Kalkine has a fully transformed New Avatar.

I. Sector Landscape and Outlook

Why managed funds industry? Managed Funds industry has low capex businesses, and the top line driver of the industry is funds under management (FUM) – as it is the base for realising fees. Fees, being the main revenue source of the businesses, are mainly segregated into parts: management & performance fees. Performance fee side of the revenues are largely dependent on the underlying performance of the funds, whereas management fees are dependent on the funds held by products of the business (FUM). Let’s quickly glace through the industry fundamentals.

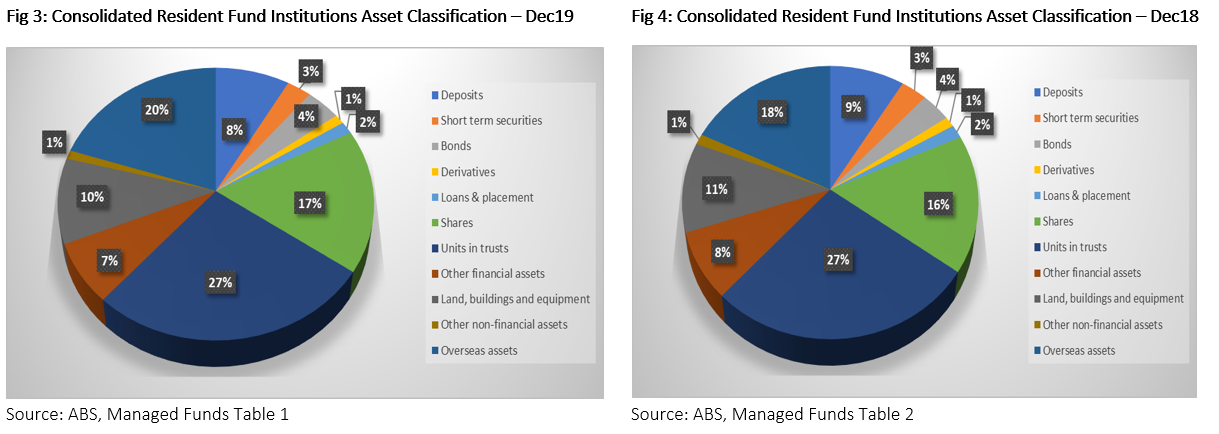

Managed funds industry is underpinned by solid fundamentals. In Australia, the managed funds/asset management/fund management industry has a substantial size. According to the Australian Bureau of Statistics (ABS), the industry had $3.9 trillion of asset under management at the end of last year (i.e. 31 December 2019). Australia boasts a solid regulatory environment for the managed funds industry, which is regulated by the Australian Securities & Investment Commission (ASIC).

Since 1992, the Superannuation Guarantee (Administration) Act 1992 makes it necessary for the employers to make superannuation payments to the funds. Presently, the super guarantee rate is 9.5% of the income, which is set to reach 12% by 2025 over tranches. Australian Superannuation assets are further categorised into industry funds, retail funds, public sector funds, Self-Managed Superannuation Funds (SMSFs), and corporate funds and other.

As on 31 December 2019, the resident managed fund institutions held $3.13 trillion of the managed fund industry, and other resident investors held $670.6 billion. Meanwhile, direct overseas investors held $136.7 billion.

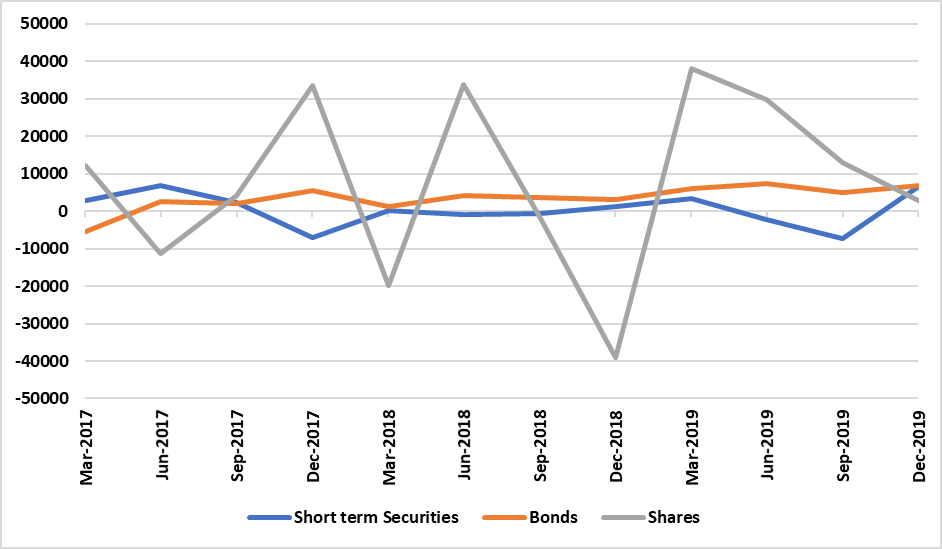

In figure 2, the data shows the segregation of assets as on 31 December 2019 based on asset classes, which were held by resident fund institutions. Total assets managed by resident managed fund institutions were $3.13 trillion, of which majority assets were invested in unit trusts (~27%).

Around 20% of the total assets were allocated to overseas assets, ~17% of the funds were invested in shares, ~10% funds were invested in land, buildings and equipment, and ~8% of the funds were in deposits.

Over the past year, the movements within the asset classes (figure 2 and 3) were led by overseas assets which constituted ~20% of the total funds held by resident managed fund institutions from around 18% in the in December 2018. Likewise, allocations to shares increased by ~1% to around 17% in December 2019. And, there was 1% movement in other financial assets, which constituted 7% as against 8% in December 2018.

Over the year to 2019, the total consolidated assets held by Resident Fund Institutions increased by $384.48 billion to $3.13 trillion from $2.75 trillion at the end of 2018. Of this $384.48 billion, the largest increase was $129.77 billion in overseas assets, followed by $98.04 billion increase in units in trusts, $83.9 billion increase in shares, $25.26 billion increase in bonds, and $23.75 billion increase in land, buildings and equipment. Meanwhile, there was a decrease of $2 billion in other non-financial assets.

