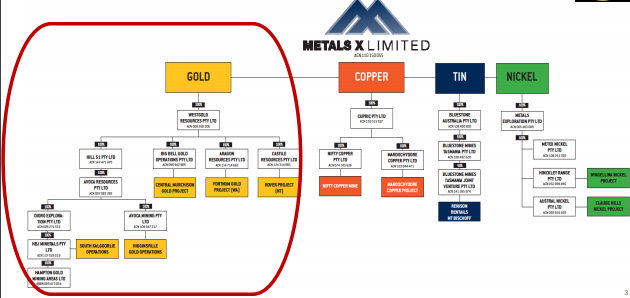

Company Overview - Metals X Limited is an Australia-based exploration company. The Company is engaged in the business of exploring and developing metals and minerals in Australia . The Company operates in three divisions: gold, tin and nickel. The Company's projects include Renison Tin Project, Wingellina Nickel-Cobalt Project, Claude Hills Project, Central Murchison Gold Project (CMGP), Rover Project and Mt Henry Gold Project. The CMGP is located in the Murchison gold province, which is approximately 600 kilometers northeast of Perth in Western Australia. The Renison Project is located on the west coast of Tasmania. The Mt Bischoff is located approximately 80 kilometers from Renison and is a deposit in its own right producing in excess of around 55,000 tons of tin metal. Its Claude Hills deposit is located approximately 30 kilometers to the East of Wingellina. The Company's CMGP and Rover Projects are gold development projects.

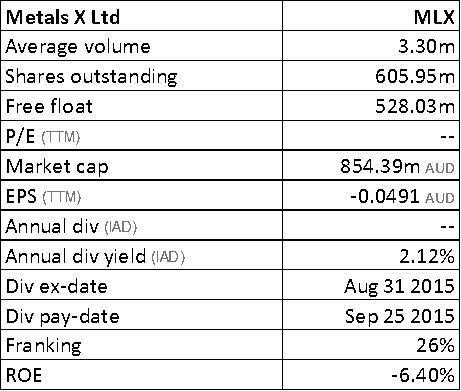

MLX Details

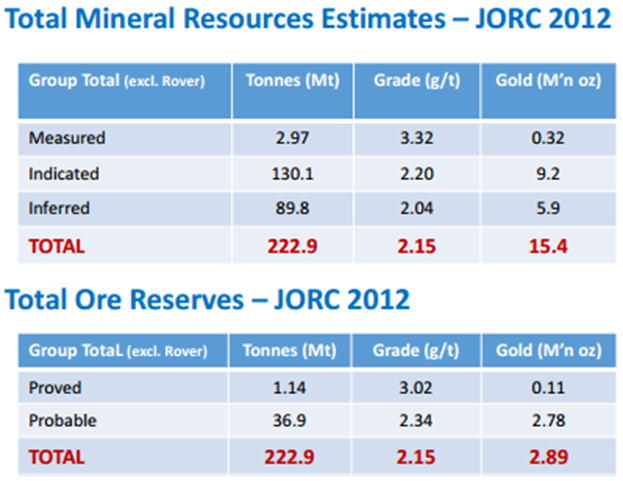

Emerging of a pure play gold player: Metals X Limited (ASX: MLX) via Westgold Resources Limited has three operating gold projects, four process plants with 5.5 million tonnes per annum capacity and has built a gold resource base of 15.4 million ounces and ore reserves of 2.89 million ounces. The fourth project, Fortnum Gold Project comprises a capacity of 70,000 oz per annum, which is under construction and forecasted to end by 2016. MLX currently produces at a run-rate of 250,000 ounces per annum and is targeting to double this over the next few years. Through said move, MLX expects to be a substantial top 10 domestic gold producer and has a target of gold production at the steady run-rate of more than 450,000oz per annum in the next two years at the target AISC of US$965/oz (currently it is A$1225/oz) while the target cash operating cost is US$840/oz (currently it is A$1100/oz).

Total Gold Resources Estimate and the Reserves (Source: Company Reports)

Westgold Resources Limited has excellent margins of US$380/oz (A$500/oz). Additionally, MLX has successfully commissioned the Central Murchison Gold Project (CMGP) process plant in FY 16 and the transition of the HBJ underground mine at South Kalgoorlie Operation completed its main capital phase and near the end of the half-year transitioning into an operating phase.

