Kalkine has a fully transformed New Avatar.

Company Overview - Mobile Embrace Limited is a mobile marketing and carrier billing m-commerce company. The Company's principal activities include mobile commerce. Its segments include Carrier Billing and Mobile Marketing. It offers its partners integrated customer acquisition, management and carrier billing through mobile devices. It enables reaching of, engagement and transactions with consumers on their mobile devices through its digital media trading desk and carrier billing platforms. The consumers engage with digital product and service offerings, and utilize carrier billing to pay for them on their mobile devices. It also enables the reaching of, engagement and transactions with consumers on their mobile devices through its mobile marketing platforms, permission databases, publishing network and mechanics. Its carrier billing products include video-on-demand, mobile security, fitness, games, education and sports. The Company operates in Australia, the United Kingdom, Singapore and New Zealand.

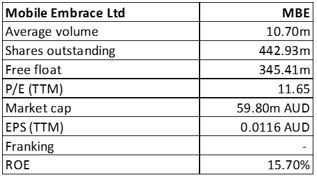

MBE Details

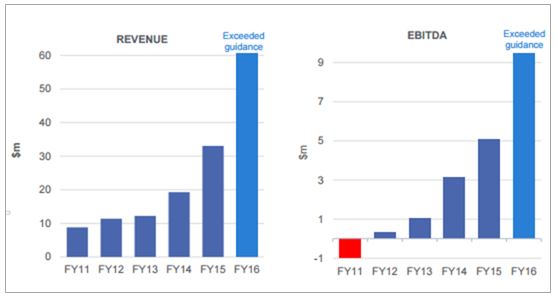

Delivered a solid top line growth for fiscal year of 2016: Mobile Embrace Ltd (ASX: MBE) has reported 83% growth in the revenue to $60.6 million on year over year basis on fiscal year of 2016 ahead of the company’s guidance. The EBITDA grew 86% to $9.5 million against the prior corresponding period (pcp) which is also ahead of the company’s guidance. As a result, the group’s NPAT grew 63% to $4.9 million as compared to FY 15 while the earnings per share has grown 57% to 1.26 cents. Moreover, MBE has posted a five-year compounded growth rate for revenue of 40%, while the EBITDA has grown at the CAGR of 100%. MBE earnings per share has grown at the CAGR of 325% from the past five years.

Financial Performance for FY 16 (Source: Company Reports)

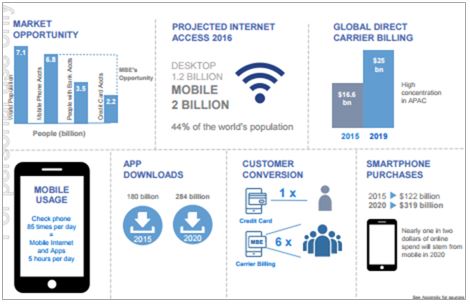

Positioning to leverage the growing market opportunity: MBE will benefit from the global uptake of mobile and is accordingly positioning themselves in a strategic manner. The mobile sector is very strong with the mobile marketing and carrier billing sectors growing. There is a heavy growth in the consumer engagement and the way through they transact through their mobiles are growing at the rapid pace. Moreover, the projected internet access in 2016 from mobile is 2 billion consisting of 44% of the world’s population compared to 1.2 billion of desktop users. The mobile usage is high as it is estimated that people check phone 85 times the day and there are 5 hours per day usage of mobile internet and apps. Additionally, the apps download is expected to grow from 180 billion in 2015 to 284 billion in 2020. Given these strong prospects, MBE has invested for the expansion of the operational infrastructure from the July 2015 to August 2016, while the company has established four international territories for direct carrier billing and new International territories for mobile marketing. The carrier billing is in ten countries and has a capacity to expand into ten more countries for which new territories are pending.

Global Opportunity for mobile (Source: Company Reports)

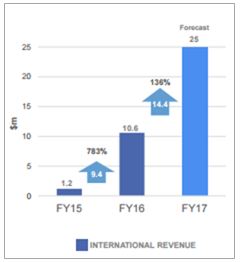

International Growth Potential: MBE has posted a strong global organic growth in 2.5 years, and intends to have a presence in 16 countries by November 2016. Mobile Embrace expects to grow into more than 30 countries by 2019. The telcos number in terms of carrier billing was 24 in 2016 which is expected to be more than 50 by 2019 and the addressable market for carrier billing is expected to grow more than one billion in 2019 from 340 million in 2016. Moreover, the international revenue is forecasted to grow more than $25 million, which is a growth of 140% from $10.6 million in FY 16. Additionally, the international transactions have grown 100% since June 2016.