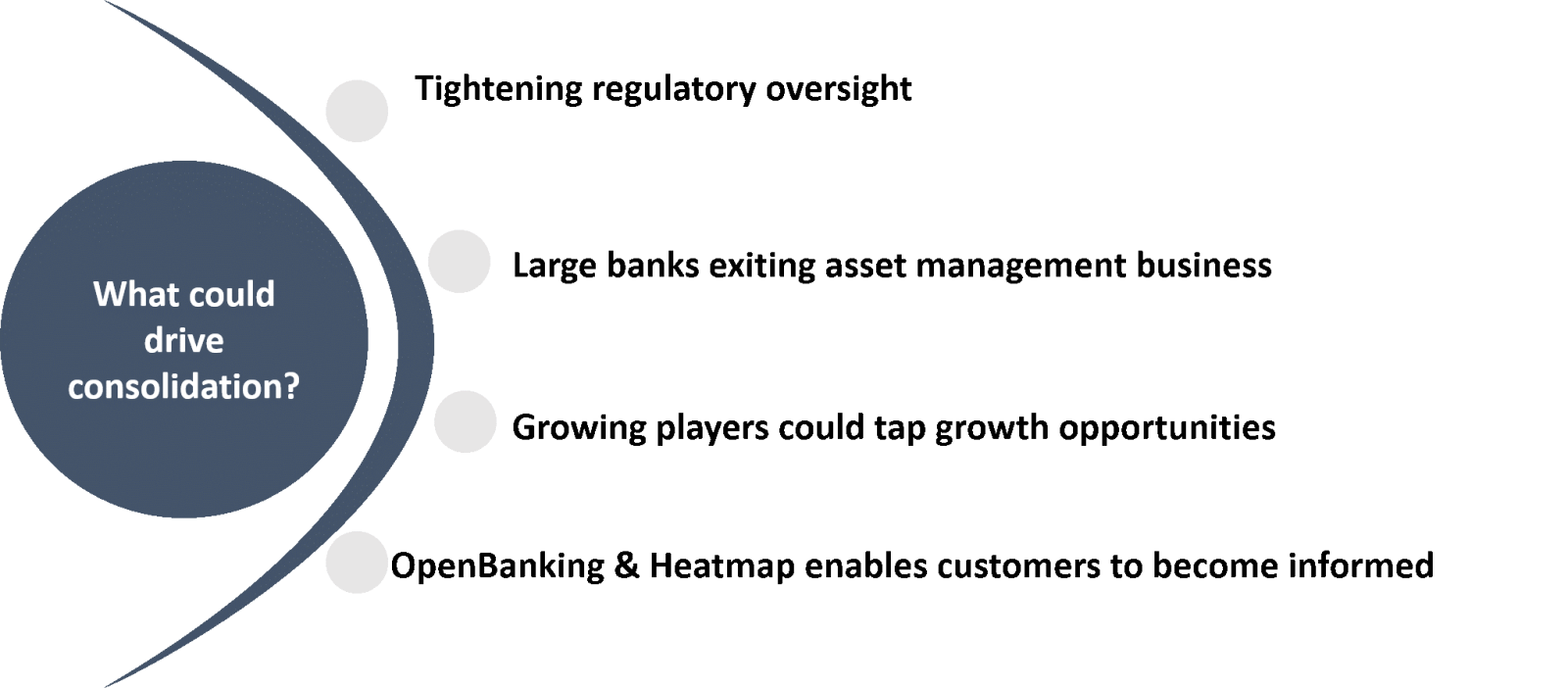

Figure 5: Quarterly Change in Selected Asset Classes (in millions)

Source: ABS, Managed Funds Table 1

At the end of last year, the consolidated total managed fund assets in shares were $533.6 billion, up from $449.71 billion in December 2018, showing an increase of around $83.9 billion an 18% jump. Likewise, the assets in bonds were at around $122.7 billion from $97.43 billion at the end of 2018. Between 2018 and 2019, there has been an increase of $197 million in short term securities, which stood at $85.81 billion at the end of last year from $85.62 billion at the end of 2018. With the understanding of the fundamentals, lets now explore the industry landscape.

Exchange Traded Products have been on the rise. Australian capital markets have Exchange Traded Products, which includes Exchange Traded Funds, Exchange Traded Managed Funds and Exchange Traded Structured Products. ETPs have provided a liquid investment option at a low-cost, and the market for these products has increased over the past considerably. At the end of February, on the ASX, there were 211 exchange traded products, which excludes Listed Investment Companies.

In December last year, the ASIC lifted the ban on actively managed ETFs, which was imposed in July last year. ASIC needed more clarity on internal market making and daily portfolio holdings disclosures for active ETFs. In the December judgement, the regulator lifted the ban on active ETFs, directed companies to ensure a set of guidelines and it continues to monitor the situation.

Increasing expectations could spark consolidation. Since APRA Heatmap was released last year, the expectations demanded - from the underperforming money managers - is likely to increase, and the regulator has intentions to up the standards of responsibility and accountability. APRA Heatmap had highlighted the divergences in the fee charged by companies offering MySuper accounts, especially with the ones having lacklustre performance and relatively expensive service as measured by the fee charged.

Figure 6: Evolving Industry Landscape

Since underperforming funds are at the risks of large outflows towards high performing funds, the APRA Heatmap could be a game changer in the $3.03 trillion (as on 31 December 2019) superannuation industry. At the same time, companies with competitive products have opportunities to improve inflows – through fund performance and attractive fees.

Except for performances of the super funds, the APRA Heatmap also discloses fees charged by the service providers. This could allow astute customers to switch funds that have more reasonable service fees. Evolving conditions could push companies out of business or for a merger, especially the ones having lacklustre performance and expensive services.

Open Banking & Heatmap confluence could flip the industry. Consistent with the potential disruption that could be faced by banking companies in the country, the ‘Open Super’ may lead to a number of possibilities, including a number of super providers shutting shops, an increase in M&A (consolidation). Moreover, a potentially widespread disruption in the industry awaits.

And, the industry has room for consolidation. Since the Royal Commission into Financial Services, the large players have been divesting investment management businesses. Commonwealth Bank had completed the divestment of the Colonial First State Global Asset Management, and the bank is committed to divest Colonial First State and aligned advice verticals. National Australia Bank is pursuing divestments of its wealth business, which includes advice, platform & superannuation and asset management. IOOF Holdings has acquired wealth and investment business from ANZ.

