Kalkine has a fully transformed New Avatar.

Company overview - Mantra Group Limited is engaged in the provision of accommodation and hotel related services, food and beverage operations and central reservations. The Company's segments include Resorts, which operate retreats and resorts in leisure destinations, principally under Management Letting Right (MLR) agreements; CBD, which operates properties in major cities throughout Australia, principally under Lease Right (LR) agreements; Central Revenue and Distribution, which contains the Company's in-house customer management and booking services, through which it earns fees from bookings made through its central reservation system, and Corporate, which includes revenue received under Marketing Services Agreements and from the Renovation and Design department. Its portfolio ranges from luxury retreats and coastal resorts to serviced apartments in CBD and leisure destinations, under its over three brands, including Peppers, Mantra and BreakFree.

.PNG)

MTR Details

Strong first half of 2017 Financial Performance: Mantra Group Ltd (ASX: MTR) had reported 15.1% growth in the underlying Net Profit After Tax (NPAT) of $31.8 million in the first half year results for the period ended December 31, 2016, which is up $4.2 million as compared to H1FY2016. The underlying EBITDAI grew 10.3% to $58.7 million during the period (underlying results are the statutory results excluding transaction costs of $1.7 million incurred in respect of acquisitions). The total revenue grew by 15.9% to $356.2 million during the first half period. The Revenue, Underlying EBITDAI, NPAT and NPATA, all performed ahead of the previous corresponding period (pcp). Further, the business has performed strongly in H1FY2017 due to the strength of Resorts and acquisitions which has offset the weakness in CBD. Moreover, the strong revenue growth is due to the four property acquisitions which were finished in the period (increase of $27.9 million). Organic growth which rose $20.9 million also contributed to the overall growth. On the other hand, the Underlying EBITDAI margin has decreased from 17.3% to 16.5% impacted by ARR decrease in CBD despite solid ongoing Asian inbound trends.

.png)

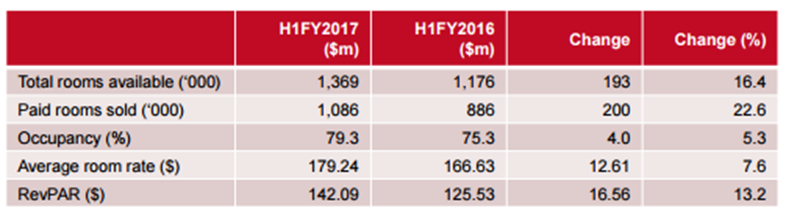

First half of 2017 Financial Performance (Source: Company Reports)

Excellent Growth in the Resorts: MTR has posted 30.1% growth in the Resorts revenue to $163.0 million in the first half year 2017 as compared to the prior corresponding period. The new Resorts properties contributed $27.9 million in the revenue and $4.7 million in EBITDAI during the period. There is an organic growth in Resorts revenue and EBITDAI, of the order of $9.8 million, which is a rise of 7.8% on a year on year (yoy) basis, and $1.7 million, which is an increase of 7.7% on a yoy basis, respectively. Moreover, the total room’s availability enhanced 16.4% on the back of the addition of Mantra Ala Moana from July 2016 to the portfolio. The Occupancy has increased by 5.3% as a result of increased demand from domestic and international travelers. Furthermore, the average room rate has increased by 7.6% as a result of the growing demand, particularly in Queensland destinations. The average room rate had increased in all Resorts regions.

Resort Segment performance in the first half of 2017 (Source: Company Reports)

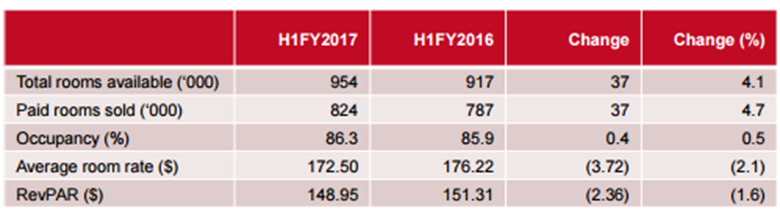

Ongoing weakness in CBD Segment: MTR has posted 3.4% growth in the CBD revenue to $162.8 million in the first half year 2017 as the segment benefitted principally from full year contributions from two CBD properties added around mid and late H1FY2016. Moreover, in the CBD business segment, the total rooms available increased by 4.1%, which primarily came from a full six-months’ contribution from two CBD properties added in H1FY2016 (Peppers Waymouth and Mantra on Mary). The occupancy of the CBD segment has increased by 0.5% following strong conference business and special events in Melbourne and Canberra, in particular. The occupancy at all CBD regions has increased with the exception of Darwin. On the other hand, EBITDAI has decreased by 5.1% principally due to challenging rates in certain CBD locations (Perth, Brisbane and Darwin). This weakness is mainly hurt by Perth and Darwin regions. But the first half of 2016 property acquisitions drove the group’s performance in the subsequent first half after an initial ramp up phase. Average room rate across the segment fell 2.1% or $3.72 to $172.50, impacted by lower rates in Brisbane, Perth and Darwin. Scheduled refurbishment at 2 Bond Street impacted Sydney wherein the rendered rooms were out of service during the four-month period. However, this refurbishment is showing positive results on rate and occupancy since they were finished in October 2016. Meanwhile, excluding Brisbane, Perth and Darwin, RevPAR has increased by $3.10.

CBD Segment performance (Source: Company Reports)

CR&D Segment performance: MTR has posted Central Revenue and Distribution (CR&D) revenue of $28.3 million in the first half year 2017 exceeding the prior corresponding period by $5.2 million. The H1FY2017 EBITDAI of the CR&D segment was $18.8 million, which is an increase on H1FY2016 of $2.0 million (12.1%). The management fees increased and there was an increase in the volumes generated through Mantra Group online booking channels. Further, there was increased fees from management agreements.

