Company Overview: Lendlease Group (ASX: LLC) is a real estate group that is into retail property management, asset management and development and operates in the Europe, Asia Pacific and the Americas regions. The large-scale urban regeneration and greenfield development projects come under its portfolio. Lendlease Corporation Limited, and its controlled entities, also Lendlease Trust are included as company’s entities; and thus, the group forms a REIT (real estate investment trust), well known in Australia. It delivers critical infrastructure, stadiums and entertainment facilities around the world, hospitals, schools, shopping centres, residential communities, high rise apartment buildings, etc. LLC focuses on enhancing its ability to originate, fund, build, deliver and manage major urbanisation and critical infrastructure projects. The company’s integrated business model, financial strength along with exceptional track record provides it a point of difference. Its approach is disciplined and is supported by the robust risk management and governance framework.(1).png)

LLC Details

.PNG)

Decent Results in 1H FY 2020: Lendlease Group (ASX: LLC) carries out operations in Asia Pacific, Europe and the Americas and has a market capitalisation of ~$6.04 billion as on April 2, 2020. It has recently released a decent set of numbers for half-year ended December 2019 wherein it grew the urbanisation pipeline significantly, completed another world class urban precinct and made progress with regards to the sale of Engineering business. These along with other initiatives strengthened the business and has positioned it for long-term growth. The continued origination success has driven LLC’s urbanisation pipeline to around $100 billion within the total development pipeline of $112 billion. The company recorded core business profit after tax of $308 Mn with RoE of 9.6% in 1HFY20. The company’s key focus is on driving securityholder value via delivery of growing pipeline of development projects. Its gearing stood at 14.75%, which happens to be the mid-point of 10-20% target range and there are expectations that it would be in the range of 15%-20% at FY 2020 end. The company’s core operating EBITDA amounted to $628 million. Its construction and investments segments managed to deliver robust results which were in line with the portfolio targets. The returns of development segment were below the target, however, the earnings for this segment have been anticipated to be skewed towards 2H of the financial year. LLC’s non-core engineering and services segment posted EBITDA of $23 million and PAT of $5 million.

Notably, it has entered into an agreement to divest its engineering business for the consideration of $180 million and this transaction is expected to be wrapped up in 2H of the financial year. Also, the sale process for its Services business continues. The company’s dividend payout ratio was slightly above the mid-point of its target range. With regards to the near term outlook, the core business is supported by expected conversion of the commercial and residential development opportunities throughout the major urbanisation projects. The company is well positioned for long-term growth and continues to implement the strategy of delivering urban precincts while having a strong focus on environmental and social outcomes..png)

Key Financial Highlights (Source: Company Reports, Thomson Reuters), * Total Dividend/Distribution per stapled security

Top 10 Shareholders: The following image provides a broader overview of the top 10 shareholders in LLC:.png)

Top 10 Shareholders (Source: Thomson Reuters)

Overview of Key Margins: The company’s EBITDA margin 4.7% in 1H FY 2020 which reflects an increase from 1H FY 2019 figure of 2.9%. Its gross margin stood at 10.4% in 1H FY 2020 while in 1H FY 2019 it was 7.4%. LLC’s current ratio stood at 1.03x in 1H FY 2020 as compared to 1.02x in 1H FY 2019 and, therefore, it can be said that the company can meet its short-term obligations. Moreover, decent liquidity footing might help it to make deployments towards growth prospects. .png)

Key Metrics (Source: Thomson Reuters)

The company’s percentage of long-term debt to total capital stood at 34.7% in 1H FY 2020 which is lower than 1H FY 2019 figure of 35.5% and, thus, it can be said that LLC has reduced its exposure towards long-term debt. Generally, lesser exposure towards long-term debt helps the company to focus towards long-term growth catalysts.

Appointment of Robert Welanetz: Lendlease Group made an announcement about the appointment of Robert (Bob) Welanetz to the Board as an Independent Non-executive Director. He would be standing for election at LLC’s annual general meeting on November 20, 2020. He is based in the US and possesses significant executive, advisory, strategic as well as operational experience in property and construction sectors.