Fintech & ESG provide opportunities. Since the largest asset manager – Blackrock raised voice for sustainable investments, the asset management industry is likely to take a leap in launching products dedicated to ESG practices. Increasingly, the investor community is embracing responsible investing. For instance - Norway Government Pension Fund Global, which is largest sovereign wealth fund had received approval to initiate fossil fuel divestment from its portfolio, and the fund has the mandate to invest in unlisted renewable projects infrastructure.

Meanwhile, fintech in the investment management industry is likely to deliver efficiency gains as well as customer value. Regtech companies could enable the investment management businesses for efficient regulatory reporting in the wake of increasing regulatory scrutiny and costs. At the same time, increasingly innovative enterprise management systems are likely to deliver cost-effective solutions.

Regulatory developments have been largely muted, but the Royal Commission’s second order impacts are visible. Over the last year, there have been two substantial regulatory updates, and both developments have been discussed above. These developments include the APRA decision to unban actively managed ETFs and the launch of APRA Heatmap for super funds. Since the Royal Commission, the prospects of regulatory oversight in the fund industry have increased, and there has been significant flight towards industry superannuation funds. Additionally, fund management companies have witnessed a downward pressure on fee charges, owing to competition and regulatory tightening, and it is likely that more legislative reforms would come into effect.

II. Investment Theme and Stocks under Discussion (CGF, JHG, NGI, PNI, PDL)

After understanding the sector, let’s take a detailed look at five asset managers in terms of their outlook and performance. To gauge the potential of the stocks, we have followed the market multiple approach and used ‘Price/Earnings’ multiple.The peer group for each stock has been shortlisted based on their respective market capitalisation.

Fig 7: Relative performance of the stocks under discussion in last 1 year (Indexed to 100) .png)

