Company Overview: Monadelphous Group Limited is a holding company. The Company's services include fabrication, modularization, offsite pre-assembly, procurement and installation of structural steel, tankage, mechanical and process equipment, piping, demolition and remediation works; multi-disciplined construction services; plant commissioning; electrical and instrumentation services; process and non-process maintenance services; front-end scoping, shutdown planning, management and execution; water and waste water asset construction and maintenance; irrigation services; construction of transmission pipelines and facilities; operation and maintenance of power and water assets; heavy lift and specialist transport; access solutions, and dewatering services. The Company operates in resources, energy and infrastructure industry sector. Its subsidiaries include Monadelphous Engineering Associates Pty Ltd, Monadelphous Properties Pty Ltd, Monadelphous Engineering Pty Ltd, Genco Pty Ltd and M&ISS Pty Ltd.

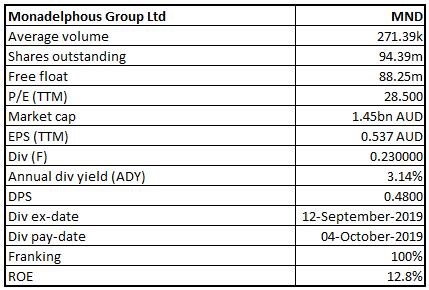

MND Details

Focus Towards Maximising Returns from Core Markets: Monadelphous Group Limited (ASX: MND) is engaged in the provision of engineering services in Australia. As on October 17, 2019, the market capitalization of MND stood at ~A$1.45 billion. Recently, the company reported a decent performance for the year ended June 30, 2019 amidst challenging environment, and it has secured a new contract and contract extension valued at approximately $1.35 billion since beginning of 2019 financial year, which will support to improve its topline growth in years to come. Furthermore, the company aims to increase its earnings by maximising the returns from its core markets, building an infrastructure business, and delivering core services to overseas markets. The company’s revenue amounted to $1.608 billion for the year ended June 30, 2019 which was in line with the guidance given to the market. Statutory revenue, which excludes Monadelphous’ share of revenue from joint ventures, was $1,477.3 million. Its underlying net profit after tax amounted to $57.4 million. As stated, the company’s maintenance and industrial services division encountered record annual revenue performance amounting to $998.4 million, reflecting a rise of 19% on a YoY basis, because of higher activity levels in iron ore and offshore oil and gas markets, as well as strengthened demand for services more broadly. The company has managed to secure $1.35 billion of new contracts and extensions since July 1, 2018, which includes more than $500 million of the resources construction contracts, that reflect renewed confidence with respect to the sector.

It was further added that the major construction contracts were secured in Western Australia (WA) at BHP’s South Flank Project and, as was announced recently, Rio Tinto’s West Angelas Project in Pilbara and Albemarle Lithium’s new Kemerton lithium hydroxide plant. The company has strengthened its position in the infrastructure sector, and there was revenue growth, which was achieved in water and renewable energy markets. The company is possessing robust balance sheet as, at the end of the year, it was having a cash balance of $164 million, cash flow from operations amounting to $16.0 million and cash flow conversion rate of 54%. The company has declared final dividend amounting to 23 cents per share, which resulted in the full-year dividend of 48 cents per share (fully franked), implying a dividend pay-out ratio of around 90% of reported NPAT. The company’s Dividend Reinvestment Plan would be applying to the final dividend.

Considering the decent dividend pay-out ratio and robust balance sheet position, we are affirmative on the stock and expect that it might witness respectable growth moving forward. Hence, considering these parameters, we have valued the stock using 3-year average P/E market multiples of ~22.57x to FY20E consensus EPS of $0.74 and have arrived at a target price of high single-digit growth (in percentage term). At CMP of $15.41, the stock of the company is trading at P/E multiple 16.38x of FY20E EPS.

.png)

Key Financial Highlights (Source: Company Reports, Thomson Reuters)

Top 10 Shareholders: The following table provides a broader overview of the top 10 shareholders in Monadelphous Group Limited:

.png)

Top 10 Shareholders (Source: Thomson Reuters)

Understanding MND’s Key Margins: The company’s net margin stood at 3.5% in FY19, which is higher than the industry median of 2.7% and, thus, it can be said that MND has better capabilities to convert its top-line into the bottom-line as compared to the broader industry. The operating margin of the company stood at 5.6% in FY19, which is higher than the industry median of 4.8%. The company’s RoE stood at 12.8% in FY19, which is higher than the industry median of 9.9% and, therefore, it can be said that MND has been generating better returns to its shareholders as compared to its peer group. MND’s current ratio stood at 2.02x in FY19, which is higher than the industry median of 1.14x and, therefore, it can be said that it is in a better position to meet its short-term obligations. Also, decent base of liquidity level reflects that MND would be able to make deployments towards the strategic business activities which could help in long-term growth. The company’s Debt/Equity ratio stood at 0.10x while the industry median stood at 0.46x and, thus, it can be said that the company has a deleveraged balance sheet when compared to the overall industry.

