Company Overview -

Medibank Private Limited is an Australia-based private health insurer and provider of ancillary services. The Company operates through two segments: Health Insurance and Complementary Services. Health Insurance segment offers private health insurance products, including hospital cover and extras cover, as stand-alone products or packaged products that combine the two. Hospital cover provides members with health cover for hospital treatments, whereas extras cover provides health cover for healthcare services, such as dental, optical and physiotherapy. Health Insurance segment also offers health insurance products to overseas visitors and overseas students. Complementary Services segment offers a range of activities, including contracting with government and corporate customers to provide health management services, as well as providing a range of tele health services in Australia and New Zealand. It also distributes insurance products on behalf of other insurers.

.png)

-

Delivered better than prospectus performance: Medibank Private Ltd (ASX: MPL) delivered a better performance in FY15 than the prospectus forecasts, reporting a net profit after tax increase by 12.9% yoy to $292 million during fiscal year of 2015, on the back of improved performance of its Health Insurance business. As a result, the group declared dividends of 5.3 cents per share, representing a full year payout ratio of 70% and better than the Prospectus forecast of 4.9 cents per share. The implied total year dividends is 7.4 cents per share (inclusive of pre-IPO dividend to Commonwealth). Medibank Private intends to achieve a dividend payout ratio of between 70% and 75% of underlying net profit after tax during 2016 financial year. The group’s net investment income reached $93.8 million during the fiscal year of 2015, which is better than the Prospectus forecast but lower than earlier year on the back of lower interest rates and decrease in growth of equity markets in FY15 as compared to FY14. Meanwhile, MPL has a debt-free balance sheet, while Health Insurance capital is over 12.3% of premium revenue as of June 2015, on track with the group’s estimated range of 12% to 14%. Both fiscal year of 2014 and 2015 maintained decent margins as actual claims were lower than provided during year end.

-

Solid health insurance business growth: Medibank Private’s core Health Insurance premium business revenue generated an increase of 5.1% yoy to $5,934.8 million during fiscal year of 2015. On the other hand, the premium revenue growth slowed down on the back of rising membership lapses, cover reductions and changes to sales mix. Medibank Private’s overall policy holders’ growth declined by 60 basis points to 0.9% for FY15, as compared to 1.5%. But, the segment’s operating profit delivered outstanding performance, surging by 33.8% yoy to $329.3 million in FY15, which is well ahead the prospectus estimates. As a result, the segment’s Gross margins also improved to 14.2% in FY15 against 13.5% in FY14, well ahead than the Prospectus forecast of 13.6%. MPL was also able to enhance its Management expense ratio for the segment to 8.6% during FY15, which is much better than the prospectus forecast of 8.7%, and against the FY14 ratio of 9.2%. MPL targets to decrease the management expense ratio to below 8% by fiscal year of 2017. The net operating margin improved by 120 basis points to 5.5%, from 4.4% in fiscal year of 2014 and better than the prospectus forecast of 4.9%, boosted by savings in management expenses and better health benefit claims management. Meanwhile, Medibank has been maintaining competitive margins in the industry as compared to its peers and is seeking to further improve its margins and enhance its operating base. The group intends to continue to focus on health benefit claims management and quality outcomes in order to decrease affordability pressures on members.

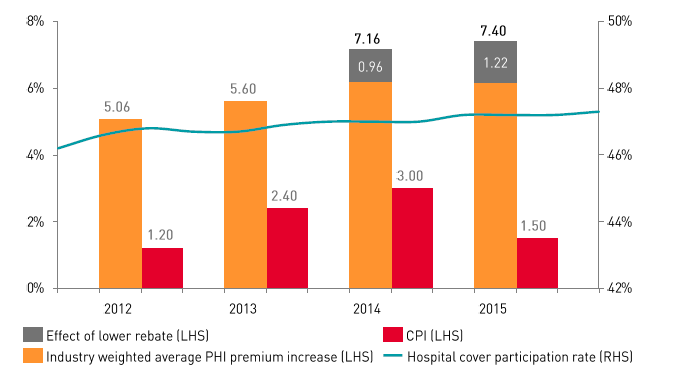

Private health industry premium rise and hospital cover participation rate (Source: Company Reports)

-

Drivers of Health Insurance business despite tough market conditions: The group paid out $5.1 billion in member benefits as of June 2015 and supported its members by paying for over 400,000 acute surgeries, generated >1.2 million hospital admissions and performed over 27 million ancillary services including dental, optical and physiotherapy. MPL spends around 86 cents in every premium dollar they would receive in paying member benefit claims charged to them by its national network of hospital and primary care providers. However, despite challenging economic conditions pressure, MPL managed to cover changes as requested while maintaining its profitability. The group also adopted specific programs to enhance its efficiency and division business. Medibank Private implemented a payment integrity program to dental and remedial massage provider networks with which MPL could track over-servicing as well as recognize improper payments through its data and analytics capabilities. Medibank launched a performance based hospital contracting by focusing on clinical outcomes, patient safety with which the group could link payment to reductions in preventable complications and waste. MPL’s product design and management of claims led to a 2.5% year on year cost growth, which is lower than the industry standards, despite meeting 100% of eligible members’ claims. On the other hand, decrease in Government private health insurance rebate also led to affordability concerns of consumers for their private health insurance policies. Therefore, to offset these pressures, MPL adopted a Health Cost leadership strategy to provide long-term affordable health insurance cover for its members who offers the relevant levels of protection. Despite paying 100% of its eligible claims, the group’s focus on health cost leadership enabled them to acquire those health benefits at competitive rates as compared to its peer group. As a result, Medibank witnessed a lowest increases in health benefit claims which rose over 4.3% as compared to industry growth of 7%.