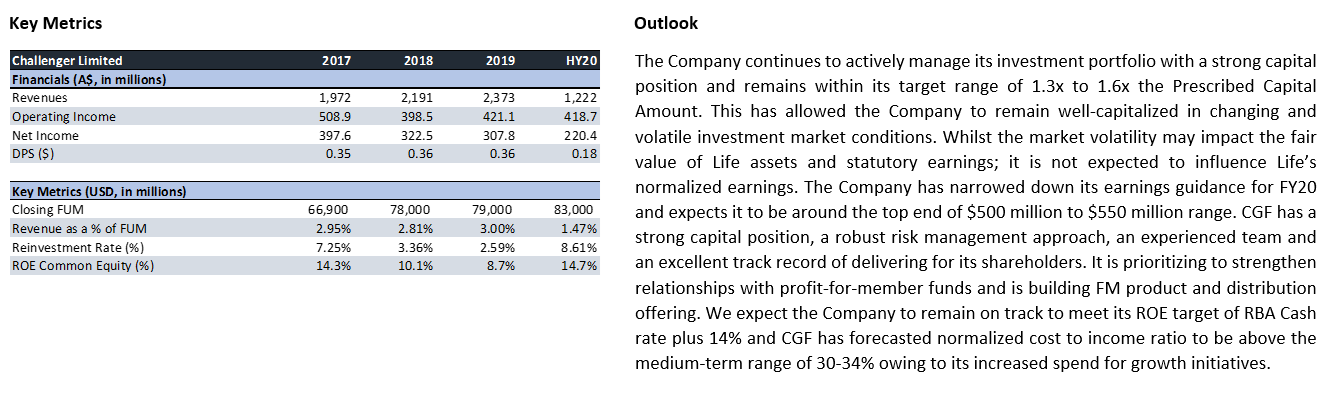

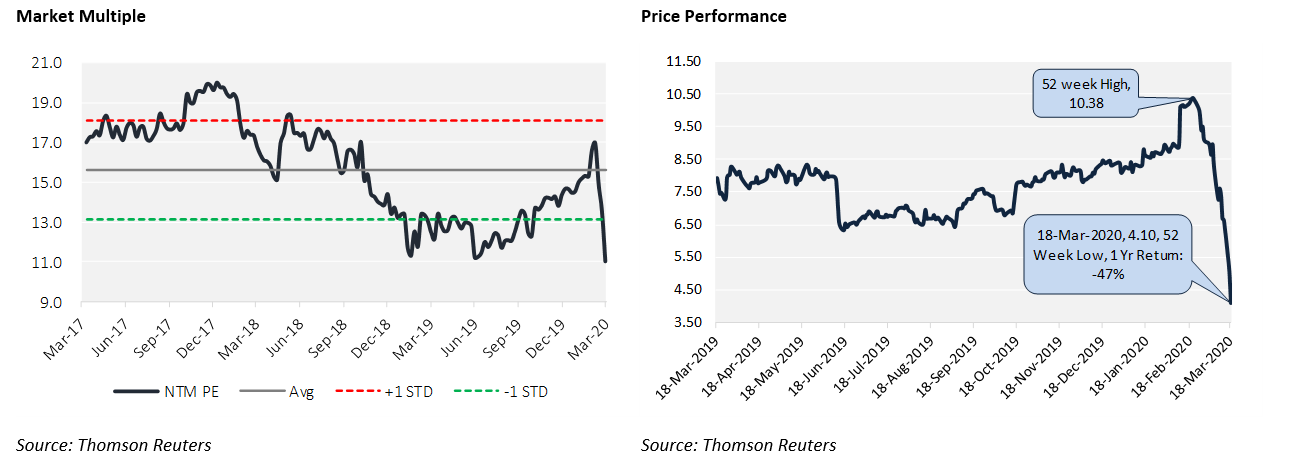

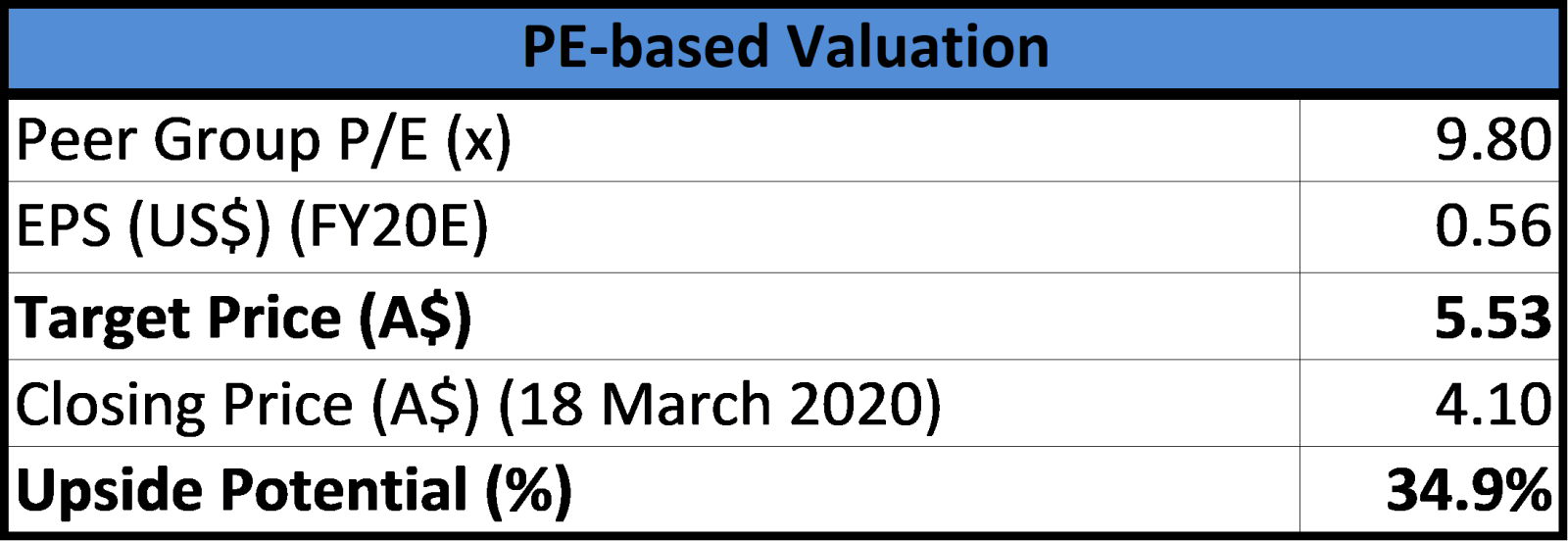

1. ASX: CGF (CHALLENGER LIMITED)

(Recommendation: Buy, Potential Upside: 35%)

Challenger Limited is an investment manager primarily focused on annuity and retirement advisory.

Valuation

Our valuation model suggests that stock has a potential upside of ~35% on 18th March 2020 closing price, based on FY20E Peer Group Average Price-to-Earnings multiple of 9.8x. Peer companies taken for relative valuation are AMP Ltd, AUB Group Ltd, Computershare Ltd, iSelect Ltd, Medibank Private Ltd, and NIB Holdings Ltd.

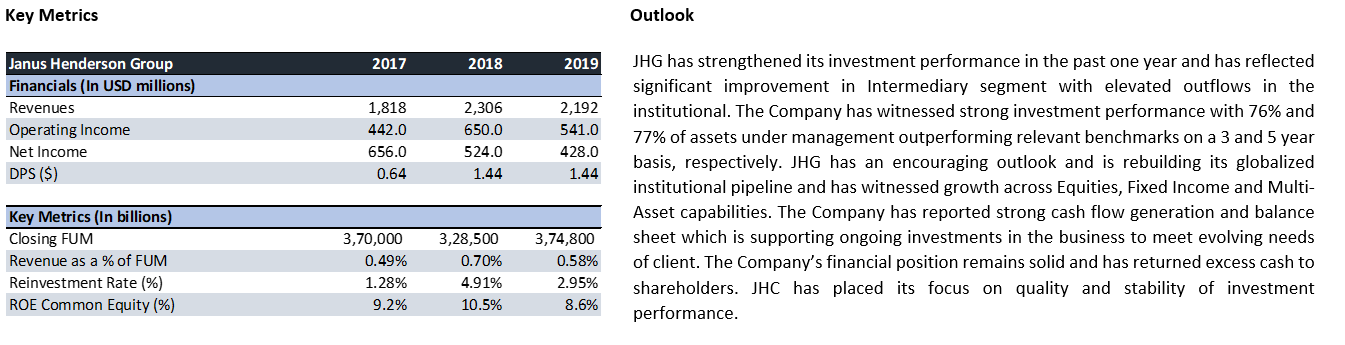

2. ASX: JHG (JANUS HENDERSON GROUP PLC)

(Recommendation: Buy, Potential Upside: 17%)

JHG is a global asset manager and manages funds across asset class such as equity, fixed income and money market for retail and institutional clients.

Valuation

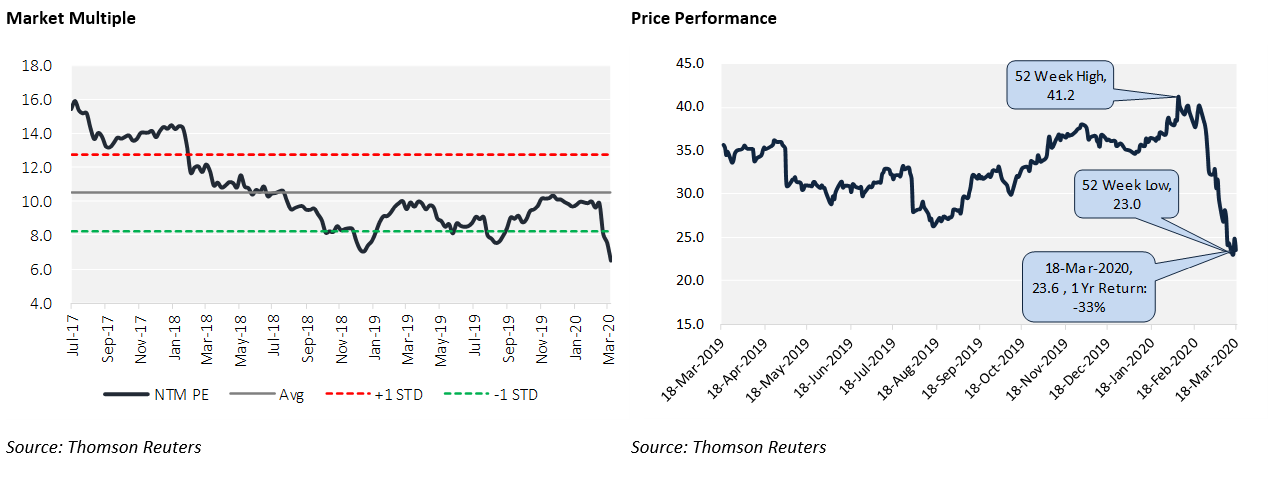

Our valuation models suggest that stock has a potential upside of ~17% on 18th March 2020 closing price, based on FY20E Peer Group Average Price-to-Earnings multiple of 6.30x. Peer companies taken for relative valuation are Invesco, Franklin Resources, and Eaton Vance.

