Company Overview - Metcash Limited is an Australia-based marketing and wholesale distribution company specializing in grocery, fresh produce, liquor, hardware and automotive parts and accessories. The Company business spans across the food and grocery, liquor, hardware and automotive sectors across Australia and a smaller liquor business in New Zealand. Its operating divisions include Metcash Food & Grocery; Australian Liquor Marketers and Hardware & Automotive. Food and Grocery activities consisted of the distribution of dry grocery, perishable and general merchandise supplies to retail outlets. Liquor activities consisted of the distribution of liquor products to retail outlets and hotels. Hardware and Automotive consisted of distribution of hardware supplies and automotive parts and accessories to retail outlets.

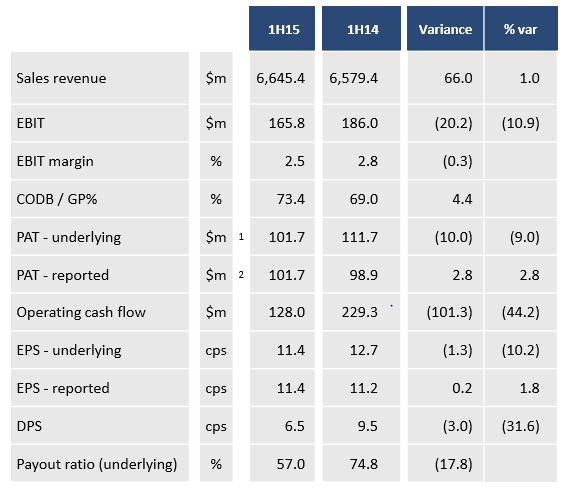

Analysis - Metcash (MTS) released its 1H15 results sometime back confirming the need for uplifting the Food & Grocery business. The Company has indicated a solid net working capital result. Improved gearing mirrored solid operating cash-flows, working capital control and lesser capital investment. As per the Company’s results for the financial half-year ended 31 October 2014, sales revenue increase of 1.0% to $6.6 billion; profit after tax increase of 2.8% to $101.7 million; underlying profit after tax dip of 9.0% to $101.7 million; and underlying EPS dip of 10.2% to 11.4cps has been reported. Operating deleverage and investment in the Food & Grocery strategy led to the decrease of the underlying profit after tax. The interim dividend per share of 6.5 cents fully franked was declared. The Company hinted its intention to maintain DPR of at least 60% for full year in congruence to its policy.

Financial Highlights (Source – Company Reports)

Lesser margin categories impacted EBIT for food and grocery. Even negative wholesale sales growth led to operating deleverage. On the other hand, transformation initiatives in Fresh, Convenience and Black & Gold depicted positive results with retail scan sales going up given transition to shopper-led category management.

New B&G Packaging to be Launched in 2H15 (Source – Company Reports)

MTS reported fresh sales growth of +4.1 % LFL basis with quality improvement and range optimisation program. Healthy retail sales performance in retail bannered independent groups (IBA) boosted operating leverage by increasing EBIT by 6.9% to $24.9 million, in ALM. The sales to wholesale contract independent groups were soft due to market share loss to organised groups and the self-supply chains. The liquor consumption also declined resulting in waning overall volumes leading to a 3.6% dip in ALM’s total sales. Automated full-case pick system, Mustang, has been deployed in NSW for ALM.

As per the MTS updates, Price Match (Competitive Pricing strategy) was activated in 425 IGA stores by the end of October 2014 and three stores piloted the Diamond program in the half with 11 operational and 29 stores approved to proceed. Price Match has upturned the negative sales trajectory in the 425 participating IGA stores and the Diamond Store Accelerator pilot stores have led to an increase in customer transactions and basket size for stores. With additional stores transitioning to Diamond, a sales led recovery is expected.

Diamond Transformation Program (Source – Company Reports)

Healthy performance in the trade sector led to Hardware sales up by 16.5% on last year or 3.9% on a like-for-like basis. However, growth in EBIT was sluggish owing to higher trade sales mix. The addition of G. Gay & Co. and the Yenkens Group stores helped in further growth for network through conversion of stores to the M10 banner.

