Company Overview: Mainstream Group Holdings Ltd, formerly MainstreamBPO Limited, is an independent fund administrator. The Company provides services for a client base of fund managers and superannuation trustees. The Company operates approximately three business lines, such as FundBPO, SuperBPO and ShareBPO. FundBPO provides investment administration, fund accounting, unit registry and middle office services to a range of investment managers. SuperBPO provides outsourcing services for superannuation funds, including member administration and communications, fund accounting and client reporting. ShareBPO provides share registry services for listed companies and exchange-traded funds. SuperBPO's clients include industry funds, corporate funds and master trusts. SuperBPO is involved in administering a range of superannuation products, including complex defined benefits schemes and pension and income streams. FundBPO operates in approximately three geographies, such as Australia, Hong Kong and Singapore..png)

MAI Details

Strong Sales Pipeline and Significant Growth in EBITDA: Mainstream Group Holdings Limited (ASX: MAI) provides global outsourced fund administration and custody services to a range of wealth management participants. As on 28 February 2020, the market capitalisation of the company stood at ~$67.24 million. During FY19, the company witnessed the 5th consecutive year of strong growth in revenue and EBITDA. Revenue of the company reached $50 million, up by $8.7 million on FY18. Majority of the revenue is sourced from organic growth from existing and new clients and recurring income from long term contracts with clients. In the same time span, EBITDA of the company went up by 17% to $7.4 million, and funds under administration reached $173 billion, achieving a growth of 24% on FY18. Over the span of 4 years from FY15 to FY19, the company witnessed a CAGR (compound annual growth rate) of 35.78% in revenue. The group, as on 30 June 2019 administers 1,012 funds for 356 clients. The company’s core business, Fund Services continued to perform strongly with significant investment made in Asia-Pacific and the Americas to take advantage of a strong sales pipeline. MAI is diversified by markets and asset classes and added 48 new funds under custody and 76 new private equity funds in FY19. The company is in a strong financial position with a solid balance sheet and a cash balance of $11.67 million. The decent financial position enabled the Board to declare a partially franked final dividend of 0.50 cents per share, bringing the total dividend per share to 1.25 cents. MAI will continue to pursue its financial objectives, including increasing its profitability over time by improving the performance of its existing business lines.

The company has also released its interim results for the period ending 31 December 2019 and reported substantial growth across Australia, Hong Kong, Singapore and USA. The diversified and high-quality client base, along with high levels of recurring revenue offers significant growth opportunities in the core markets. During 1H FY20, MAI reported a record FUA $187 billion, representing growth of 27% on the prior 12 months.

The company delivered on its strategy and provided global fund administration services to its client. MAI has built its business across multiple jurisdictions and is well placed for further growth. The group also offers revenue opportunities due to its size, investment in technology and expertise in managing regulatory change. MAI offers promising prospects and is on track to achieve its FY20 guidance..png)

FY19 Financial Highlights (Source: Company Reports)

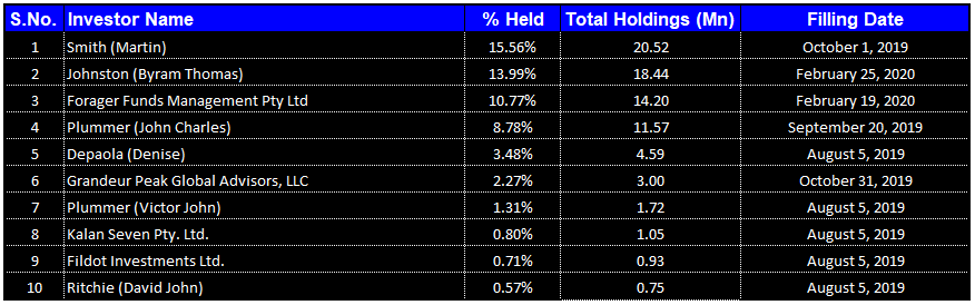

Details of Top 10 Shareholders: The following table provides an overview of the top 10 shareholders of Mainstream Group Holdings Limited. Smith (Martin) is the largest shareholder in the company, with a percentage holding of 15.56%.