International Revenue (Source: Company Reports)

Growth in the Proprietary Data Assets and Technology: MBE is growing the proprietary assets to enable the targeted acquisition of customers at massive scale. Additionally, the monthly transactions have increased 50% from 2 to 3 million in FY 16. MBE is growing data assets in multiple territories to deliver strong annuity revenues. Moreover, there are commercial benefits like higher quality data turns consumers into customers through targeted marketing and the businesses pay more for the delivery of the quality customers. Meanwhile, MBE is even enhancing the technology platform assets to continue strengthening its competitive advantages and scalability. MBE is rolling out MOBIPAY NINJA, the new proprietary billing and customer management platform. The new automation features are now available on Mobile Marketing Platform and new business products have also been launched on the platform. Additionally, there are commercial benefits for the technology for better customer conversion rates and diversification, faster and cost effective global carrier integration and the mobile digital marketing platforms are generating new parallel revenue streams.

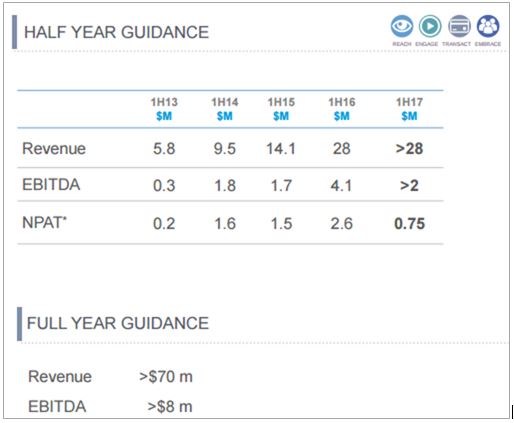

Market Update for 1H FY 17: MBE has to regularly adjust operations to carrier billing compliance changes and the recent Australian telco carrier billing changes has caused a one-off event that has adversely affected MBE’s ability to acquire customers, (in Australia only), within target cost of acquisition (CPA) and scale ranges. Though CPA is now improving, and to reduce this effect the marketing spend has been reduced until ROI metrics become favorable again. The adjustment will impact the first half FY 17 revenue by circa $3.8 million and EBITDA by $1.7 million. On the other hand, MBE has confirmed the strong growth of the international direct carrier billing (DCB) operations. MBE has continued to diversify its DCB operations through the expansion of telco and territory footprint of its international roll-out. International monthly DCB revenue is tracking at more than $2,450,000 for the second quarter and is on track to grow 23% quarter on quarter. Moreover, MBE is expanding the international DCB footprint and expects to enter two additional new markets shortly. The international DCB business is already on a circa $10m per annum run rate in the current quarter. MBE expects the run rate will continue to increase through the second half year of FY 17 as more telcos and territories launch and anticipate Q4 exit run rate will be more than $5 million.MBE expects the revenue of more than $28 million in the 1H FY 17 which the company has reported for FY 16. The group forecasts a revenue of more than $70 million for full year. Moreover, MBE is expecting EBITDA of $2 million for the first half of FY 17 and the EBITDA of more than $8 million for full year.

Financial Performance Guidance (Source: Company Reports)

Agreement with Dtac: MBE has signed the new agreement with Dtac, which is a subsidiary of Telenor to expand its international DCB operations in Thailand. Dtac is the second largest mobile telecommunication provider and has 25.5 million mobile subscriptions. Further, this agreement would strengthen MBE’s position in Asia as this will add to the agreements already established in Singapore, Pakistan and Malaysia. Additionally, due to the growth of streaming services and superior 4G experience there is demand and market opportunity for MBE’s DCB products and services.

Update in relation to the Supreme Court Litigation: MBE in relation to the Supreme Court Litigation has quantified the amount of its cross claim against the Plaintiffs which is in the range of $4 million and 11 million. MBE would continue to deny the claim by GBD in entirety and will continue to pursue its cross claim. If MBE succeeds in its cross claim, while the amount recoverable is not known now. Moreover, the pleadings have closed and the exchange of the written evidence is expected to be finalized in the late January 2017 and the directions hearing is expected in later half of the next year.

Stock Performance: The shares of MBE stock fell over 53.57% in the last four weeks (as of November 26, 2016) impacted by the softness in guidance update from the group for fiscal year of 2017. Moreover, compliance to the recent changes in Australian telco carrier billing impacted marketing channel partners and thus the group’s ability to win new clients. On the other hand, the fall can be looked as an entry opportunity while the group still has a significant market opportunity in several underpenetrated regions while international operations are on track. The stock has been up 3.8% on November 29, 2016. We give a “Buy” recommendation on the stock at the current price of – $ 0.13

MBE Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Please wait processing your request...

Please wait processing your request...