Kalkine has a fully transformed New Avatar.

Company Overview: Maca Limited (ASX: MLD) is an Australia-based company, which is engaged in provision of civil and contract mining services throughout Australia and mining services to the mining industry in Brazil, South America. Its mining business specializes in providing mining and crushing services predominantly to mid-size mining projects across a range of commodities. Through its civil construction and asset maintenance businesses, the company provides a range of civil infrastructure and maintenance services to government and private organizations. Its mining services and civil construction business provides open pit contracting services to the mining industry, including loading and hauling, drilling and blasting, crushing and screening and civil infrastructure services to public and private industry..png)

MLD Details

Top-line grew at a CAGR of 2.57% over FY15-19: Maca Limited (ASX: MLD) is involved in three businesses and two geographical segments with the provision of civil contracting services, contract mining services and mineral processing services throughout Australia, and contract mining services in Brazil, South America. Its revenue is derived from contract services, sale of inventory and others. Contracts for services include drill and blast, earthmoving, infrastructure, contract mining, excavation, crushing and road construction and maintenance. For rental of equipment, as per agreed contract, MLD has an enforceable right to receive payment, as the customer simultaneously receives and consumes the benefits. Other revenue primarily includes dividends received, profit or loss on the sale of assets or investments, government rebates and interest income, recognized on an accrual basis.

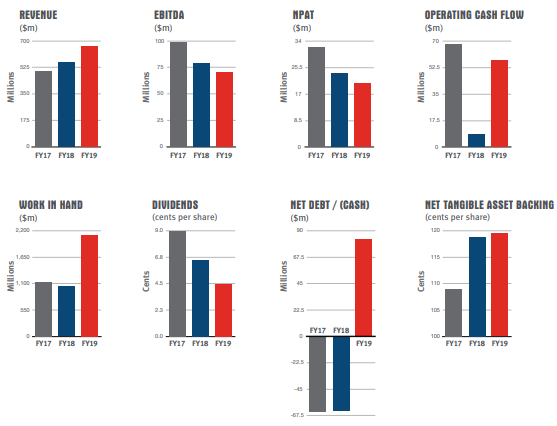

Looking at the past performance over FY15 to FY19, total revenue of the company has grown at a CAGR (compounded annual growth rate) of 2.57%. Group’s total revenue improved from $601 million in FY15 to $665.3 million in FY19.

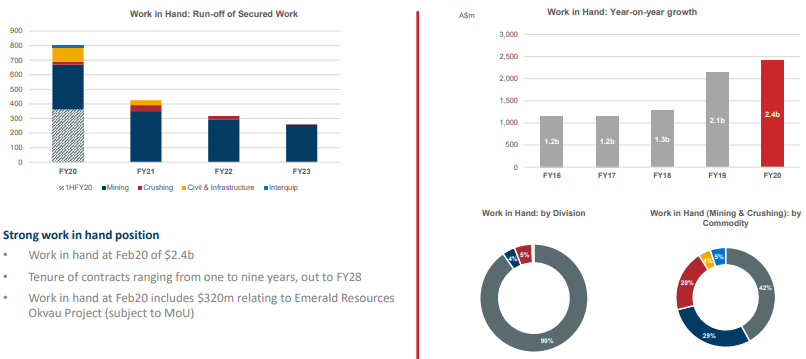

MLD maintains a positive outlook for FY20, supported by favorable market conditions in the concerned sectors, strong work in hand position of $2.4 billion in February 2020 and a strong pipeline of opportunities with existing and new clients. Its operational activities in Brazil will cease soon, while it is expected to commence operations in Cambodia by first half of FY21. Robust pipeline of development in the West Australian iron ore sector is expected to drive demand for significant bulk earthworks projects, alongside strategic targeting of public sector projects. Moreover, the company is expected to improve on debt management, and rationalize its balance sheet throughout FY20 and into FY21.

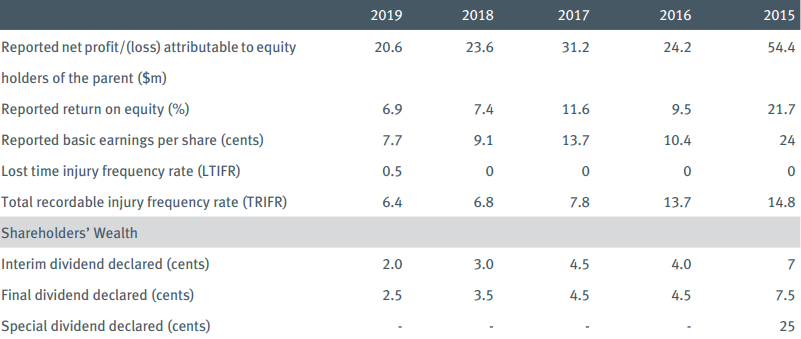

MLD’s Past Performance Highlights (Source: Company Reports)

FY19 Key Highlights for the period ended June 30, 2019: Group’s revenue for the period was reported at $665.7 million, an increase of 18% on the previous year. Revenue for Civil Construction and Infrastructure Maintenance division was reported at $139 million, and revenue for the mineral processing equipment businesses increased from $21 million to $51 million.