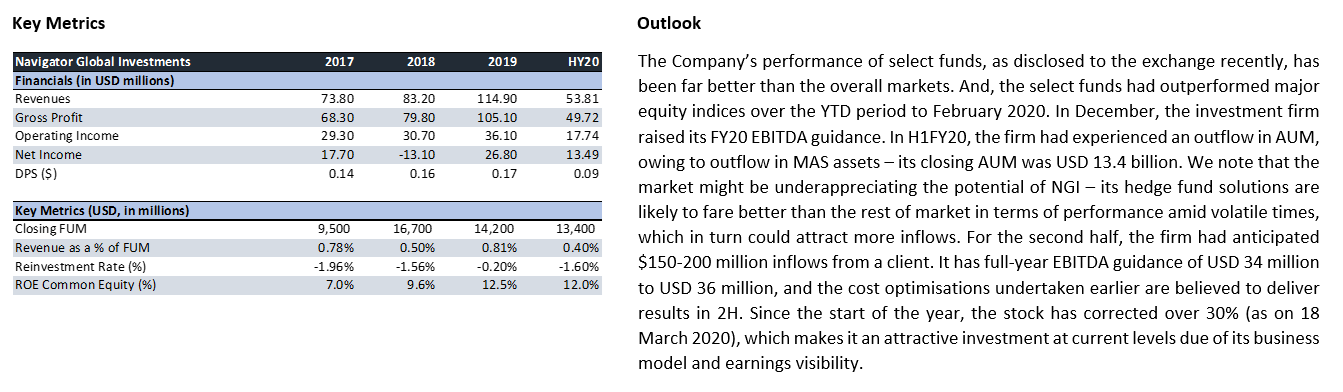

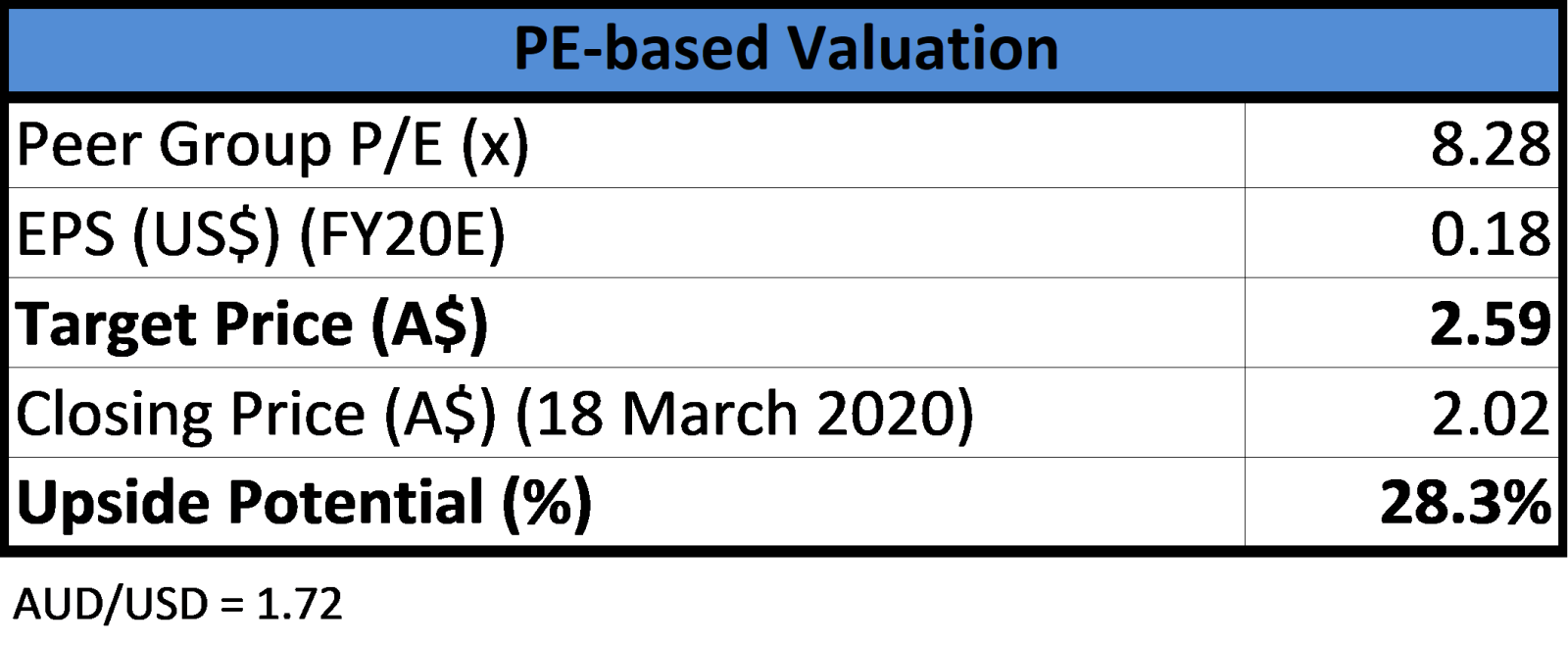

3. ASX: NGI (NAVIGATOR GLOBAL INVESTMENTS LIMITED)

(Recommendation: Buy, Potential Upside: 28%)

NGI is an alternative asset manager which manages hedge funds for global clients.

