Kalkine has a fully transformed New Avatar.

Company Overview: Lovisa Holdings Limited is engaged in the retail sale of fashion jewelry and accessories. The Company's segments include Australia & New Zealand, which is engaged in the retail sale of women's jewelry and accessories in Australia and New Zealand, and Rest of the World, which is engaged in the retail sale of women's jewelry and accessories in Singapore, South Africa, Malaysia and the United Kingdom. The Rest of the World segment also includes the Company's franchise stores in the Middle East. The Company utilizes daily inventory monitoring software and airfreight to move product to store locations within approximately 48 hours from its centrally located warehouses in Melbourne and Hong Kong. The Company has over 230 retail stores. Its each store contains an average of over 2,500 product lines. It operates in Australia, New Zealand, Singapore, Malaysia, South Africa and the United Kingdom, and franchised stores in the Middle East (Kuwait, the United Arab Emirates and Saudi Arabia)

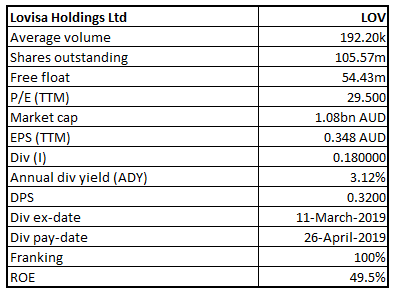

LOV Details

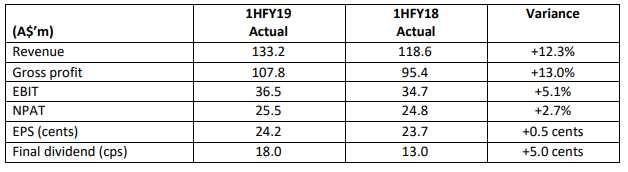

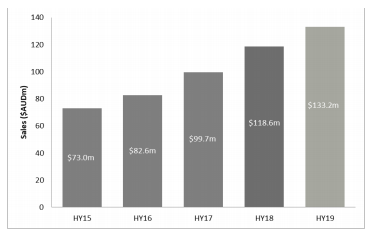

Decent Performance in 1H FY19: Lovisa Holdings Limited (ASX: LOV) is an ASX-listed company, which is primarily engaged in the business of retail sale of the fashion jewellery and accessories. As on August 12, 2019, the market capitalisation of Lovisa Holdings stood at ~A$1.08 billion. The company earlier released its results for the half-year ended December 2018 or 1H FY19 in which its revenue stood at $133.2 million which reflects a rise of $14.6 million (or 12.3%) on 1H FY18. It was added that the revenue growth was achieved through the net opening of 33 new company owned stores as well as 7 new franchise stores. The company’s gross profit amounted to $107.8 million, which implies a rise of $12.4 million on prior half. Its gross margin stood at 81% in comparison to 80.4% for 1H FY18. Additionally, it was added that the gross margin on a constant currency basis stood at 80.5%. The company’s cost of doing business (or CODB) for 1H FY19 stood at 50.4%, as compared to 48.1% for the first half of last year and the company continues to deploy towards the expansion of the global footprint. The company has a robust balance sheet, and its net cash stood at $32 million on hand. Based on the decent performance in 1HFY19, the company has declared an interim dividend amounting to 18 cents per share (fully franked). The company’s cashflow was robust, and its cash from operations before interest and tax amounted to $49.1 million which was supported by the operating cash conversion at 121% and the company continues to manage its working capital well in the face of the ongoing investment towards stock for the new stores as well as to support the e-commerce.

It was stated that the primary driver of the future growth for the company is continued international store roll out. The store network witnessed a rise to 366 stores as at the period end, which reflects a net increase of 40 stores from June 2018. It was stated that 51 new stores were opened, and 11 stores were closed as part of the ongoing store network optimization process. Additionally, operational and revenue generation capabilities along with decent liquidity levels might be tailwinds for the company’s growth.