EBITDA for the period was reported at $70.7 million, a decline of 8% on the previous year. Net profit before tax for the period was reported at $32.0 million, an increase of 1% on the previous year. NPAT attributable to members for the period was reported at $20.6 million, a decline of 13% on the previous year. Work in hand at the end of the period was reported of value $2,110 million, as compared to $1,051 million at the end of the previous year.

FY19 Key Metrics (Source: Company Reports)

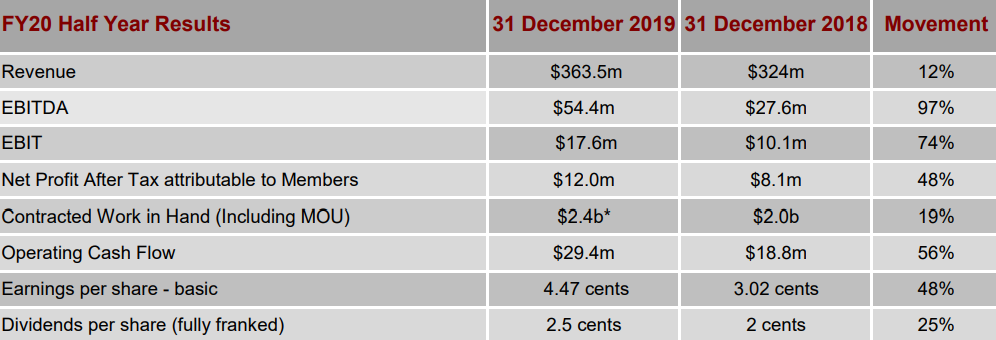

H1FY20 Key Highlights for the period ended December 31, 2019: The company’s half year net profit after tax attributable to members was reported at $12.0 million, an increase of 48% on the previous corresponding period (pcp). Revenue for the period was reported at $364 million, an increase of 12% on pcp. Earnings before Interest, Tax, Depreciation and Amortization (EBITDA) for the period was reported at $54.4 million, an increase of 97% on pcp, consistent with the previously advised FY20 EBITDA guidance of $104 to $110 million (excluding the impact of forex losses). The Board announced an interim dividend (fully franked) of 2.5 cents per share, with record date and payment date on 9 March 2020 and 19 March 2020, respectively.

H1FY20 Key Metrics (Source: Company Reports)

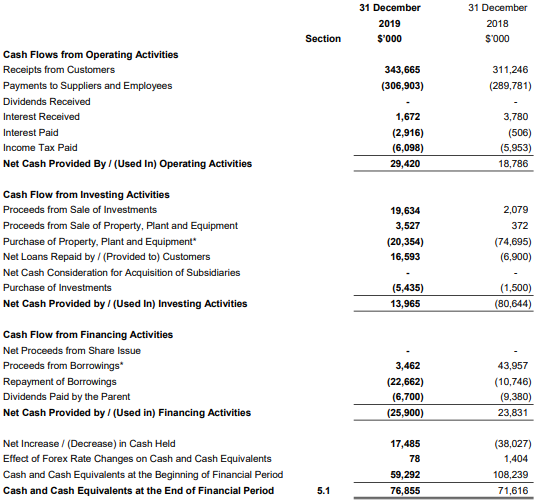

Cash Balance as on December 31, 2019 Stood at $76.9 Mn: Operating cash flow for the period was reported at $29.4 million. As client loan positions unwind, operating cash flow for the second half FY20 is expected to be stronger. Capital expenditure relating to plant and equipment for the first half of FY20 was reported at $42 million. Capital commitments predominately relating to the Ravensthorpe project for the second half of FY20 currently stands at $52.1 million. The company deployed a combination of cash and equipment finance contracts for the capital equipment purchases. Group’s cash position as on December 31, 2019 was reported at $76.9 million, with net debt of $81.8 million (inclusive of $13.0 million of operating leases recognized under AASB 116).