Valuation

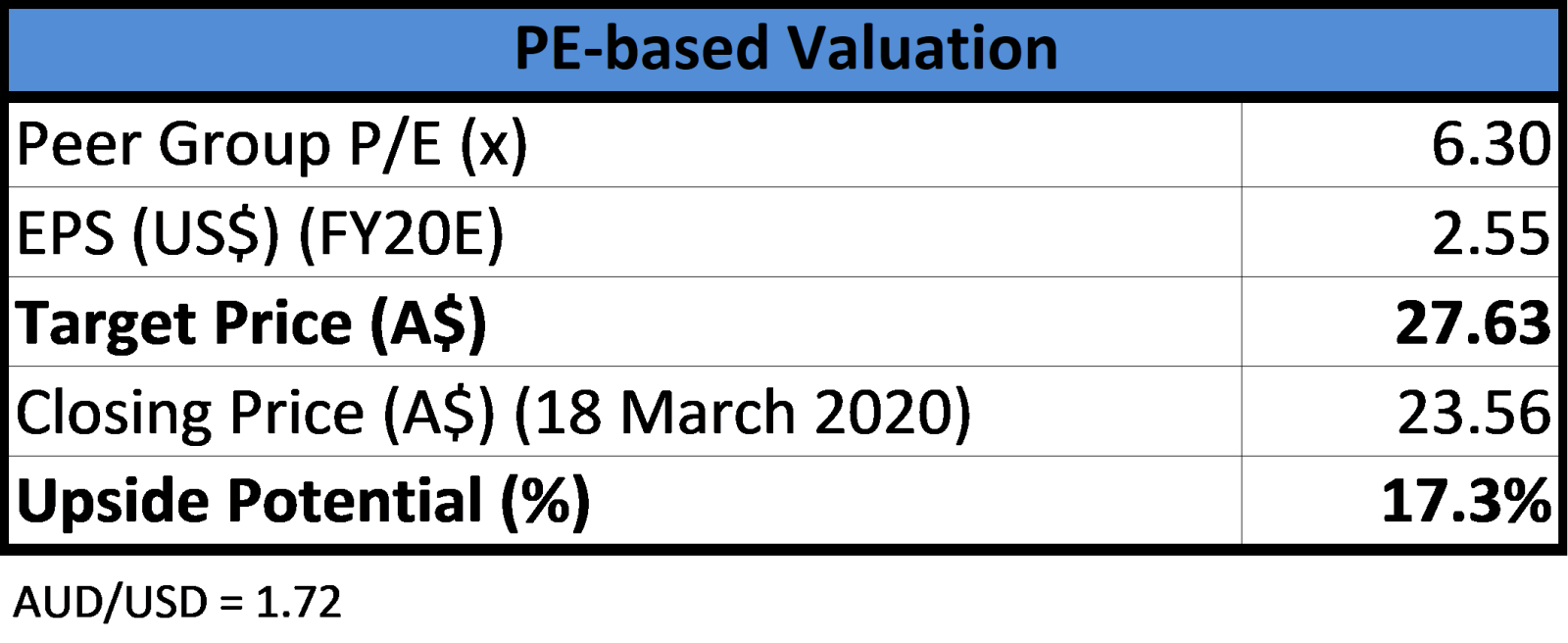

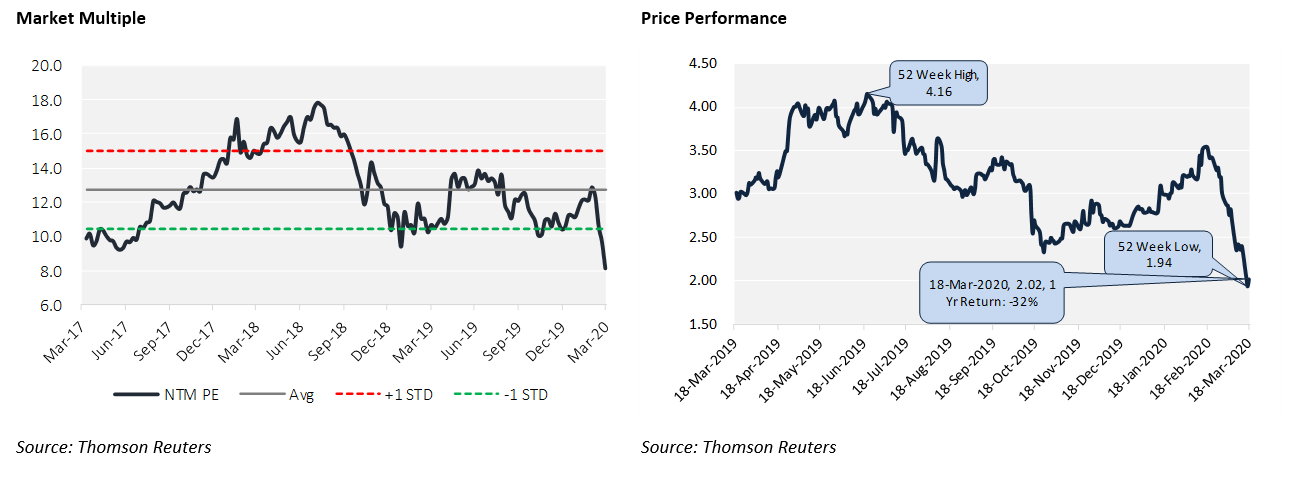

Our valuation models suggest that stock has a potential upside of ~28% on 18th March 2020 closing price, based on FY20E Peer Group Average Price-to-Earnings multiple of 8.28x. Peer companies taken for relative valuation are Pendal Group Ltd, EQT Holdings Ltd, and Pinnacle Investment Management Group Ltd.