Result Highlights (Source: Company Reports)

Top 10 Shareholders: The following table provides a broader overview of the top 10 shareholders in Lovisa Holdings Limited:

Top 10 Shareholders (Source: Thomson Reuters)

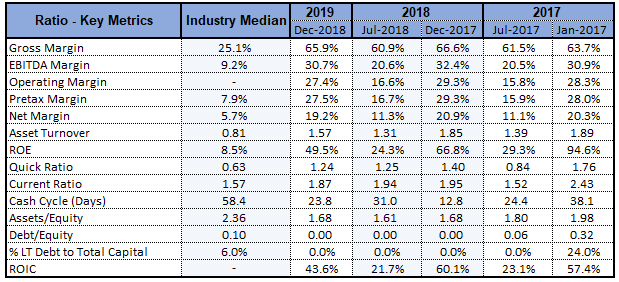

Key Ratios Higher Than Broader Industry Median: The company has reported decent key financial ratios in 1H FY19 as compared to the broader industry median, which reflects the decent financial position of the company. Lovisa’s net margin stood at 19.2% in 1H FY19, which is higher than the industry median of 5.7%, reflecting that the company has better capability to convert its top-line into bottom-line as compared to the broader industry. The company’s EBITDA margin stood at 30.7% in 1H FY19, which is higher than the industry median of 9.2%. The company’s RoE stood at 49.5% in 1H FY19 which is significantly higher than the industry median of 8.5% and, thus, it looks like that the company has been delivering higher returns to its shareholders when compared to the broader industry. It can be said that the company’s decent footing with respect to its key margins and higher RoE might help it in gaining traction among the market players.

Key Metrics (Source: Thomson Reuters)

The company is having current ratio of 1.87x which is marginally higher than the industry median of 1.57x and, thus, it looks like that the company is having decent liquidity position which might help it in meeting its short-term obligations. Additionally, the respectable liquidity levels provide the company with sufficient headroom to make deployments to achieve long-term growth.

Understanding Viewpoints On The US Market: The company stated that it has traded in the US since November 2017, and considering the pleasing performance of 8 stores trading in California market, the company is optimistic and there are expectations that it would continue the store rollout with the knowledge that Lovisa offer is resonating with American consumer. The company further stated that the US represents a significant opportunity, however, it would continue with the cautious as well as disciplined approach with size and timing of store rollout dependent on the delivery of the quality stores rather than hitting the store number targets.

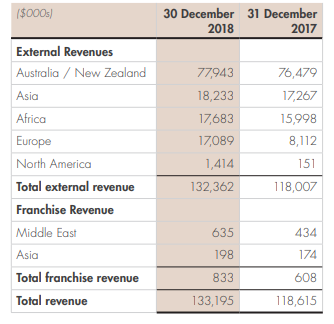

Revenue By Nature And Geography (Source: Company Reports)

Store Rollout Helped Total Global Sales Revenue: Lovisa Holdings Limited stated that the total global sales revenue witnessed an increase of 12.3% and stood at $133.2 million because of the acceleration in the store rollout. The company further stated that they were focused towards preserving the gross margin throughout the period. Additionally, Lovisa Holdings Limited added that comparable store sales witnessed a decline of 1.8% and was impacted by the difficult conditions in the Australian market.

Sales (Source: Company Reports)

Europe and USA sales imply continued new store growth, and there was an increase of 12 stores in the UK, five stores in France, three stores in Spain as well as 7 in the US. However, the Australian region was impacted by the softer trading conditions and robust prior half year performance. It was added that South Africa has been performing well and there was growth from existing and new stores.