H1FY20 Cash Flow Statement (Source: Company Reports)

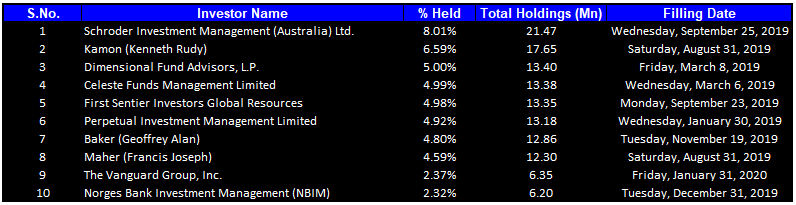

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together form around 48.56% of the total shareholding. Schroder Investment Management (Australia) Ltd. and Kamon (Kenneth Rudy) hold maximum interests in the company at 8.01% and 6.59%, respectively.

Top 10 Shareholders (Source: Thomson Reuters)

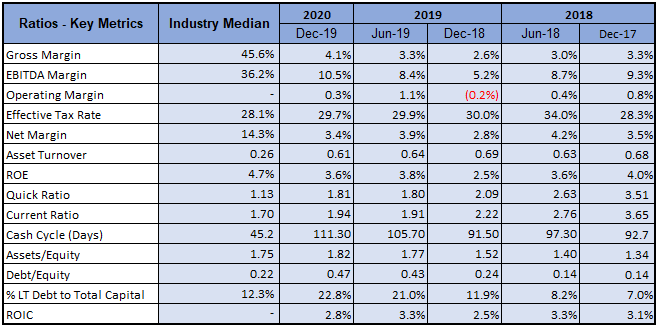

A Quick Look at Key Metrics: Its gross margin, EBITDA margin and net margin for H1FY20 stood at 4.1%, 10.5% and 3.4%, better than the H1FY19 result of 2.6%, 5.2% and 2.8%, respectively, implying an improvement in the company’s fundamentals. ROE for H1FY20 stood at 3.6%, better than the H1FY19 result of 2.5%. Its current ratio for H1FY20 stood at 1.94x, better than the industry median of 1.70x, which implies that the company is in a good position to address its short-term obligations.

Key Metrics (Source: Thomson Reuters)

What to expect: As per the release, the company was awarded the Greenfinch open pit mining contract by Ramelius Resources Limited (ASX: RMS), wherein it would provide load and haul, and, drill and blast services to RMS, generating revenue of $41 million over the 16 month term with operations commencing in March 2020.

Outlook for the activities within mining sector remains strong and the company is well placed to benefit from the opportunities available and consolidation within the contracting space. The Company has work in hand of worth $2.4 billion and expects further to grow in the coming years. With improved operational delivery, the civil and Infrastructure divisions are expected to deliver significant revenue growth in the second half of financial year 2020. Revenue guidance for FY20 has been anticipated at ~$770 million and EBITDA has been anticipated in the range of $104 million to $110 million.

Work in Hand Information (Source: Company Reports)

Key Valuation Metrics (Source: Thomson Reuters)

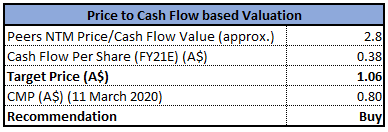

Valuation Methodology: Price to Cash Flow Multiple Based Relative Valuation

Price to Cash Flow Multiple Approach (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Technical Analysis:

Monthly Chart:

(Source: Thomson Reuters)

Weekly Chart:

(Source: Thomson Reuters)

On both monthly and weekly chart, the stock seems to be moving in a downtrend. However, it is trading close to a strong support level around ~$0.645, which suggests the probability for a bounce-back. Stochastic Oscillator also indicates that there might be slowdown in the bearish momentum in the coming days and buyers would be in a position to come into the picture. On any bounce-back, the stock may test the level around 20 EMA.

Note: EMA – Exponential Moving Average

Stock Recommendation: MLD’s stock posted a negative one-year return of 7.41% and a negative return of 5.91% in the span of six months. It is trading below the average of 52-week high and low level of $1.200 and $0.710, respectively, proffering a share accumulation opportunity for the investors. The company is well-positioned to deliver quality services to customers in the mining, civil and infrastructure and SMP sectors, and is selectively identifying further development opportunities. Considering the recent mining services win in the Goldfields Esperance region with FQM Australia Nickel at Ravensthorpe, further civil construction awards in Victoria and with work in hand at $2.4 billion, we have valued the stock using price to cash flow based relative valuation method and arrived at a target price of double-digit upside (in % terms). Hence, we give a “Buy” recommendation on the stock at the current market price of $0.800, down 8.571% on March 11, 2020.

MLD Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...