Company Overview - Mantra Group Limited is an Australia-based company engaged in the provision of accommodation and hotel related services, food and beverage operations and central reservations. The Company is a hotel and resort marketer and operator. The Company operates through segments, including CBD, Resorts, and Central Revenues and Distribution (CR&D). The Company operates properties under three brands: Peppers, Mantra and BreakFree. The Company's portfolio consists of approximately 119 properties and over 13,000 rooms across Australia, New Zealand and Indonesia. The Company, through its portfolio, operates a network of accommodation properties in Australia. The Company offers services, including management of guest relation and reception areas; restaurants and bars; conference and function centers; pool and entertainment facilities, and offices. The properties of the Company include luxury retreats, coastal resorts, service apartment and hotels.

MTR Details

World's first Pokemon Go-friendly hotels: Mantra Group Ltd (ASX: MTR) has launched the world’s first Pokemon Go-friendly hotels in Sydney and Melbourne to encourage fans or the tourists. Pokemon Go is a game based on augmented reality where players use their smartphone camera to walk around the street finding and catching Pokemon, which is launched recently and the game already gained several daily active users as compared to Twitter. According to Similarweb, one in five Australian Android users have the game installed on their device. The group is launching ‘Pokestop By Our Bar’ with free Pokemon Go Lures to leverage the ongoing demand around the app. The introduction of the Pokemon Go is part of the strategy to attract more tourists.

Delivering portfolio growth above expectation: Currently, MTR has more than 125 properties and greater than 20,500 rooms under management across Australia, New Zealand, Bali, Indonesia and Hawaii, which has made the company number one Australia based hotel & resort operator. MTR has launched Pepper Docklands in Melbourne CBD and opened Settle Ala Moana Hotel, Hawaii with 1,176 rooms in July 2016. On the other side, Mantra Groupwould continue to assess suitable acquisition opportunities both domestically and abroad. During the first half of 2016, MTR has finished nine property acquisitions which enhanced the revenue by $32.2million whereas the organic growth witnessed the revenue rise of $22.6 million. MTR is growing through acquisition of properties as this seems to be cost-effective than building the properties. MTR had decided to raise the funds for the acquisition through an equity raising. Additionally, MTR has more than A$7 billion assets under management consisting of large hotel leasing portfolio and significant bargaining power.

.png)

Comparison between Building and Buying of Hotels (Source: Company Reports)

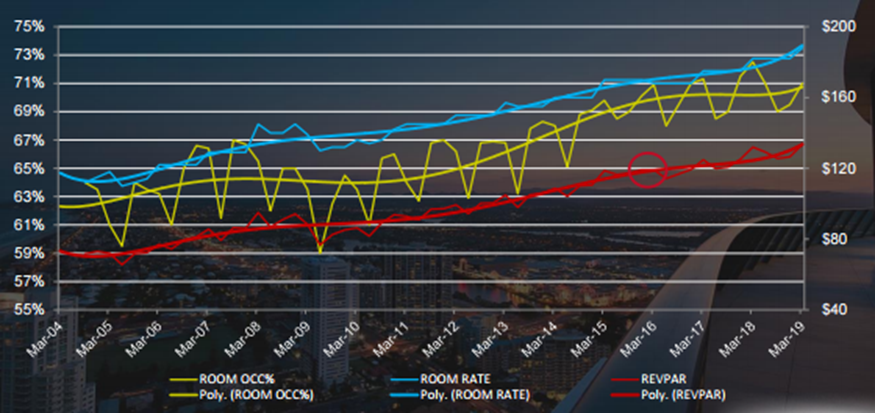

Raising funds for Ala Moana acquisition: MTR had resorted to Share Purchase Plan (SPP) at $3.84 for which the new shares were allotted on 15th June, 2016. Through the equity placement, the group raised over $107 million via the issue of approximately 27 million shares at a price of $3.95 per share. The placement price offered a 1.5% discount to the group’s share price as of 17th May 2016 close price. The group intends to use these proceeds for the acquisition of ALM Management Services. ALM operates the Ala Moana Hotel in Honolulu, Hawaii (Ala Moana) and the related manager's lot real estate at Ala Moana. Mantra group is acquiring Ala Moana for US$52.5 million without the transaction costs. This acquisition by Mantra is on track with its strategy as Ala Moana has a major property in Honolulu which offers further scope to expand into new and attractive offshore market. Mantra reported that the Ala Moana Acquisition and the recent Placement would be accretive to Underlying EPS (excluding transaction costs) during fiscal year of 2017. On the other side, the group has already recognized scope to further enhance the operational performance of Ala Moana (similar to initiatives undertaken by Mantra for their earlier acquisitions in 2015). With the acquisition integration, MTR expects to enhance occupancy from its present level of 75% as well as increase RevPAR. The group intends to generate cost savings in underperforming areas of the business.

