Kalkine has a fully transformed New Avatar.

Company Overview: Mirvac Group (ASX: MGR) is a leading, diversified, Australian property group which delivers innovative and exceptional workplace, retail destinations, high-quality homes, and connected communities for its customers. The company’s investment portfolio includes assets across the office, industrial and retail sectors. Mirvac Group is the creator, owner and manager of some of Australia’s most renowned and recognisable projects. The company’s aim is to enhance the value of Australia’s cities through innovative, visionary design, development, asset management and construction..png)

MGR Details

.PNG)

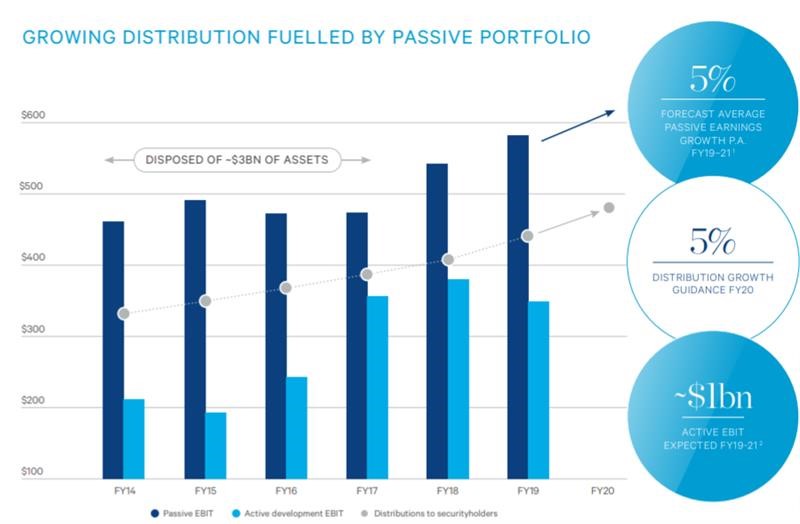

High-Performing Investment Portfolio with Steadily Growing Income: Mirvac Group (ASX: MGR) is Australia’s leading property group known for delivering innovative and exceptional workplace precincts, retail destinations, high-quality homes and connected communities for its customers. The company has kept itself diversified by maintaining an appropriate balance of passive and active invested capital through cycles and retaining capability across the office, industrial, retail and residential sectors. The company holds a high-performing investment portfolio which continues to generate a steadily growing income. Further, the company’s integrated business model helps it to produce strong, visible and secure cash flows, sustainable distribution growth and attractive returns on invested capital. From 2015 to 2019, the company’s profit attributable to the stapled securityholders has increased at a CAGR of 13.69%. For the same time period, the company’s annual distributions have increased at a CAGR of 6.97%..png)

Past Financial Performance (Source: Company Report)

Going forward, the company continues to focus on its urban strategy of providing secure cashflows and sustainable distributions. Mirvac Group is well-positioned to mitigate adverse market cycles and use them to its advantage by capitalising on the opportunities they present. The company’s high-quality investment portfolio continues to provide secure and growing income while its development pipeline and asset creation skillset provide significant potential for future growth. Although the company has been recently impacted by the Covid-19 pandemic, it continues to work on its development pipeline, exploring a range of additional opportunities and improving its capabilities, in order to expedite the recovery process.

FY19 Performance Highlights : In the financial year 2019, the company achieved a statutory profit of over $1 billion for the fourth consecutive year. At an operating level, the company’s profit was up 4% to $631 million, representing 17.1 cents per stapled security. The company’s performance during the year was underpinned by the significant gains of its Office & Industrial business and its high-quality investment portfolio. During the year, Mirvac Group achieved a strong operating cash flow of $518 million and paid distributions of 11.6 cents per stapled security, up 5% on last year. Over the year, the company reported 4% EPS growth, 8% NTA Growth, 10.1% Group ROIC.

In FY19, the company successfully completed a fully underwritten institutional placement and Security Purchase Plan (SPP) to position the business for future growth. Under the placement, the company raised $796.2 million, to support the delivery of the next generation of value accretive office, industrial, residential and mixed-use projects and to provide additional funding impetus for continued investment through the cycle..png)

FY19 Results Snapshot (Source: Company Reports)

Half-year Performance Highlights: In the first half of FY20, the company witnessed strong performance across its business, driven by its passive income stream from $12.0 billion modern investment portfolio. For the period, Mirvac Group recorded a profit attributable to stapled unitholders of $546.5 million and Operating profit after tax of $352 million. Benefits from a strong increase in operating earnings were offset by lower revaluation gains. During the period, the company declared half year distribution of $240.0 million, representing 6.1 cents per stapled unit.