-

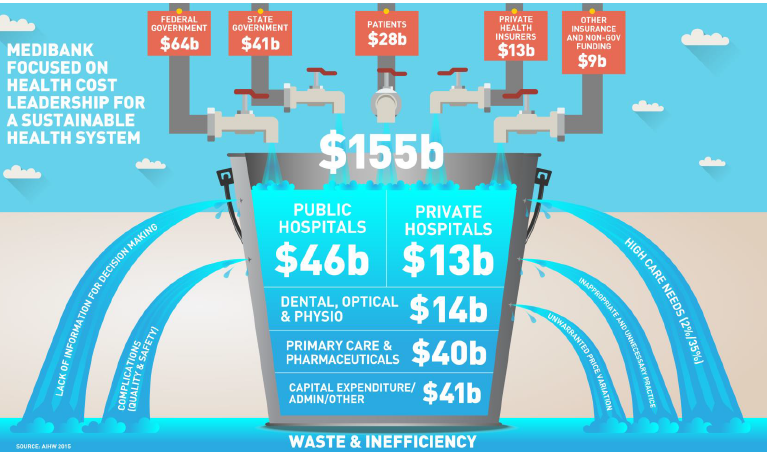

Health Cost leadership strategy focus to offset tough market conditions pressure (Source: Company Reports)

-

Complementary Services business alignments is on track to boost the group’s core business: Medibank is streamlining its Complementary Services business to align the division to boost its core Health Insurance business, and accordingly reported many divestments during the first quarter of this year. As a result, the collective operating result (Health Insurance & Complementary Services) improved by 25% on a year over year basis to $320 million during fiscal year of 2015. Meanwhile, Complementary Services accounts only 10% of the overall group’s revenues, and just 4% of MPL’s operating profit. The division’s PNIC team manages the $5 billion pa of health purchasing and is also responsible for major health contracts within the Complementary Services. PNIC team is also responsible for Nurse Triage telehealth capability, and the ADF Garrison Health contract as well as delivers a strategic contribution to MPL’s PHI business. Complementary services division also has a diversified insurances business which offers a standalone returns while a significant platform to engage and retain health insurance members.

MPL Daily Chart (Source - Thomson Reuters)

MPL Daily Chart (Source - Thomson Reuters)

-

Health Insurance Outlook: The group reported that they continued to witness affordability challenges which led to cover reductions and customer churns, and in turn affected its premium revenue growth during the first quarter of fiscal year of 2016. On the other hand, MPL estimates that these challenges would be offset by ongoing better than expected claims management outcomes, for fiscal year of 2016. Accordingly, MPL expects a premium revenue growth of more than 5.5% during FY16, while reiterated its management expense ratio of 8.3% in FY16 and below 8.0% in fiscal year of 2017. Medibank intends to achieve an operating profit of more than $370 million during FY16.

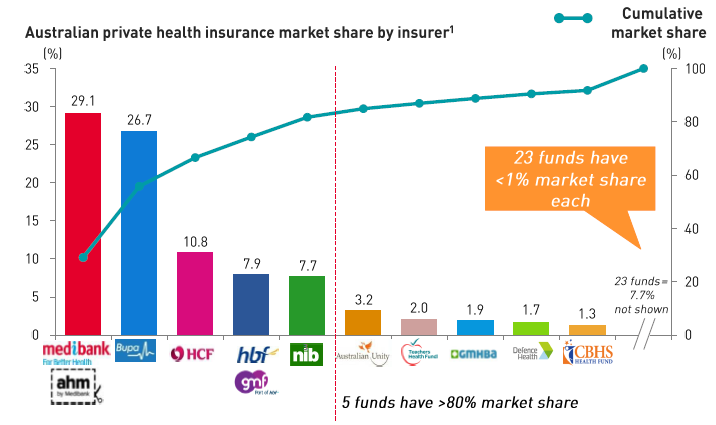

Well positioned to leverage the changing industry dynamics (Source: Company Reports)

-

Stock Performance: The shares of Medibank Private Ltd (ASX: MPL) generated over 6.5% returns since its IPO till date (as of Dec 4 Close), while rallied over 11.2% in the last six months. On the other hand, the stock has been under pressure over the last four weeks, and even fell over 3.4% due to management’s update of a challenging first quarter results. However, investors need to note that the group posted more than estimated fiscal year of 2015 results, and has competitive margins as compared to its peers. Moreover, management also reiterated on its positive fiscal year of 2016 performance, as it is focusing to further enhance its management expense ratio. MPL is trading at decent valuations as compared to its peers and has a P/E of 21.9x. We believe the solid fundamentals of Medibank would drive the stock higher in the coming months, and based on the foregoing, we reiterate our “BUY” recommendation on this 2.3% dividend yield stock at the current stock price of $2.23.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Please wait processing your request...

Please wait processing your request...