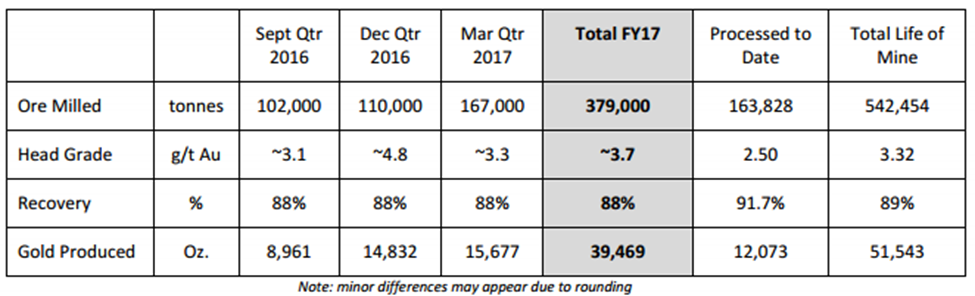

Cannon gold mine upgraded the mine profit guidance:Cannon gold mine, an open pit operation is being operated by MLX in a 50/50 profit share arrangement with Southern Gold. The new review shows that at current gold price of A$1,750/oz, the net profit guidance increases from A$14.9m to A$17.2m. The cash distribution, net of debt facility to MLX has become A$14.5m. Meanwhile, Cannon Mine ore processing has now recommenced at South Kalgoorlie Operation’s Jubilee Mill (SKO) and the mine is now entering into the final phase where the majority of the in-pit gold would be extracted and processed over the next 7 months. The major cutback at the pit has been completed and the significant ore zone is in the lower half of the pit which is now being mined. Assuming no disruptions to the mine schedule, the open pit mining would finish during December 2016 with stockpiled ore processed until the end of March 2017. The project is cumulative cash flow positive in November and cash distributions to MLX and Southern Gold would occur on completion of mining during the December 2016 to March 2017 period. With regard to the recent operational performance, the group delivered a higher than budgeted metallurgical recovery rates at SKO, and witnessed a revision of Cannon’s ore block model based on recent grade control drilling, leading to an improved overall gold recovered estimate.

Moreover, the group delivered a lower operational cost on a per ounce basis and higher net cash generation. In addition, the total cost base drops below A$1,000/oz.

Cannon Gold Production Guidance (Source: Company Reports)

Diversified Base Metal Miner:MLX has a big resource and reserve base in Tin, Copper Nickel and Cobalt. MLX is the only listed Tin producer in the western world of capacity of over 3,500tpa, is a significant Copper Producer of capacity of approximate 35,000tpa and has 100% of one of largest undeveloped Ni-Co-Fe deposits in world.

Moreover, there is development ready growth projects in Tin & Copper and also has a strong cash flow from Tin & Copper. MLX has development ready world class nickel-cobalt project. On the other side, MLX would unlock the value of the company by listing of Westgold Resources Limited.

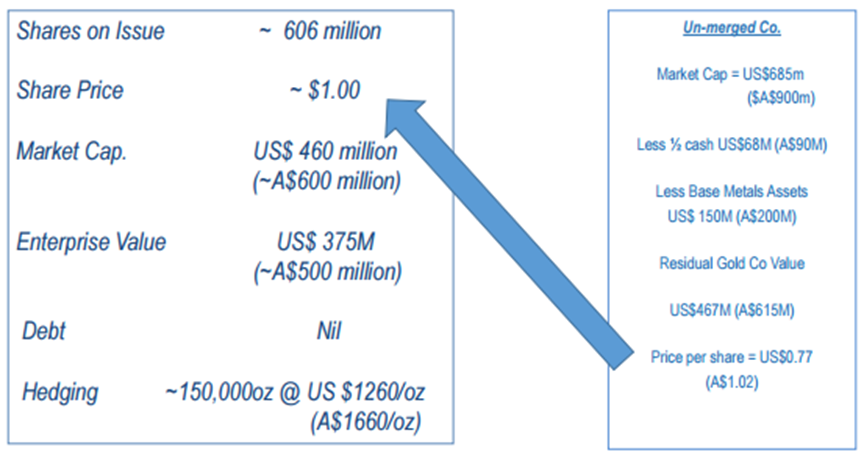

Westgold Resources Corporate Snapshot on Listing (Source: Company Reports)

Takeover of Aditya Birla Minerals Ltd.’s Nifty copper mine:MLX has completed the compulsory acquisition of the remaining ordinary shares in Aditya Birla Minerals Ltd under the compulsory acquisition provisions of the Corporations Act 2001 such that MLX now holds 100% of Aditya Birla.

Demerger update:MLX is looking to demerge its gold division from the remainder of its diversified base metal assets, after the takeover of Aditya Birla Minerals Ltd.’s Nifty copper mine. Over the past few years, MLX has made a number of acquisitions and has built a formidable diversified mining company. The demerger would require shareholders’ and other regulatory approvals, and is subject to accounting and taxation advice.

