costs for Koolan Island averaged $77/wmt (excluding royalties) from the commencement of commercial operations at the end of May 2019.

.png)

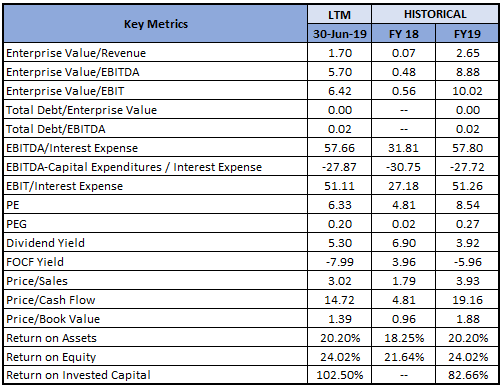

FY19 Key Financial Metrics (Source: Company Reports)

FY19 Operating Cashflow Improved by 70.20% on Previous Year: Cash, term deposits and liquid investments at the end of the period were reported at $384.5 Mn, a decline of $73 Mn from the previous year. This was mainly due to operating cashflow (net of corporate costs) of $59.4 Mn, interest received of $11.6 Mn, Koolan Island mine development expenditure of $109.9 Mn, purchase of property, plant and equipment of $18.5 Mn, and payment of $18.3 Mn cash component for FY18 fully franked dividend to shareholders.

Operating cashflow for the period improved from $34.9 Mn in FY18 (before insurance settlement) to $59.4 Mn in FY19. As per the company’s balance sheet, current assets totaled $447.7 Mn and current liabilities totaled $73.1 Mn. No bank borrowings for liabilities related to trade payables, employee entitlements, derivatives and provisions for rehabilitation and other items, were reported for the period. The Board of Directors declared a fully franked final dividend of 4 cents per share for FY19, totalling $45.2 Mn. It was paid on 26 September 2019 with a record date of September 04, 2019.

.png)

FY19 Working Capital Movement (Source: Company Reports)

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together form around 82.83% of the total shareholding. APAC Resources Ltd and True Plus Ltd. hold maximum interest in the company at 34.73% and 14.15%, respectively. Recently, Allied Properties Investments company limited and its related bodies, increased its stake in the company from 33.23% to 34.73%, effective from September 26, 2019. In another update, company’s directors Lee Seng Hui and Simon Bird, acquired 22,619,817 ordinary sharesand2,680 ordinary shares, taking the final holdings to 402,017,287 ordinary shares and 47,919 ordinary shares, respectively, effective from September 26, 2019.

.png)

Top 10 Shareholders (Source: Thomson Reuters)

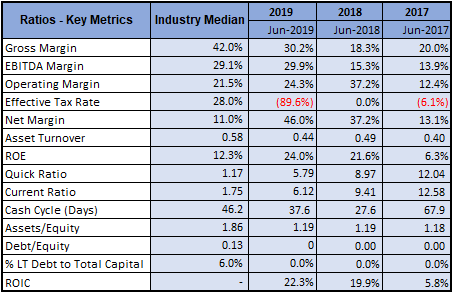

A Quick Look at Key Metrics: Its EBITDA margin and net margin for FY19 stood at 29.9% and 46.0%, better than the industry median of 29.1% and 11.0%, respectively, implying decent fundamentals for the company. Its ROE for FY19 stood at 24.0%, better than the industry median of 12.3%, which implies that the company generated a better return for its shareholders than its peer group. Its quick ratio for FY19 stood at 5.79x, better than the industry median of 1.17x, indicating decent liquidity for the company than its peer group.

Key Metrics (Source: Thomson Reuters)

Key Risks: The company is susceptible to various risks such as foreign currency risk, interest rate risk, credit risk, commodity price risk, and liquidity risk.

What to Expect: As per the release, the company is determined to continue growing via discovery, development, operation and organic growth of mineral resources. Being an established producer and exporter of hematite iron ore, company’s strategy is to expand its profile as a successful and profitable supplier of raw materials. The company aims to grow its cash reserves and continue to pursue an appropriate balance between the retention and utilization of its cash reserves for value-accretive investments. Its key business objectives for FY20 includes (1) completion of the current program of Extension Hill low grade sales; (2) completion of the ramp-up of ore production at Koolan Island and sales in-line with the mine plan to maximize cashflow and capitalize on favorable market conditions; (3) continue to drive for sustainable cost improvements across the existing business; (4) maintain an appropriate yield on the group’s cash and investment reserves; and (5) continue to search for acquisition opportunities in the resources sector.

FY20 Guidance: Company expects total sales of 3.7-4.0 Mwmt of iron ore at an average group cash cost of $70-75/wmt for the FY20. Group cash costs include all operating, capital, royalties and corporate costs. Koolan Island is expected to contribute 2.7-3.0 Mwmt of high-grade DSO, with site cash costs expected to average $72-77/wmt FOB, including capitalized waste stripping. Unit costs at Koolan Island are projected to progressively decline over the mine life, in-line with the mine schedule as the strip ratio reduces each year. The Mid-West is expected to contribute around 1.0 Mwmt at an average cash cost of $40-45/wmt FOB, comprising the sale of remnant low grade material from stockpiles at Extension Hill.

FY20 Guidance (Source: Company Reports)

Key Valuation Metrics (Source: Thomson Reuters)

Valuation Methodology: Price to Cashflow based Valuation

Price to Cashflow based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, *NTM-Next Twelve Months

Stock Recommendation: The stock of the company generated positive YTD return of 53.40% and is trading slightly below the average of 52 weeks high and low of $1.305 and $0.435, respectively with reasonable PE multiple of 6.30x. This indicates a decent opportunity for accumulation. Moreover, the Company’s bottom-line grew by 34.61% on previous year. Further, total sales of 3.7-4.0 Mwmt of iron ore is expected for FY20, at an average group cash cost of $70-75/wmt, which will help the company to enhance its top-line and bottom-line growth. Its profitability margin for FY19 was impressive with decent return on equity and liquidity position to fund its short-term obligations. Looking at the business prospects over the long-term, we have valued the stock using a relative valuation method, i.e., Price to Cashflow multiple and arrived at a target price of double-digit growth (in % term). Hence, we give a “Buy” recommendation on the stock at the current market price of A$0.745 per share, down 1.325% on 2 October 2019.

MGX Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...