.png)

Ala Moana Hotel’s Detail (Source: Company Reports)

Upgraded guidance: MTR had upgraded their financial forecast for FY 16 during February 2016 and recently reaffirmed this guidance, indicating the group’s confidence despite the ongoing tough market conditions. According to the upgraded forecast, the expected EBITDAI, NPAT and NPATA for FY16 will be in between the range of $88.5 million - $90.5 million, $41.5 million - $43 million, and $44.2 million - $45.7 million respectively.

The estimation is based on inclusive of new properties to 18th February 2016 while excludes the impact of any further conditional or uncontracted properties as at 18th February 2016 as well as any transaction costs related with FY2016 acquisitions. Meanwhile, for the first half of 2016, the group’s total revenue increased by 21.7% to $307.4 million from $252.6 million in the prior corresponding period. EBITDAI rose by $11.0 million or 26.1% to $53.2 million during the period as compared to $42.2 million in corresponding period of last year. Consequently, MTR’s EBITDAI margin rose from 16.7% to 17.3% for the first half of 2016, primarily driven by increased rate and occupancy in Resorts segment.

.png)

Financials (Source: Company Reports)

Segment performance: MTR’s CBD revenue grew by 15.4% to $157.4 million in the first half of 2016 in which the new CBD properties contributed $6.8 million in revenue. The new CBD properties contribution to the first half EBITDAI was marginal on the back of start-up costs and timing of acquisitions. The organic growth increased the CBD revenue of $14.2 million. Moreover, MTR’s Resorts revenue grew 31.8% to $125.3 million as compared to prior corresponding period (pcp) and this had significantly increased the overall revenue of the group. The new Resorts properties had contributed $25.4 million in revenue and $4.7 million in EBITDAI while the organic growth enhanced the Resorts revenue and EBITDAI by $4.8 million and $2.0 million respectively. Additionally, Central Revenue and Distribution (CR&D) segment increase in revenue is on the back of higher booking volumes via central facilitated channels and increased management fees from new properties under management. The tight cost control in the corporate segment resulted in savings of $0.7 million as compared to the pcp.

.png)

Segment Performance (Source: Company Reports)

Better than estimated Tourism opportunity: The tourism sector is booming in Australia and it has been earlier projected that 1.4 billion international tourists’ arrivals are expected by 2020 and 1.8 billion arrivals expected by 2030. As per the Tourism Research Australia’s (TRA) Tourism Forecasts 2016, domestic tourism is forecast to improve significantly in the next few years with visitor nights expected to increase 4.5 per cent in 2015–16 and to average 3.1 per cent over the ten years to 2024–25, owing to improving economic growth, lower interest rates, lower fuel prices and the lower Australian dollar. The inbound tourism market is forecast to continue leading growth (9.3 per cent in 2015–16 and an average 5.6 per cent over the ten years to 2024–25). Asian markets are expected to continue driving growth in the next few years led by China (up 18.5 per cent in 2016–17 and 13.3 per cent in 2017–18) and India (up 9.4 per cent and 9.7 per cent, respectively). As a result of the demand, there could be increase in the room rates which would consequently enhance the group’s performance. MTR is expecting strong Chinese tourism trends to continue. China’s outbound tourists have been said to rise to 200 million by 2020 as compared to 83 million in 2012.

Hotel Outlook for Australia (Source: Company Reports)

Stock Performance: The shares of Mantra Group fell 22.01% in the last six months (as of July 22, 2016) due to potential impact on the group’s performance on the back of effect from Brexit, Chinese economic situation hitting inbound Australia’s tourism and rising competition. Moreover, the growing penetration of the group’s competitors like Airbnb is also a major threat to the group’s performance. On the other hand, MTR is positioning itself to withstand this pressure, as well as expanding portfolio by making strategic acquisitions. Recently MTR acquired Ala Moana, but the fiscal year of 2016 guidance excludes the impact as the acquisition is forecasted to settle by the end of July 2016. The group is making efforts to enhance its balance sheet flexibility and accordingly announced the placement for additional capacity to deliver the proceeds for potential pipeline of opportunities at domestic as well as international level. We believe investor’s need to leverage the correction in the stock as an entry opportunity due to recovering demand from China, growth efforts by MTR and easing Brexit fears. The stock recovered over 14.1% in the last five days alone (as of July 22, 2016) and we believe the stock has more potential in the coming months. Based on the foregoing, we give a “Buy” recommendation on the stock at the current price of $3.75

MTR Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...