Demerger highlights (Source: Company Reports)

MLX has stated that a shareholder of the company at the complete separation of the gold unit will own equal interests in shares of both the entities. A shareholder meeting for approval is said to be conducted in late October/ early November 2016.

Interest in companies (Source: Company Reports)

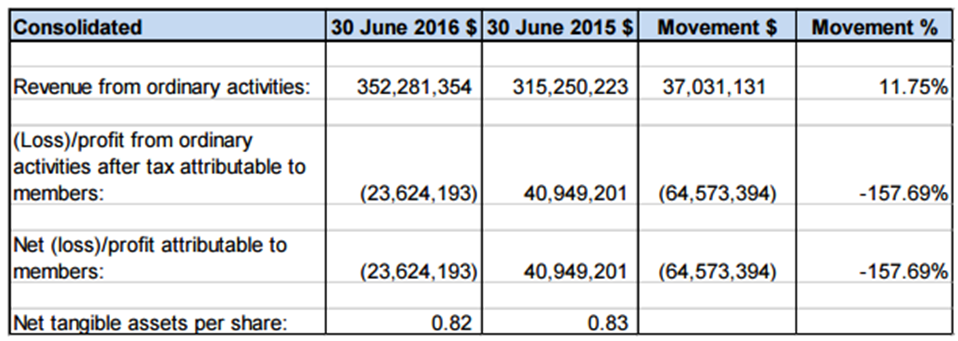

Delivered better revenues despite bottom line pressure: MLX reported a consolidated entity’s net loss after income tax of $23,624,193 in FY 16, which is a decrease of 158% as compared to FY 15. However, the consolidated revenue increased by 11.75% to $352,281,354. But, even the consolidated overall cost of sales reached $339,726,697 in FY16 as compared to $254,907,936 in prior corresponding period. The group’s impairment losses fell to $105,000 in fiscal year of 2016 as compared to $6,217,594 in fiscal year of 2015. However, MLX’s exploration and evaluation expenditure write off reached $26,816,554 during the period as compared to $6,110,660 in prior corresponding period. With regards to the segment’s performance, the Higginsville Gold Operation revenue fell to $151,350,329 in fiscal year of 2016 as compared to $195,812,444 in FY15 on the back of declining production due to lower grades from the Trident underground mine. Consequently, HGO cost of sales increased by $159,570,620 in FY16 from $148,812,444 in FY15 due to better costs of deeper underground mining and post-fill requirements. As per the South Kalgoorlie Operation performance, revenues rose to $72,484,117 in FY16 as compared to $36,963,792 in FY15, driven by better production contributed from the HBJ underground mine which transitioned from a development phase to a production phase. Central Murchison Gold Project contributed revenue of $56,482,885 in fiscal year of 2016 as the production started from the project post plant commissioning in mid-October 2015.

The group’s 50% stake at Tasmanian Tin Operations contributed revenue of $70,682,179 in fiscal year of 2016 against $79,629,155 in FY15 impacted by the tin prices and a reduction in tin output. Meanwhile, the group reported an exploration and evaluation expenditure write off of $26,816,554 in FY16 from $6,110,660 in FY15 on the back of review of each area of interest to find the suitability of ongoing to carry forward costs in relation to those areas of interest.

Financial Performance for FY 16 (Source: Company Reports)

Strengthening balance sheet:MLX has completed the institutional placement to raise $100.6 million and had undertaken the share purchase plan (SPP) to raise up to $15 million, which was oversubscribed. The shares as per SPP were to be allotted on September 08, 2016 and the refunds of oversubscriptions would take place as soon as possible.

Meanwhile, for fiscal year of 2016, the group’s overall equity rose 14% that is $48,641,758 to $394,908,332 during the period as compared to $346,266,574 in prior corresponding period. This difference was mainly on the back of a result of share issues to acquire Aditya Birla shares and to acquire other assets (the Mt Henry and Fortnum Gold Projects) during the period.

Stock Performance:The shares of MLX stock rose over 50.5% in the last six months (as of September 20, 2016) driven by the gold price rally. MLX’s FY16 performance was below expectations affected by the ramp-up of gold production at CMGP that did not meet earlier expectations but the new operations are improving performance and a boost is also expected from the Fortnum Gold Project coupled with MLX’s well-funded position for a demerger.

The gold division’s projection of more than doubling the current annualised production rate over the next few years will add value. Thus, we believe that MLX has still more momentum left as compared to its peers. We give a “Buy” recommendation on the stock at the current price of $1.38

MLX Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...