Company Overview – Magellan Financial Group is a fast growing Sydney based niche fund manager. Established in 2006 the fund specializes in the management of global equity and infrastructure funds for domestic retail and institutional investors. Magellan has been particularly successful in winning mandates from global institutional investors. Current funds under management is in excess of $20 billion dollars and is split between global equities, core and active infrastructure. Magellan has a reputation of one of Australia’s better franchises for international equities.

Analysis – Magellan Funds Management is an active international equity and infrastructure fund manager. Near term earnings growth is pinned by strong growth in funds under management or FUM complemented by performance fees. A long record of investment outperformance supports the case of further growth in FUM. Major risks to the earnings are the need to deliver strong investment returns and the volatile nature of large institutional mandates. Attractive long term industry dynamics are supported by increasing number of Australian investors seeking international equity exposure to diversify their Austral equities centric portfolios. Magellan does not focus on short term performance instead focusses on high quality stocks like to produce long term performance throughout the business cycle.

MFG Global Fund Performance (Source - Company Reports)

Attractive long term industry dynamics are supported by Australia’s ageing demographic and compulsory superannuation. High savings from superannuation necessitate an increase allocation to offshore equities with Magellan well positioned. Consistent inflow of retail funds under management or FUM underpins earnings momentum. Retail FUM is far stickier than institutional FUM and the management fees are twice the amount for institutional FUM.

MFG Infrastructure Fund Performance (Source - Company Reports)

Highly regarded management, a five year investment performance track record, sought after investment strategy and strong distribution capability in US, Canada and Europe is delivering considerable success in growing institutional funds under management. Funds management activities are undertaken by Magellan’s wholly owned subsidiary Magellan Asset Management. Funds under management has grown from $4 billion in June 2012 to $23 billion in June 2014 due to strong distribution capability and strong investment performance. For international wholesale investors Magellan’s investment returns and infrastructure funds stand out. Distribution remains the key with bulk of the distribution relationships formed on the back of Magellan’s head of distribution Frank Casssaroti’s 20 year plus experience at Colonial First State, one of Australia’s largest financial planning network.

MFG Global Fund FUM + Inflows (Source - Company Reports)

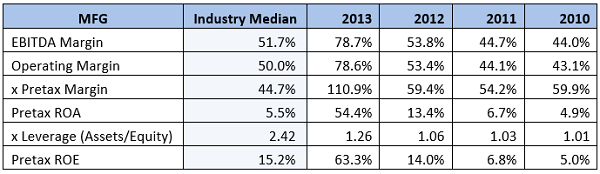

We like Magellan’s long term equity selection methodology. Entry barriers exist with major hurdles for aspiring competitors arising from the need to establish a retail and wholesale distribution capability and the need to develop close relationships with wholesale investors prepared to back start up fund managers. Traditional wealth manager business models boast strong operating leverage and Magellan is no exception with impressive returns on equity. A fast growing reputation for strong investment performance means it is less it is less pressured than peers to reduce management fees. Traditional independent asset managers typically receive a smaller share of the asset management fee from the providers of retail funds management platforms, but Magellan appears to have reversed the status quo, a testament to the firm’s reputation, strong investor relationships and rapidly improving brand. We do express some caution regarding the outlook considering Magellan has yet to be fully tested through the investment cycle with the predominantly US mega cap quality stock strategy.

Key strengths of the business include access to a large retail distribution network via independent financial advisors, a low cost base and strong long term industry growth prospects. A mild competitive disadvantage is that the distribution network is nonaligned, but this is offset by an emerging brand and impressive investment returns. Australia’s compulsory superannuation system underpins long term growth in superannuation assets with industry experts predicting the pol of retirement assets to grow at a 9% compound annual growth rate to more than AUD 5 trillion by 2025. Our positive investment view is based on Magellan delivering sustainable earnings growth on the back of strong growth in funds under management of 25% per annum during the next five years.

Downward margin pressure is a key risk but we are confident the firm will be able to limit the earnings impact due to solid growth in higher margin retail funds under management. We expect tight cost control to feature despite the very strong top line revenue growth. Magellan’s intangible assets are a key source of competitive advantage with an emerging brand and entrenched domestic and international sales relationships providing clear differentiation with peers. Switching costs provide a durable competitive advantage due to the perceived benefits of switching from one fund manager to another are so uncertain investors often take the path of least resistance and remain with incumbent managers.

MFG Daily Chart (Source - Thomson Reuters)

For Australian investors, Magellan’s switching cost benefit is enhanced by its strong investment performance. Higher margin and sticky retail customers ( we estimate an average margin of 1.10%) account for around 30% of the $23 billion in total funds under management, while 70% is lower margin institutional FUM ( margin estimated at 0.40%). In our opinion Magellan’s institutional FUM is less sticky than retail but institutional FUM is supported by multiyear mandates and retention based on achieving benchmark returns. Magellan’s style and investment track record suggest a high probability of achieving or exceeding return benchmarks.

In our view Magellan’s competitive advantages in both retail and to a lesser extent wholesale are sustainable. Magellan has very successfully and in a very short time frame, attracted significant amounts of funds under management necessary to generate excess returns on capital. Increasing numbers of Australian retail investors are seeking to diversify offshore. A combination of a high concentration of resources and financial stocks in the Australian market, an arguably overvalued Australian dollar and an increasing pool of retirement savings is motivating retail and institutional investors to more actively consider international equities.

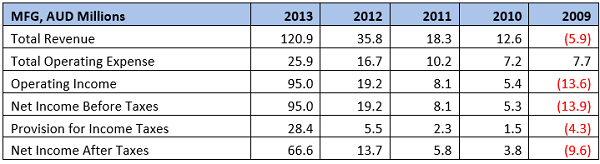

Magellan is in sound financial health. Magellan is generating strong profit growth and we expect dividends to increase at least match earnings per share growth. Magellan has a conservative balance sheet with no debt. Magellan’s financial position is boosted by cash, substantial liquid investments and solid operational cash flows. As at 31

st December 2013 cash levels stood at AUD 35 million with a further AUD 15.8 million of fixed term deposits. In our opinion Magellan is one of the better franchises to service the increasing demand for international equities. Senior management are co-founders and major shareholders and we expect the conservative balance sheet settings to buffer future unforeseen events and market volatility. We rate the co-founders Chris Mackay and Hamish Douglas highly as they have been impressive performers since establishing the business in 2006.

Inflows of AUD 1.5 Billion during the march quarter takes funds under management or FUM up an impressive 52% to AUD 22.4 billion in the nine months to 31

st March 2014. Continuing its run of inflows Magellan has attracted a very strong AUD 1.2 billion worth of institutional money in July. Put into context the monthly institutional fund inflows for the six months leading up to June 2014 was around $295 million. The AUD 138 million of domestic net retail inflows were more in line with the AUD 150 million per month average in the past six months. Total FUM to 21 July 2014 increased AUD 1.4 billion to AUD 24.9 billion.

Magellan continues to invest in and develop the firm’s distribution capabilities employing well know and established development managers in the retail and institutional space. Magellan is well positioned to take advantage of increasing flows leading to growth in assets under management and management fee income. In the long term the pool of assets supporting Australia’s compulsory superannuation system will likely outgrow the Australian stock market necessitating a higher allocation to international equities. Fund inflows continue to grow while other high profile Australian fund managers struggle to gain traction with investors. Sustained improvement in equity market conditions would boost investor confidence and increase demand for actively managed equity investments. We see Magellan as favorably positioned to capitalize on the chronic under allocation to global equities by self-managed super funds. We put a BUY recommendation on the stock at the current price of $11.50.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...