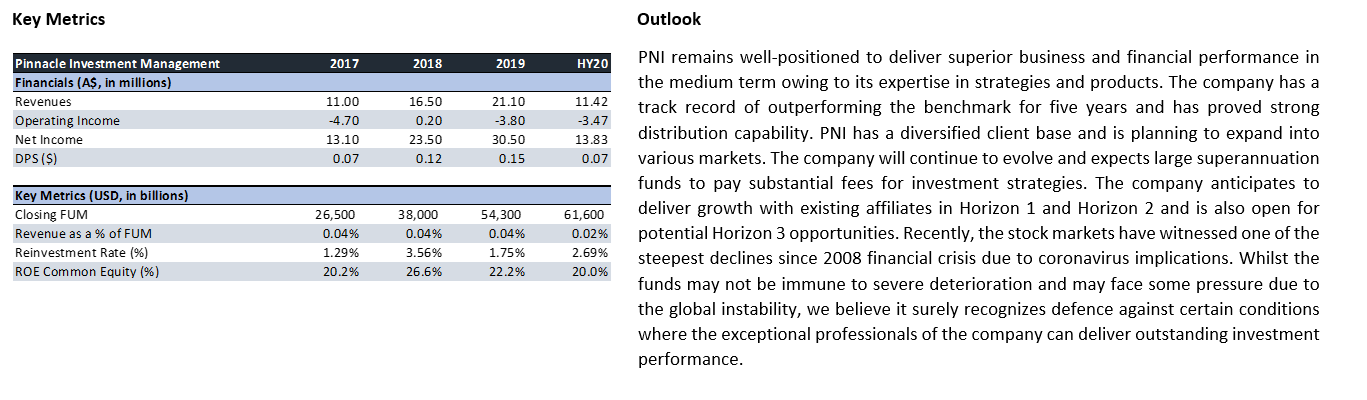

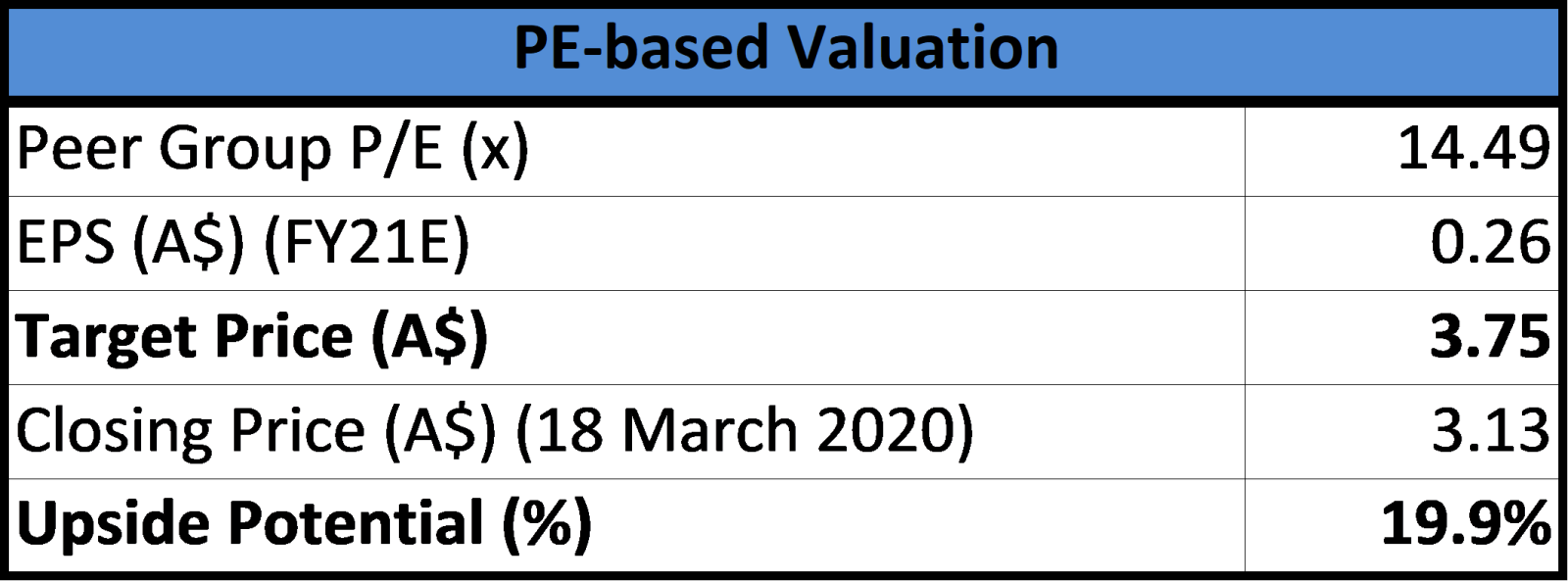

4. ASX: PNI (PINNACLE INVESTMENT MANAGEMENT GROUP LIMITED)

(Recommendation: Buy, Potential Upside: 20%)

Pinnacle Investment Management holds interests in several specialist investment managers, providing superior distribution capabilities and infrastructure to deliver superior outcomes.

Valuation

Our valuation models suggest that stock has a potential upside of ~20% on 18th March 2020 closing price, based on FY20E Peer Group Average Price-to-Earnings multiple of 14.49x. Peer companies taken for relative valuation are Netwealth Group Ltd, Centuria Capital Group, AUB Group Ltd, and Perpetual Ltd.