Top 10 Shareholders (Source: Thomson Reuters)

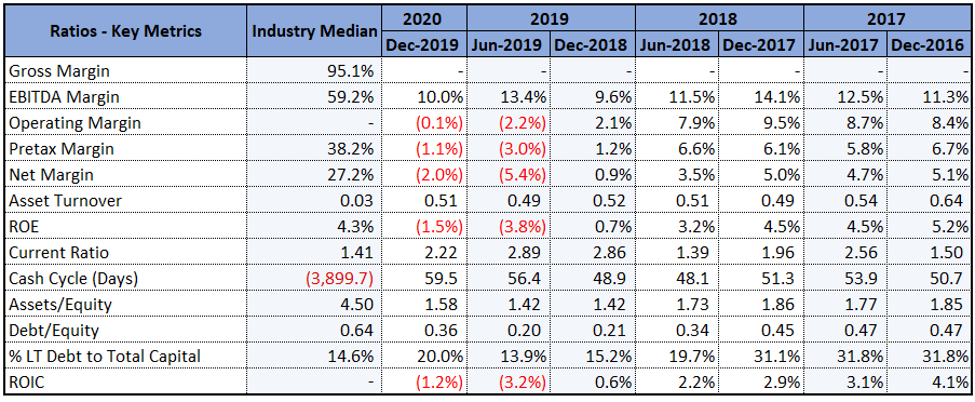

Increased Profitability and Good Management of Costs: During 1H FY20, EBITDA margin of the company witnessed a slight improvement over the previous corresponding half and stood at 10%, up from 9.6% in 1H19. This indicates the increased profitability of the business. In the same time span, net margin witnessed a slight improvement over the previous half, indicating that the company is managing its costs well and is capable of converting its revenue into profits. Return on Equity also improved over the previous half showing that the company is well deploying the capital of its shareholders. During 1H FY20, current ratio of the company stood at 2.22x, higher than the industry median of 1.41x, implying that the company is liquid enough to pay off its current liabilities using its current assets. In the same time span, Asset/Equity ratio of the company was 1.58x, lower than the industry median of 4.5x. This indicates that the business is financed with a larger proportion of investor funding and a small amount of debt, resulting in a financially stable balance sheet.

Key Margins (Source: Thomson Reuters)

Significant Growth Opportunities in Core Markets: As per the company’s internal management structure, the group is organised into business units based on geographic locations and has three reportable segments, including the Asia Pacific, the Americas and Europe. Asia-Pacific (APAC), which includes Australia, Singapore and Hong Kong, contributed 72% of the group’s revenue during the 1H FY20, whereas America accounted for 19% of the revenue. During FY19, the company reported highest revenue of $36 million from the Asia Pacific region, up by 15% on the previous year, followed by $9 million from the Americas and $5 million from Europe. This increase was mainly due to increased cross-sell opportunities through custody service expansion in the APAC region, build-out of private equity fund services in the Americas and Ireland migrating to Mainstream preferred hedge fund technology in the Europe region.

During 1H FY20, the company achieved substantial growth in mainstream funds under administration and witnessed a CAGR of 20% in Australia, 38% in Hong Kong, 21% in Singapore and 18% in the US in the past three years. The company has expanded its growth opportunities with the increasing size of fund assets, with 649 funds in the Asia Pacific, 233 in the Americas and 129 in Europe.

Mainstream’s Funds under Administration (Source: Company Reports)

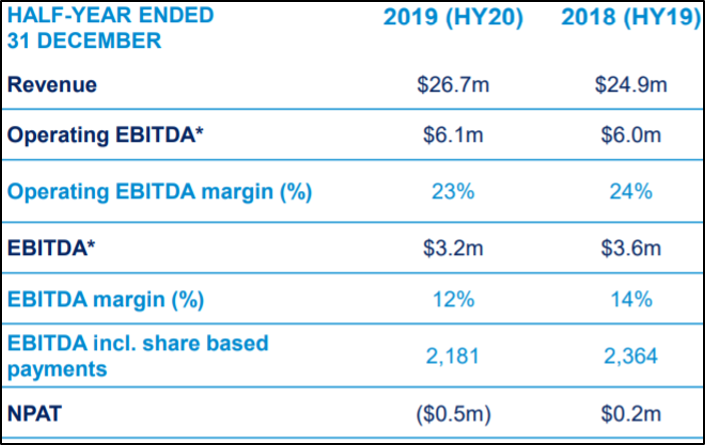

Record Funds Under Administration: The company has recently released its interim results for the period ending 31 December 2019, wherein it reported an increase in revenue by 7% to $26.7 million. Growth in revenue was organic, driven by ongoing demand for services in MAI’s core markets of Australia, Asia and the US. In the same time span, EBITDA of the company stood at $3.2 million, which was impacted by investment in automation and digital services to enhance its offering and boost demand.