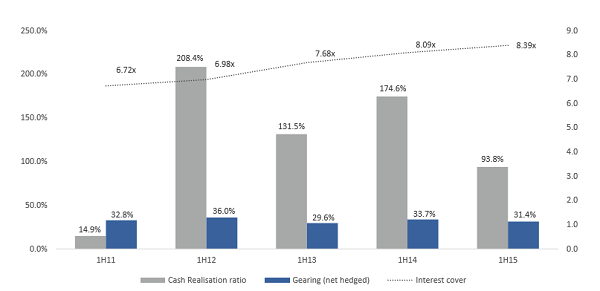

Gearing, Cash Realisation Ratio & Interest Cover (Source – Company Reports)

There was a 21% increase in sales in Automotive on last year in view of strong performance by the core retail business in support of growth through acquisition. There was an extension of service offer by Automotive with the acquisition of Midas. The repositioning and aligning of the ABS/Midas service and value offers has also been stated. There was success in converting 11 other independents to the Autopro and Carparts brands. In fact, six new Autobarn stores are to be opened.

As understood, ALM’s top-line growth has been caught up by 3.6% in view of compliance issues from smaller accounts. Hardware and Automotive division witnessed margin contraction. Nonetheless, EBIT support from smaller divisions have been accelerating. For instance, revenue for the IBA business has been robust. Therefore, some of the above indicate a sign of encouraging future in the early stages of MTS’ five year transformation coupled with the cost control flow through for Food & Grocery and warehouse efficiencies. The benefits are supposedly to be realized in FY16. With the progress of the transformation plan and a little cushioned position, the Company has anticipated FY15 Group EBIT to be $315 - $330 million. MTS is positive on its view despite the highly competitive general trading environment with price deflation and extra-conscious consumer base.

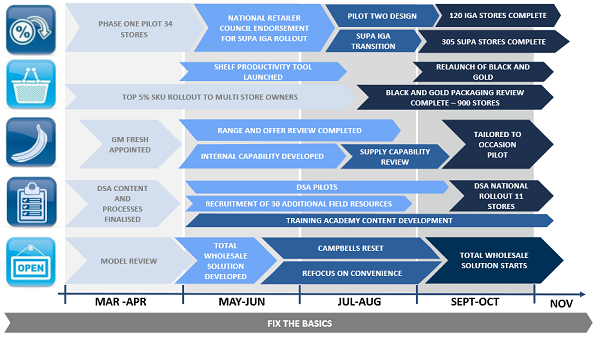

Progress Roadmap (Source – Company Reports)

MTS outlook further entails Diamond programs now gaining traction after the initial lag time to be put in place due to individual retailer sign-up; 50 stores to be completed by the end of FY15 under DSA pipeline; phase 2 pilot in place for smaller store format for Price Match; and sales growth seen and pipeline identified for Convenience. Fresh is also witnessing augmented category ranges targeting buy-as-you-need-shopper driving sales lifts. With regards to B&G, over 900 stores are already on new price program. These few tangible signs of improvement come as a slight relief from what MTS witnessed in 2014 wherein the market cap declined $1.1 billion.

Towards the medium term, it is prudent for MTS to endure price match and overcome issues in the face of entry of Aldi in Western Australia and South Australia from late 2015. In fact, Coles is focused on value with price investments to be funded by cost savings. Woolworths is more confronted with modest value sensitivity in view of EBIT margins appearing a priority. For MTS, the revenue growth has been submissive irrespective of easing petrol discounts with risks related to deflation and competition (Woolworths, Coles, Aldi etc.). Nonetheless, the transformation plan looks to be a sound tactic to overcome challenges in the Food & Grocery division. The risk on execution along with debt refinance are to be taken care at the same time. Further, strong Liquor EBIT performance appears to be a positive. The revenue may have declined 3.6% with wholesale sales down between 4-16% as external banner groups continued to lose share to organised banners and chains, however, EBIT margin improved 16bps to 1.68% given the increase in retail sales (3.5% LFL in a competitive market) and a reduction in CODB/sales through warehouse efficiencies and cost control. Net interest expense was also moderated ($23.9m in 1H15) as opposed to $30.2m in 2H14 and $27.0m in 1H14. This was steered by lower debt utilisation and lower interest rate. It is also to be noted that the outlook for the Australian grocery market is optimistic owing to population growth, inflation and an intense market.

Metcash Daily Chart (Source - Thomson Reuters)

Accordingly, we put a BUY recommendation for this stock at the current price of $1.525.

Please wait processing your request...

Please wait processing your request...