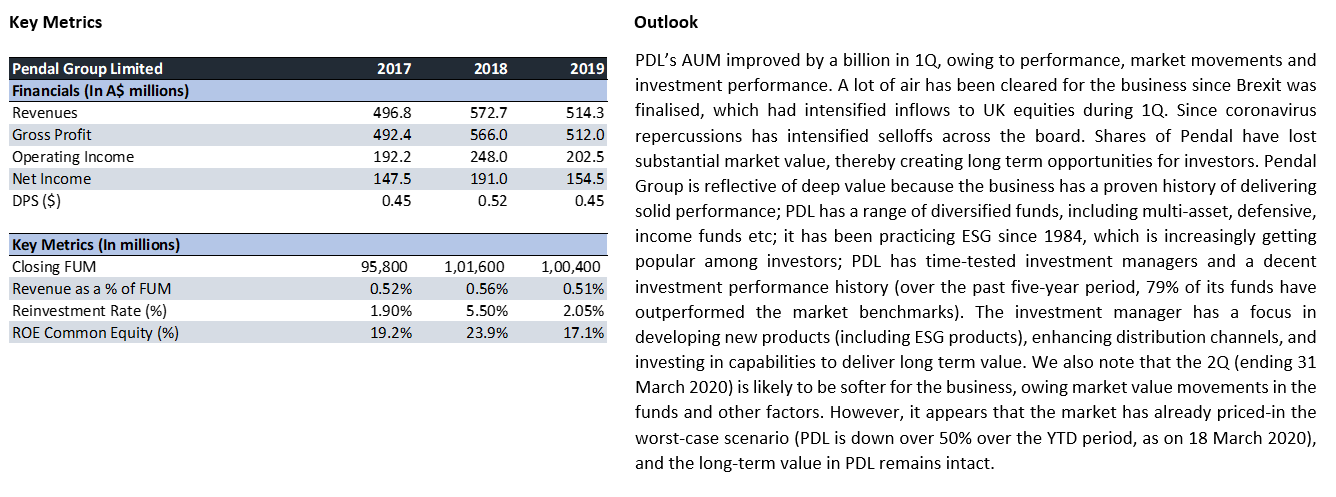

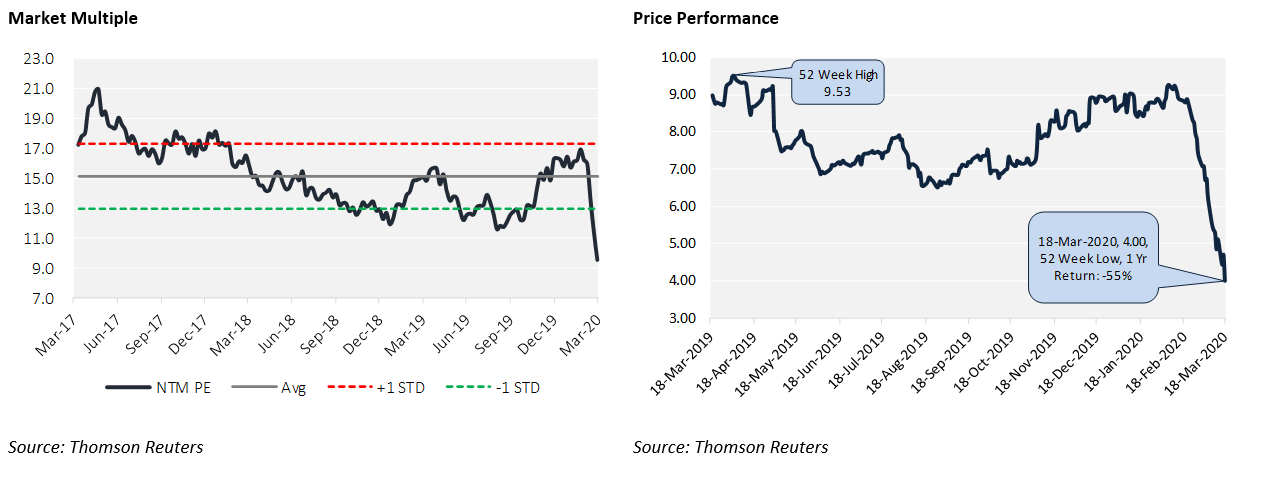

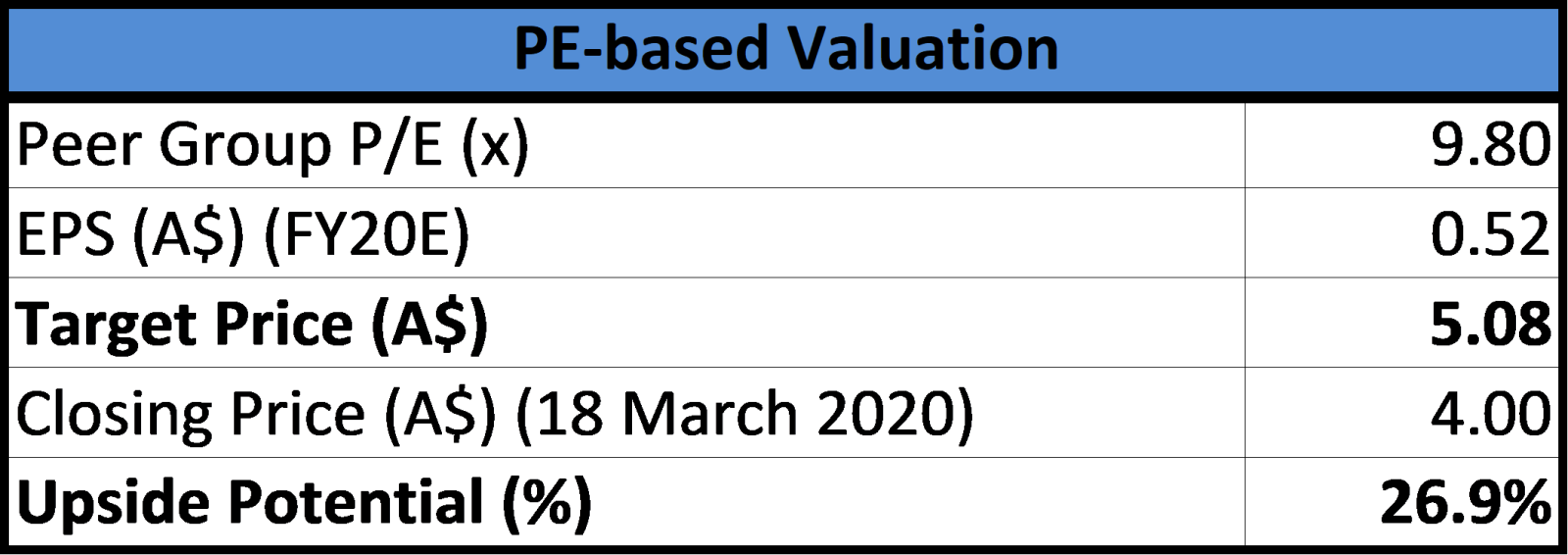

5. ASX: PDL (PENDAL GROUP LIMITED)

(Recommendation: Buy, Potential Upside: 27%)

PDL is one of the country top asset managers with diversified product base and demonstrated history of outperformance.

Valuation

Our valuation models suggest that stock has a potential upside of ~27% on 18th March 2020 closing price, based on FY20E Peer Group Average Price-to-Earnings multiple of 9.80x. Peer companies taken for relative valuation are Challenger Ltd, NIB Holdings Ltd, Perpetual Ltd, and Platinum Asset Management Ltd, respectively.

Note: All the recommendations and the calculations are based on the closing price of 18 March 2020. The financial information has been retrieved from the respective company’s website and Thomson Reuters.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...