In the Office & Industrial division, the company saw a strong increase in Property NOI driven by Office LFL NOI growth of 5.6%, offset by lower development earnings compared to the prior period. In the Residential division, the company achieved over 800 sales in 1H20, with strong results at new releases in Victoria at Smiths Lane, The Fabric at Altona North and the Folia apartments in Tullamore..png)

H1FY20 Results Snapshot (Source: Company Reports)

Sustainable Distribution Growth: Through its integrated business model, the company has continued to enjoy sustainable distribution growth and attractive returns on invested capital. In FY19, the company paid distributions of 11.6 cents per stapled security, up 5% on last year. In the first half of FY20, the company paid a distribution of 6.1 cents per stapled security, up 15% on pcp. Before Covid-19 pandemic, the company was expecting to pay a distribution of 12.2cpss in FY20, however, due to the uncertainty surrounding the pandemic, the company has withdrawn its guidance.

Distribution Growth (Source: Company Reports)

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together forms around 29.45%. The Vanguard Group, Inc. and APG Asset Management N.V. hold the maximum interest in the company at 10.56% and 3.76%, respectively..png)

Top 10 Shareholders (Source: Refinitiv (Thomson Reuters))

Capital Efficient Acquisition of a Landmark Site in Willoughby: On 7 February 2020, the company announced that it has entered into an agreement to acquire a landmark site currently occupied by Nine Entertainment Co. in Willoughby from LEPC9 Pty Ltd. Historically, the site was occupied by Nine Entertainment Co., has a concept plan approval for the development of 460 new dwellings and approximately 6,000 square metres of public open space. This acquisition reinforces the company’s ability to identify and secure opportunities on capital efficient terms, and it extends the company’s residential pipeline, enabling it to service the growing demand for new homes, as the housing market continues to recover.

A Quick Look at Key Margins: For H1FY20, the company’s occupancy rate stood at 99.1%, up 0.3% on pcp. For the same time span, the company reported EBITDA margin of 30.1%, in line with the pcp. The company has a current ratio of 1.02x, higher than the industry median of 0.64x, demonstrating that the company is well equipped to pay its short-term obligations. .png)

Key Metrics (Source: Refinitiv (Thomson Reuters))

Tackling Covid-19 Pandemic: The company entered the COVID-19 pandemic with a strong balance sheet. In order to protect its employees, other stakeholders, as well as the long-term viability of the business, the company is undertaking a range of measures including implementing best practice hygiene standards and social distancing measures across all sites; putting in place a remote working directive from 16 March; consulting with State and Federal Governments on multiple issues throughout the period; a voluntary reduction in working hours for most employees, from 1 May to 30 June. The company continues to assess the impact of COVID-19 on its operations and financial position, in order to help the business, rebound as quickly as possible.

Key Risks: Mirvac Group is exposed to several external environmental factors that present challenges to all participants in the Australian Residential Market Industry. As a property group involved in real estate investment, the company faces a number of risks throughout the business cycle that have the potential to affect the achievement of its targeted financial outcomes. Recently due to the restrictions put by the government to tackle COVID-19 impacts, the company’s retail portfolio witnessed a sharp change in sales performance. CBD and tourism based centres have also been severely impacted, with smaller centres based around essential goods and services performing fairly in comparison. Despite this, the company is starting to see opportunities emerge beyond this current crisis. It is working closely with the Government to fast track a number of sites at various stages of the planning cycle, which will help it rebound as quickly as possible and support the wider economic recovery.

What to expect: Going forward, the company continues to focus on its urban strategy of providing secure cashflows and sustainable distributions. Due to the uncertainty caused by the COVID-19 pandemic, the company has recently withdrawn its earnings and distribution guidance for FY20. Despite the near-term negative economic impact, Mirvac’s purpose and unique urban asset creation capability position it well to capture opportunities and generate value, throughout the recovery process and beyond.

As per the recently released Q3FY20 update, in the Office & Industrial division, the company is fast tracking its $5.4 billion future development pipeline, to ensure that it is in the best possible shape to benefit from the eventual recovery. Further, the company expects, the accelerated growth of e-commerce to support strength in demand for high-quality logistics and last mile facilities in key urban markets. In the residential space, the company expects the challenges to continue in the near future, however, to deal with these challenges, Mirvac has transitioned to virtual sales offices and private viewings by appointment..png)

Key Valuation Metrics (Source: Refinitiv (Thomson Reuters))

Valuation Methodology: Price to Sales Based Market Multiple Valuation (Illustrative).png)

Price to Sales Based Market Multiple Valuation Method (Source: Refinitiv (Thomson Reuters))

Stock Recommendation: In the current challenging environment, the company has bolstered its short-term resilience, and has maintained its focus on the future. The company currently has a robust balance sheet to support future growth through cycle.The stock of MGR has corrected by around 38.42% in the past three months and is currently trading below the average of its 52-week low and high of $1.650 and $3.525, respectively. Considering the growth potential in the long run, we have valued the stock using price-to-sales based market multiple approach and arrived at a target price of lower double-digit growth (in percentage terms). Hence, considering the company’s fundamentals, 1H FY20 financial performance, strong balance sheet, and current trading levels, we give a “buy” recommendation on the stock at the current market price of $2.240, up by 6.667% on 30 April 2020, owing to the recent quarterly update.

MGR Daily Technical Chart (Source: Refinitiv (Thomson Reuters))

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...