Company Overview - Mineral Deposits Limited (MDL) is an Australia-based company focused on the mineral sands sector through the joint venture interest in TiZir Limited (TiZir). MDL and ERAMET SA each own 50% of TiZir, which owns the Grande Cote Mineral Sands Project in Senegal, and the Tyssedal ilmenite upgrading facility in Norway. The Grande Cote Mineral Sands Project is located on the coast of Senegal starting approximately 50 kilometers north of Dakar and extends northwards for more than 100 kilometers. The main Heavy Mineral (HM) deposits identified to date are Diogo, Mboro, Fass Boye and Lompoul.

Analysis - Mineral Deposits Limited (MDL), the Australian based finding, mining and processing mineral sands resources, is our focus for today. The Company owns 50% of TiZir Limited which owns the Grande Côte mineral sands mine in Senegal, West Africa, and an ilmenite upgrading facility in Tyssedal, Norway.

As at 30 September 2014, the Company’s issued shares were 103,676,341 while cash was US$27.3 million. MDL reported zero debt and investments included 19.1% of World Titanium Resources valued at US$1.8 million. Mining and production at Grande Côte is expected to ramp up into 2015. It is further expected that production will be around 85ktpa of zircon and 575k tpa of ilmenite in view of full production over a mine life of about 20 years. The Tyssedal ilmenite upgrading facility smelts ilmenite to produce a high?TiO

2 titanium slag which is sold to pigment producers and a high purity pig iron which is sold as a valuable co-product to ductile foundries. This facility produces about 200ktpa of titanium slag and 110ktpa of high?purity pig iron.

Grande Côte Mining Operation (Source – Company Reports)

The ramp?up of the mineral separation plant is progressing well. Wet plant and the ilmenite plant are operating to design feed rates. On?spec standard zircon was also produced within days of initiating the operations. The Company has been successful in making first shipments of sulphate ilmenite, chloride ilmenite and zircon. The Tyssedal plant in Norway also is operating as per the Company’s expectations.

Earlier, there were interruptions owing to impellor failures of the main dredge pump in August 2014 for the Grande Côte Mining operations, which are now on the ramp-up mode. Mining throughputs are witnessing upsurge owing to security of having multiple spare impellors on site and tails from the Wet Concentrator Plant (WCP). Design changes etc. are being made to overcome failures.

The Company further confirmed that an expected increase in mining rates may help it to achieve steady state throughput of 4.5 million tonnes per month in the third quarter of next year.

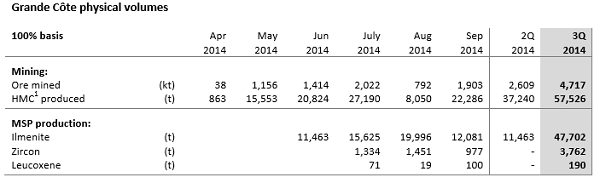

The Company also stated that Grande Côte’s first shipment of about 5,000 tonnes of chloride ilmenite from Dakar port on 28 August was followed by a shipment of about 22,000 tonnes of sulphate ilmenite late September.

Grande Côte Physical Volumes (Source – Company Reports)

Grande Côte Physical Volumes (Source – Company Reports)

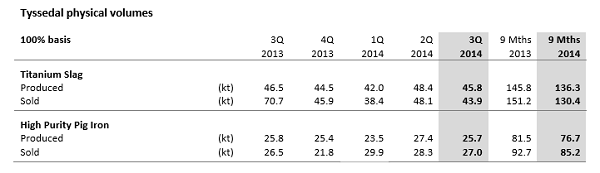

Over 1,200 tonnes of containerized zircon was also shipped during the quarter. In October, the Company intended to make the first shipment of ilmenite to the Tyssedal plant. Tyssedal Titanium slag production of 45.8kt for the third quarter was as per the 3Q 2013 production, though weaker than 2Q 2014 output. Sales of 43.9kt for the quarter were marginally lower than production levels. Pricing was also slightly weaker in 3Q relative to 2Q. On the other hand, the Company reported a high purity pig iron production and healthy sales volumes for 3Q at 25.7kt and 27.0kt respectively, while pricing in 3Q was consistent with 2Q. Cost cutting initiatives were successful throughout the year to date.

Tyssedal Physical Volumes (Source – Company Reports)

Tyssedal Physical Volumes (Source – Company Reports)

As per the Company’s financial results for the half?year ended 30 June 2014, Tyssedal was profitable with EBITDA of $11.3 million even during harsh market conditions. TiZir was also reported to be well?funded with $74 million of cash with $48 million undrawn on the Tyssedal working capital facility. Also, a further $50 million facility was being discussed for the Grande Côte.

