Company Overview - Mcmillan Shakespeare Limited is an Australia-based provider of salary packaging, novated leasing, asset and fleet management and insurance services. The Company is engaged in the provision of remuneration, asset management and finance services to public and private organizations in Australia. The Company operates in two segments: Group Remuneration Services and Asset Management. Group Remuneration Services segment provides administrative services in respect of salary packaging and facilitates the settlement of motor vehicle novated leases for customers, but does not provide financing. The Group Remuneration Services segment also provides ancillary services associated with motor vehicle novated lease products. Asset Management segment provides financing and ancillary management services associated with motor vehicles, commercial vehicles and equipment. In addition, the Company’s retail financial services business offerings include finance, warranty and insurance.

Analysis - McMillan Shakespeare (MMS) recently announced for the $115 million acquisition of Presidian Group (catering to the automotive industry by providing finance, warrantee and insurance products) which has been regarded as an important step towards a diversification strategy. MMS has primarily put forth interests to buy 100% of Presidian through a binding agreement. Further, the details of the deal include 40% financed in scrip and the remaining in cash and debt indicative of minimal earnings per share dilution.

Presidian Group Structure (Source – Company Reports)

Presidian is thought to have generated about $75 million as revenue and $14.4 million as earnings before interest, tax, depreciation and amortization given the its annualised performance for the six months to 30 December 2014 reflecting an acquisition multiple of 8 times EBITDA on the enterprise value basis. MMS is already known to have a good exposure to the motor-vehicle industry through motor-vehicle novated leases and other services. This effort will help it expand its consumer finance base for new and used motor vehicles. It will also bring opportunities to pave way for new revenue streams given the fragmentation in the consumer finance industry. Presidian provides finance of the order of about 51% of FY14 revenue, about 40% warranty and 9% of insurance products to a network of 2,500 used car dealers.

NPAT Performance (Source – Company Reports)

Such initiatives along with outstanding half year result backs the performance. Primarily, MMS reported its half year NPAT of $31.1m which is 62% higher than the prior corresponding period (pcp) and 5% higher than 1HFY13. This has been a little lower (~7%) than the consensus expectations in view of the temporary service suspension in Queensland in H1 which amounted to $2m cost to NPAT. However, the market expects this to be compensated for in H2. The free cash flow has been of the order of $35m after CAPEX and tax before fleet increase.

Earnings per Share (Source – Company Reports)

Looking at the results, we note that the improvement comes from the recovery of results from the Group Remuneration Services’ segment following the reversal of the government’s proposed legislative change to fringe benefits tax (FBT) on motor vehicles.

Competitive Strengths and Performance Indices (Source – Company Reports)

Revenue from the ordinary activities has been up by 12%. Lower revenue from novated leasing given temporary contract suspension affected the profits to some extent. The Group Remuneration Services segment has been performing well with improvement in operating margins given the NPAT to be $24.6m indicating 86% growth on pcp and 12% growth on 1HFY13. Core operating contribution (profit before finance, tax and depreciation derived directly from salary packages managed and novated leasing MMS) of 40% has been recorded and the free cash flow amounts to $27.4m.

On the other hand, Asset Management segment reported growth to continue to $353m. The market conditions have been reported to be competitive with pressure on NIM and management fees. Stable performance with regards to the inertia of fleets is noted over previous period. The Company has put efforts in terms of provisioning of about $2.0m against an expected future residual value loss, and hedging facilities for the interest rate risk management. Further, the UK business has been reported to have improved growth while the Company is creating brand reputation in the market. Wholesale funding panel backs the retail sales model. MMS witnessed growth by A$23m for assets under finance. Other developments include funding of A$27m by Maxxia Finance and approval of Lifestyle Lease by HMRC with launch planned for 2015. The UK business has been strong and good market response is coming for the Guaranteed Future Value product. The Company seems to have been busy with many key contract wins and a pipeline of new business. Asset Management reported an NPAT of $6.2m which is 3% lower than pcp.

Dividends per Share (Source – Company Reports)

MMS also reported an interim fully franked dividend of 25 cents per share and diluted EPS of 41.0 cps showing 62% growth on pcp and 4% growth on 1HFY13. The basic EPS has been 41.2 cps with 59% growth on pcp and 3% growth on 1HFY13. This resulted in an annualised return on equity of 27%. From funding standpoint, MMS has the backing of extended Asset Management facility limit up till March 2017 and increase in the UK facility by a further £12m to £37m.

The Company is now focusing on setting a new stage of development, growth and profitability wherein the financial strength and its cash generation capability will help create a diversified and robust business ecosystem. In such a scenario, acquisitions will help foil the core proficiencies. The Company’s IT investment program is also likely to benefit in terms of growth, efficiency and productivity.

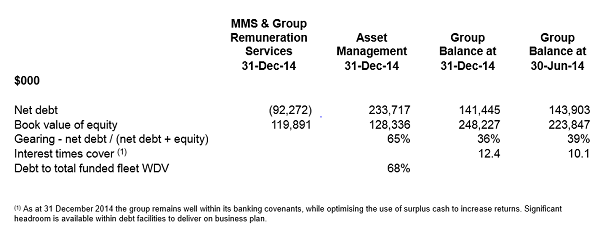

Gearing (Source – Company Reports)

Overall, the Company is known to deliver strong returns on equity consistently. Even with the blow of regulatory changes affecting MMS’ operations in FY14, 25% ROE could still be generated. Nevertheless, regulatory risk now seems to be lower given the overall scenario. One still needs to know that risks related to interest rates, second hand car prices, new car sales, government policies, economic conditions and competition do prevail with regards to Company’s performance. It is to be nevertheless noted that the business has been performing well regardless of turbulent economic conditions. Further, MMS is confident of witnessing organic profitable growth based on new business and cross-selling opportunities, competitive cost of funds, supple financing facilities, and revenue benefits emanating from the Presidian acquisition. UK business can prove to be a long-term growth opportunity and the Company anticipates higher profits in FY15 in view of the developments entailing UK regulatory approval obtained for new product and 2H CY15 earmarked for marketing activity. The recent efforts and achievements by the Company have been reverberated through the price rise of about 25% in 12 months ending 30 April 2015. In fact, the stock has risen to a new 52-week high six times in the last three months which is indicative of an improved growth profile. Changes in substantial holding from key entities also holds the key to rising interests in the Company.

MMS Daily Chart (Source - Thomson Reuters)

Accordingly, we put a BUY recommendation for this stock at the current price of $12.12.

.png)

.png)

.png)

.png)

.png)

Please wait processing your request...

Please wait processing your request...