.png)

Key Metrics (Source: Thomson Reuters)

Announcement About Contracts Update: Monadelphous Group Limited has made an announcement that it has been awarded a major construction contract at Albemarle Lithium Pty Ltd’s new Kemerton lithium hydroxide plant, which is in south-west region of WA. As per the contract, the company would be delivering pyromet structural, mechanical and piping (or SMP) package of work, and associated piping fabrication for Albemarle’s lithium hydroxide plant. The release also added that the work would be completed by early 2021.

Expansion of Rail Maintenance Service Offering: The company has made an announcement that it has been awarded contract for the provision of the services to Rio Tinto on its privately-owned rail network in Pilbara region of WA. The maintenance and industrial services division of the company would be providing maintenance services across 3 packages of the work under 3-year contract, with 2 three-year extension options. The contract, which has been valued at around $60 million, strengthens the position of the company in rail sector.

Understanding Strategic Progress of MND: The company has made good progress in the markets and with respect to its growth strategy to maximise returns from the core markets, build infrastructure business and deliver core services to overseas markets. The engineering construction division has wrapped up the work at Ichthys Project Onshore LNG Facilities in Darwin, Northern Territory early in the period. Monadelphous Group Limited’ robust execution and safety performance throughout project resulted in award of the significant levels of complex additional work and enabled the company to broaden the experience in oil and gas market and showcase the capabilities of execution to numerous potential new customers.

The company’s maintenance and industrial services division witnessed higher levels of demand with regards to the resources sector for sustaining capital works and shutdown services, and growth in the activity levels in the offshore oil and gas maintenance services contracts. It was also mentioned that award of $240 million 3-year general maintenance services contract with BHP for Pilbara iron ore mine sites has strengthened leadership position of the company in the market.

Dividend Pay-Out Ratio Stood ~90% in FY19: The company’s Board has declared the final dividend amounting to 23 cents per share (fully franked). As a result, its full-year dividend amounted to 48 cents per share (fully franked), reflecting a dividend payout ratio of around 90% of the reported NPAT. It was further added that the Dividend Reinvestment Plan would be applied to the final dividend. The balance sheet of the company happens to be robust and it provides the company with substantial capacity to deploy towards suitable new business opportunities, which might arise. Over the last five years, the dividend payout ratio of MND has been improving. In FY15, MND’s dividend payout ratio came in at ~80.8% and finally, in FY19, the payout ratio was ~90.0%. The annual dividend yield of the company is about 5.7% on a five-year average basis (FY15-19). At the current market price of A$15.41 per share, the annual dividend yield of MND stood at 3.14%.

.png)

Dividends Per Share (Source: Company Reports)

During FY19, the company’s management has decided to pay dividends amounting to $53,673,000. The company’s policy is to payout dividends in the range of 80%- 100% of the annual net profit after tax. However, it remains subject to working capital requirements, potential investment opportunities as well as business and economic conditions generally.

What To Expect From MND Moving Forward: There are expectations that the resources and energy sectors in Australia might provide robust pipeline of opportunities over the upcoming years as more positive market conditions return. It was further added that the project development activity is increasing, and numerous resources construction opportunities are coming to the market, primarily in the iron ore and lithium sectors. There are anticipations that the prospects from further development in LNG production might be positive in the coming years. The maintenance activity with respect to resources market has been anticipated to be robust because production levels in Australia are at record levels. The customer focus on optimising the production and rising productivity levels would continue to drive demand for the ongoing maintenance support and sustaining capital work.

The company stated that the growth prospects over longer-term are favourable and the revenue for 2019/20 financial year would be dependent on the timing of the execution of work which has been secured recently, and value and timing of the future successful awards of the additional resources construction contracts.

.png)

Key Valuation Metrics (Source: Thomson Reuters)

.png)

Historical PE Band (Source: Thomson Reuters)

Stock Recommendation: On YTD basis, the company’s stock has delivered a return of 10.26%. At the current market price of A$15.410 per share, the annual dividend yield stood at 3.14%. There are expectations that the return of more favourable core market conditions might provide a robust pipeline of opportunities in years to come. Also, LNG prospects are anticipated to be positive moving forward. The company has strengthened its position in the infrastructure sector, with renewable energy joint venture Zenviron, which has been making good progress on projects secured in the prior period and securing 3 additional wind farm contracts. Moreover, the company has been awarded a significant number of new major construction and maintenance contracts since the beginning of the calendar year 2019, and considering the strong reputation and broad service offering, the company happens to be in good shape in order to continue to capitalise on the strengthening market conditions. Considering these parameters, we have valued the stock using 3-year average P/E market multiples of ~22.57x to FY20E consensus EPS of $0.74 and have arrived at a target price of high single-digit growth (in percentage term). Hence, we give a “Buy” recommendation on the stock at the current market price of $15.41 (up 0.653% on 17 October 2019).

MND Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...