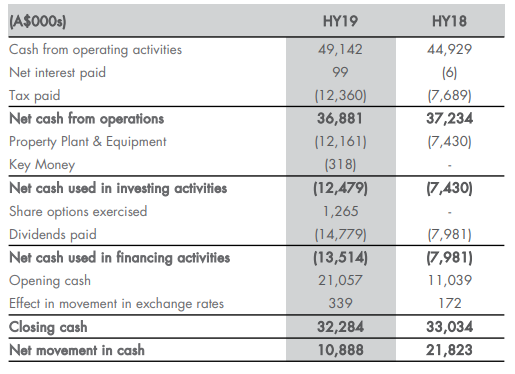

Analysing Cash Flow Position: The company’s cash flow from operating activities witnessed a rise of 9.4% and stood at $49.1 million and its operating cash conversion stood at 121%. The company has witnessed increased capex spend per store considering the scale and rollout in the new markets. The following picture provides an overview of the company’s cash flow:

Cash Flow (Source: Company Reports)

The company added that deployment towards the growth of business has continued and there has been addition of numerous senior leadership roles into the structure in order to lead existing as well as new territories. It was stated that the acceleration of rollout in the new territories has led to an increase in CODB and there were higher initial operating costs. There has been deployment towards the implementation of e-commerce site, and it has been live since the month of October.

What To Expect From LOV: The company stated that the trading since the end of the half-year witnessed an improvement throughout all the markets and there have been positive comparable store sales for the period. The company has been focusing on ensuring that robust gross margins are maintained, and costs remain well controlled. It also plans to deploy towards future growth of the business. As of now, the company is focusing on the expansion of the store network, and there are expectations that an increase in the number of stores for 2H FY19 would be higher than in 2H FY 2018. Also, the company would continue to deploy towards the support structures ahead of the growth curve in order to drive the store network expansion as well as support the larger business.

With respect to the USA and Europe, the company added that it would continue to apply the diligent approach to new store evaluation in order to ensure that it maintains quality of the store network, and it would not sacrifice the store quality for the speed or size of rollout. The company continues to focus on deployment in people and processes in order to ensure that they remain efficient as it grows and able to execute on the strategic plans.

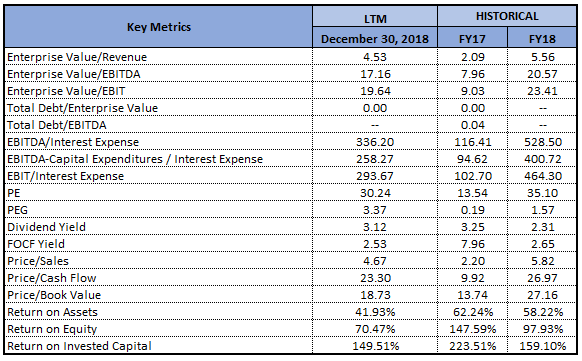

Key Valuation Metrics (Source: Thomson Reuters)

(3).png)

Historical P/E Band (Source: Company Reports, Thomson Reuters)

Stock Recommendation: The company’s stock has delivered a return of 34.87% in the span of previous six months, while in the time frame of past three months, the stock’s return stood at 7.89%, proffering decent returns over the said period. At CMP of $10.85, an annual dividend yield of the company stands at 3.12%, which can be considered at decent levels. The company has appointed numerous important roles to business like Chief Operating Officer, Executive Vice President Europe & Africa, Vice President Retail Stores and Operations USA as well as Leasing Managers in France and East Coast USA. From the analysis standpoint, the company’s position is looking quite good as it has witnessed a CAGR growth of 19.70% in its top-line between FY14- FY18 which reflects that it is possessing decent revenue-generation capabilities. During the same period, the bottom-line encountered a CAGR growth of 67.26% and cash flow from operations witnessed a CAGR growth of 32.87%. There are expectations that its capabilities to generate revenues along with its operational capabilities might help the company in further improving its performance moving forward. Considering these factors, we have valued the stock using the 1-standard deviation to 3-year average of P/E market multiples of around 29.5x for FY20E with consensus EPS of $0.394 and have arrived at target price upside of single-digit growth (in %). Based on the foregoing, we give a “Buy” rating on the stock on the at the current market price of A$10.850 per share (up 5.854% on 12 August 2019), ahead of its full-year results which are to be released on 22 August 2019.

.png)

LOV Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...