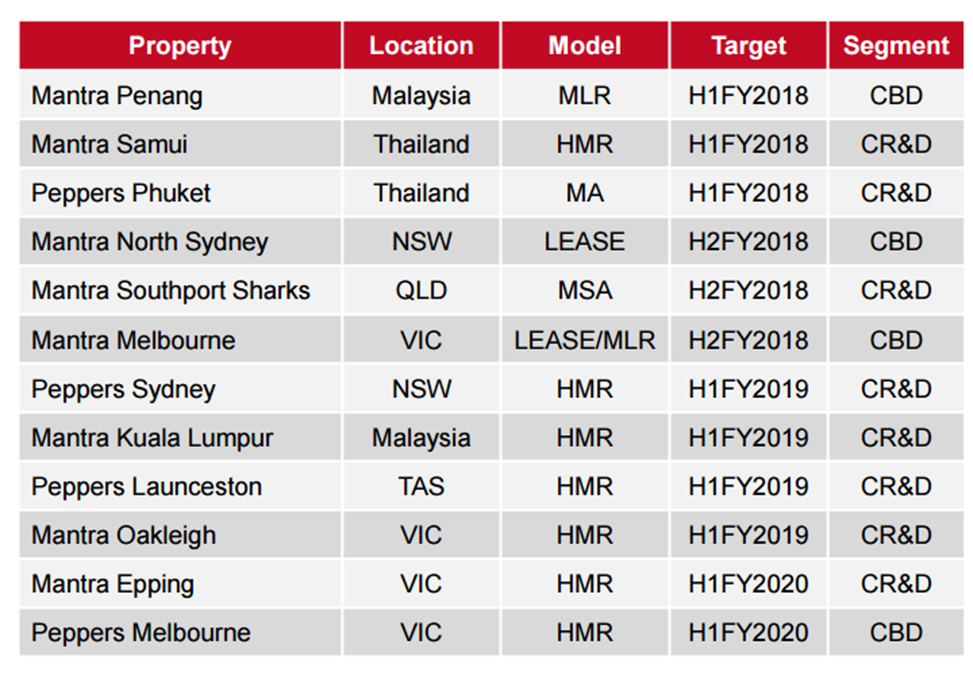

Network Growth: During the six months ended December 31, 2016, MTR has added four new properties to its network, three in the Resorts segment that includes Ala Moana Hotel in Honolulu Hawaii, Mantra Residences @ Southport Central on the Gold Coast, and Mantra - The Observatory at Port Macquarie. The group also added Peppers Kings Square Hotel, Perth (a management agreement property), that has joined MTR’s Central Revenue and Distribution segment. Moreover, the development pipeline is strong for the group with Mantra Club Croc, Airlie Beach and TRIBE West Perth due to open in H2FY2017. Further, the group’s new-build Mantra hotel at Sydney Airport is scheduled to join the Group in July 2017, with Mantra Macarthur Hotel, Canberra and the first two (of three) towers of Brisbane’s luxurious FV by Peppers due to open in August 2017 (subject to customary settlement conditions). Additionally, MTR would continue to be ahead with H2FY2017 set to see ongoing portfolio growth, characterized by further acquisitions in key Australian and international destinations. Furthermore, MTR has already made the announcements regarding the group's operation of new hotels being constructed in Melbourne, Perth, Queenstown, Albury and Wallaroo Shores, and additional new projects would be announced.

Upcoming portfolio pipeline (Source: Company Reports)

Balance Sheet highlights: Mantra group’s cash balance decreased to $56.7 million as compared to $117.1 million as of June 30, 2016. On the other hand, the June’s 2016 cash balance was held for Ala Moana acquisition. Accordingly, management believes that they reached to normal cash levels during the first half and intends to continue to generate strong operating cash inflows from operations. The net cash inflow from operating activities rose $1.1 million or 4.5% from $24.1 million to $25.2 million in the current period. Moreover, Mantra drew down a further $15.0 million of its borrowing facility in order to ensure sufficient funds for acquisitions. As at 31 December 2016, the Group had drawn $141.0 million on the facilities, with $53.2 million available funds. The group paid a fully franked interim dividend of 5 cents per share.

Outlook and Strategy for 2017: MTR has reaffirmed the guidance provided in August 2016 of EBITDAI, NPAT and NPATA, which is expected to be in the range of $101.0 million - $107.0 million, $48.5 million - $52.5 million, and $51.0 million - $55.5 million, respectively. The guidance for FY2017 excludes the impact of any additional conditional or uncontracted properties as at June 30, 2016 and any transaction costs and foreign currency translation costs associated with FY2017 acquisitions. Moreover, in line with its key strategies, MTR continues to assess suitable acquisition opportunities both domestically and abroad. Additionally, the dividend payout ratio for full year is expected to be in the range of 60% to 80% of the Statutory NPAT. In addition, the second half of the financial year had a solid start with early H2FY2017 showing great momentum. Lately, MTR has also appointed a new CFO.

Stock Performance: MTR stock fell over 12.1% in the last three months (as of February 24, 2017), as the CBD Segment EBITDA declined despite top line increase. Soft market conditions at Brisbane, Perth and Darwin led to this weak performance. On the other hand, the group reported a solid overall performance and is well positioned to benefit from the inbound tourism on a long-term perspective. Despite the rising competition, Mantra has a well-diversified portfolio and still prominent in some major locations. The stock has a decent dividend yield. We give a “Buy” recommendation on the stock at the current price of – $ 2.72

.png)

MTR Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Please wait processing your request...

Please wait processing your request...