Unloading of Engineering Business: In the month of December 2019, Lendlease Group entered into an agreement with Acciona Infrastructure Asia Pacific to sell its engineering business. The purchase consideration for the said purposes amounted to $180 million. The company added that the sale of Engineering business happens to be a crucial milestone which provides a clear pathway for the people, partners, clients and securityholders. Also, it would be allowing LLC to focus on core competitive advantages.

As per the terms of the agreement and subject to completion of the conditions precedent, Acciona would be acquiring engineering business excluding NorthConnex and Kingsford Smith Drive projects. These projects are in the final stages and would be completed by Lendlease. Also, the Melbourne Metro Tunnel Project has been currently excluded, and project consortium is working with government on the confidential basis in order to resolve issues with regards to scope and costs.

Significant YoY Rise in Distribution Per Security: LLC stated that an unfranked interim distribution amounting to $169 million has been approved. Notably, interim distribution comprises an unfranked dividend which amounted to 22.1 cents from the company and the trust distribution of 7.9 cents per unit from Lendlease Trust. Therefore, distribution per security comes out to 30.0 cents in 1H FY 2020 which is significantly higher than 1H FY 2019 figure of 12.0 cents. The dividend pay-out ratio happens to be slightly above the mid-point of target range, and this could attract the attention of the market players moving forward..png)

Dividends/Distributions (Source: Company Reports)

Overview of Portfolio Management Framework: The company stated that Portfolio Management Framework has been designed in order to maximise the long-term securityholder value through 1) A diversified risk adjusted portfolio, 2) Leveraging competitive advantage of integrated model, 3) Optimising business on the long-term basis, and 4) Providing financial strength in order to execute the strategy, maintaining investment grade credit rating as well as capacity to absorb and respond to the market volatility..png)

Portfolio Management Framework (Source: Company Reports)

What to Expect from LLC Moving Forward: The company is focused on delivering the urbanisation portfolio safely, sustainably and profitably. Its portfolio of 21 major urbanisation projects throughout 9 gateway cities give long term earnings visibility along with strong platform to deliver enhanced risk adjusted returns to the securityholders. The company’s funds under management increased 8% on the YoY basis to $37 billion. LLC is well positioned to double its funds under management as the company’s urbanisation pipeline gets delivered.

The outlook for construction segment is robust, as there is backlog revenue amounting to $14 billion. The established construction business in Americas has a decent market share in the target cities and sectors with backlog revenue amounting to $5.3 billion. The robust growth in urbanisation pipeline to around $30 billion in the region gives significant opportunities for the future construction backlog. The investments segment has been providing robust base of recurring earnings to the group. The company added that continued growth in the FUM would be supporting operating earnings moving forward.(2).png)

Key Valuation Metrics (Source: Thomson Reuters)

Valuation Methodologies:

Method 1: P/E Based Relative Valuation.png)

P/E Based Relative Valuation (Source: Thomson Reuters)

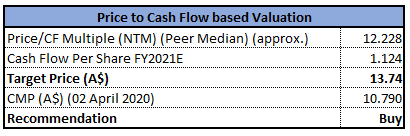

Method 2: P/CF Based Relative Valuation

P/CF Based Relative Valuation (Source: Thomson Reuters)

Stock Recommendation: The company’s total revenue has witnessed a CAGR of 5.64% between FY 2015- FY 2019 and, therefore, it can be said that LLC is possessing decent capabilities to garner revenues which could help it further strengthening its financial footing. The diversification of investments throughout the group helps the improved risk adjusted returns. The company is having relationships with around 150 institutional investors as well as solid track record of performance. The delivery of attractive outcomes for capital partners would be critical for ongoing success of investments segment. Considering the focus of the company towards leveraging competitive advantage via urbanisation and investment platforms along with positive outlook for construction segment, there are expectations that LLC might attract attention of market players. We have applied two relative valuation methods, i.e., P/E multiple and P/CF multiple, and arrived at a target price of lower double-digit upside (in % terms). Thus, we give a “Buy” rating on the stock at the current price of A$10.790 per share, up by 0.841% on April 2, 2020.

.png)

LLC Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...