Looking at the conventional wet mining zone, MDL reported that dredge sucks sand from front of pond and pumps slurry to floating WCP. Further, spirals gravity then separates 2% heavy mineral concentrate (HMC) from 98% lighter quartz sand within the WCP.

Conventional Wet Mining –Dredge and Floating Concentrator (Source – Company Reports)

Conventional Wet Mining –Dredge and Floating Concentrator (Source – Company Reports)

With regards to the Mineral Separation Plant (MSP), the magnetic, electrostatic and gravity processes separate HMC into various minerals including zircon, ilmenite, rutile and leucoxene. MDL’s own power plant (36MW HFO/Diesel/Gas) provides power for running the operations. The judgment to build a purpose built mine while employing a new plant appears to pay off with the MSP performing in harmony with the scheduled timeframe.

Grande Côte Mineral Separation Plant (Source – Company Reports)

Grande Côte Mineral Separation Plant (Source – Company Reports)

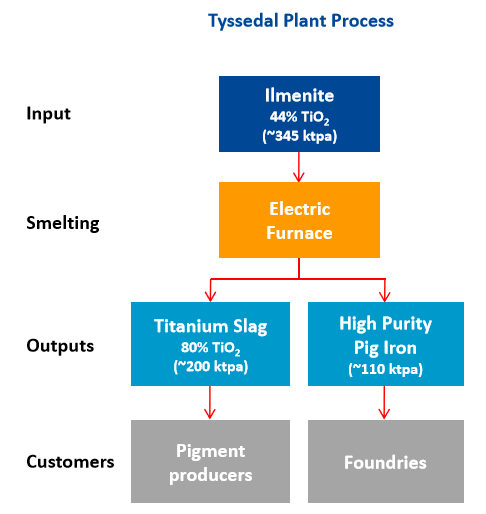

For Tyssedal, the Company is upgrading ilmenite to a high?TiO

2 feedstock and plans for a 15% capacity increase during a major scheduled maintenance program in 3Q 2015. Further, nameplate production is expected in 2H15 for supplying to the Tyssedal smelter in Norway that is set to be expanded by 15% to 230kt pa. At present, Tyssedal can only use ~30% of Grande Côte’s ilmenite production at nameplate levels. An analysis of this outlines that TiZir’s net long ilmenite position stands at ~400kt pa, which is ~3% of global supply, thus appearing to be at risk to the discounting in view of the fact that incremental ilmenite tonnes are mostly sold into the Chinese market. Nonetheless, the position in North America / Europe coupled with Tyssedal’s TiO

2 marketing skills may prove to offset the aforesaid issue.

Tyssedal Plant Process (Source – Company Reports)

Tyssedal Plant Process (Source – Company Reports)

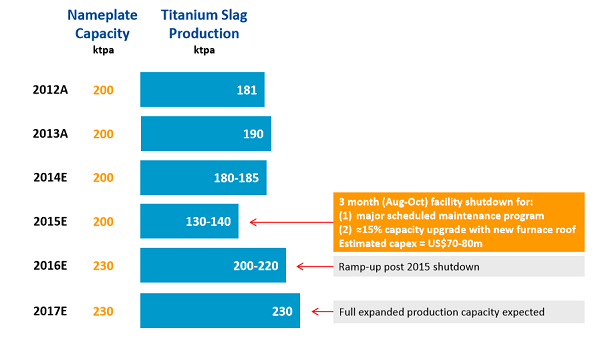

MDL also believes that Tyssedal will be able to produce sulphate slag or chloride slag post the planned capex program in 3Q 2015.

Growth Plans (Source – Company Reports)

Growth Plans (Source – Company Reports)

MDL may need to raise capital in view of the account for an undrawn $50mn facility TiZir has with a Norwegian Bank. In such case, it is thought that TiZir may be able to maintain some cash and debt allowance in June 2015 if it succeeds in raising another $50mn in debt. However, we note that TiZir’s bond is repayable in Sep 2017 leaving little time to generate the cash. Refinancing of the facilities may thus be on the cards.

MDL Daily Chart (Source - Thomson Reuters)

MDL Daily Chart (Source - Thomson Reuters)

The Company is also wary of certain factors such as inherent risks involved in exploration and development of mineral properties, fluctuations in economic conditions, changes in the price of zircon, ilmenite and other key inputs, changes in mine plans and other factors, such as project execution delays, etc.

The complete ownership of infrastructure with in-site gensets, direct rail access from mine to port, loading facilities and such other features, is specific to MDL contrasting most of other mineral sand mines. This enables MDL to operate entirely on its own with markets and pricing as the only uncontainable factors. Given the entire game plan and deep value forecast wherein the ramping up of Grand Côte mine appears to act as the key promoter, we put a

BUY recommendation for this stock at the current price of $1.305.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...