During 1H FY20, the company reported record funds under administration of $187 billion, up by 27% from HY19. This growth was driven by rising growth in global stock markets and annual growth in net inflows of $13 billion. In line with the company’s strategy, MAI made several investments in future growth and recruited seven additional unit registry employees to support growth in Australian operations. The company made good progress in building higher margin businesses and maintained a net cash position in excess of regulatory capital requirements. The company invested in growth and reduced its 3-year debt facility from $7 million to $6 million.

1H FY20 Financial Performance (Source: Company Reports)

Future Expectations and Growth Opportunities: The company is well-positioned for continued growth and expects considerable opportunities from consolidation in the Australian fund admin and custody sector. The business model of MAI is based on high levels of recurring revenue from deep client relationships with further cross-selling opportunities and material long term agreements. MAI is trending towards growth, owing to its partnership with high quality fund managers. It also anticipates a strong sales pipeline from deep client relationships and growing brand awareness.

The company has provided guidance for FY20 and expects full year revenue of approximately $55 million. Further growth in investments and management restructure is expected to result in EBITDA of around $9 million. The company is also strategising to reward shareholders with dividends and anticipates partial franking levels as international profit continues to grow. MAI is focusing on investing in growth and expects to see the benefits of these investments in FY21. The company is progressing in higher private equity and custody businesses and is planning to launch quoted fund capability. These initiatives, along with disruptions in the Australian market, are expected to increase demand for MAI’s services.

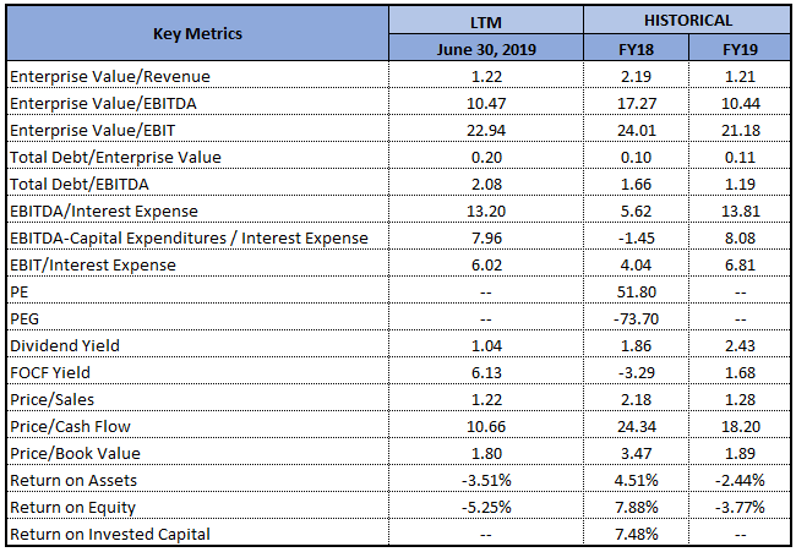

Key Valuation Metrics (Source: Thomson Reuters)

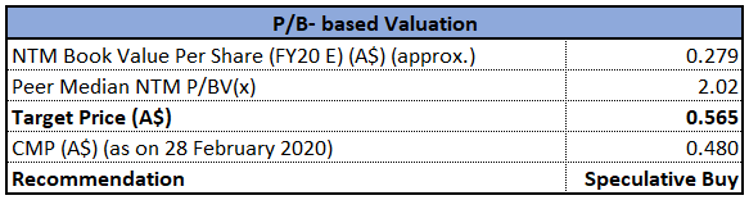

Valuation Methodology: Price to Book Value Based Relative Valuation

Price to Book Value Based Relative Valuation (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock of MAI gave a return of 2% in the past six months and a return of approximately 1% in the last three months. The stock is trading close to its 52-weeks’ low level of $0.430, proffering a decent opportunity for accumulation. The company has attractive fundamentals and is well positioned to benefit from a continued trend towards fund administration outsourcing and complicated compliance with the regulation. The company expects continued demand for services in core markets and is progressing well in building higher margin businesses. Considering the returns, trading levels, decent growth opportunities and significant growth in financial position, we have valued the stock using Price to Book based relative valuation approach and have arrived at a target price offering an upside of lower double-digit (in percentage terms). For the said purpose, we have considered Pacific Current Group Ltd (ASX: PAC), EQT Holdings Ltd (ASX: EQT), Primewest Group Ltd (ASX: PWG), etc., as peer group. Hence, we recommend a “Speculative Buy” rating on the stock at the current market price of $0.480, down by 5.882% on 28 February 2020.

MAI Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...