Kalkine has a fully transformed New Avatar.

Company Overview: LendLease Group is an integrated international property and infrastructure company. The Company consists of Lend Lease Corporation Limited and its controlled entities, including Lend Lease Trust. Its segments include Property Development, Infrastructure Development, Construction and Investment Management. It is engaged in designing, developing, constructing, funding, owning, co-investing in, operating and managing property and infrastructure assets. The Property Development business involves the development of inner and outer urban developments, apartments, commercial offices, retail centers, healthcare facilities and retirement villages. The Infrastructure Development business arranges, manages and invests in public private partnership projects. The Construction business involves project management, building, engineering and construction services. The Investment Management business involves property and infrastructure investment management, property management and asset management.

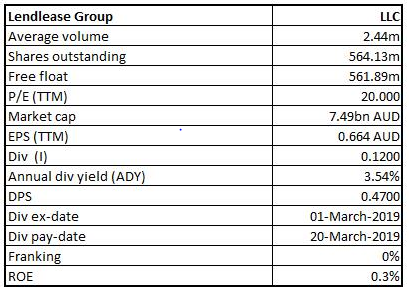

LLC Details

Global Trends Are Influencing LLC’s Strategy: Lendlease Group (ASX: LLC) is carrying out its operations in Asia Pacific, Europe as well as Americas regions. It is engaged in retail property management, asset management and development, etc. As on June 13, 2019, the market capitalisation of Lendlease Group stood at ~A$7.49 billion. It had recently released its presentation at Credit Suisse Asian Investment Conference in which it highlighted its approach, pillars of value, global trends and other important metrics.

The company stated that there are certain global trends which are influencing its strategy. There are expectations that by 2030, more than 60% of the world’s population is anticipated to live in the urban areas and the company is having urbanisation pipeline amounting to $59.3 billion. The company added that global assets under management are expected to witness a rise from US$85 trillion in 2016 to US$145 trillion by 2025 and the company has achieved 17.8% annual growth with respect to the funds under management since FY 2014. In the presentation, the company also highlighted its globally diverse pipeline which provides long-term earnings visibility. In the Americas, LLC is possessing development pipeline amounting to $7.9 billion while the construction backlog was $6.2 billion. However, in Australia, the company’s development pipeline amounted to $31.1 billion and the construction backlog stood at $6.6 billion. The company stated that its strategy is focused towards the integrated model which leverages more than one operating segment across the diversified portfolio. The company stated that it has intentions to review the capital structure because of the change with respect to the business mix as well as expected lower volatility of earnings. At CMP of $12.99, the stock of the LLC is trading at P/E multiple 16.38x of FY19E EPS. In the long run, we are affirmative on the stock as the company is expected to be helped by its investment segment, which is strong position, long-dated projects, growing pipeline and competitive advantage of the integrated business model. Hence, keeping the view of a decent outlook in the business along with mixed challenges, we have valued the stock based on 5-year average P/E multiple of 12.9x to FY20E consensus EPS of $1.21 and arrived at the target price of around $15.7, which is offering a lower double-digit upside potential (in %).

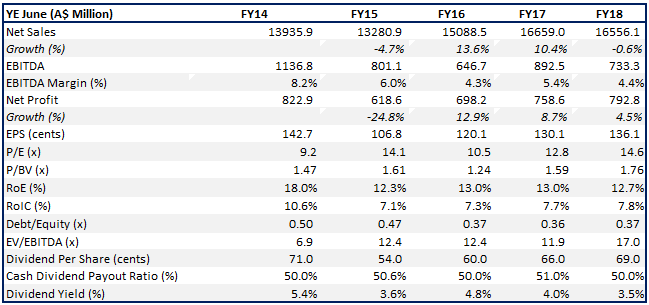

Key Financial Metrics (Source: Company Reports, Thomson Reuters)

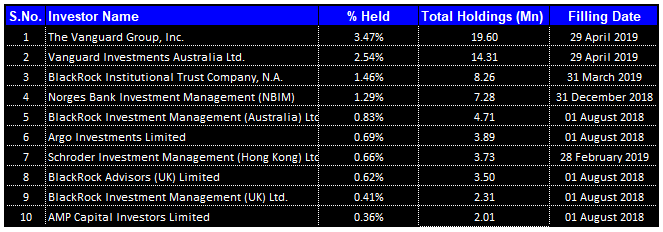

Top 10 Shareholders: The following table gives the broader picture of the top 10 shareholders of Lendlease Group:

Top 10 Shareholders (Source: Thomson Reuters)

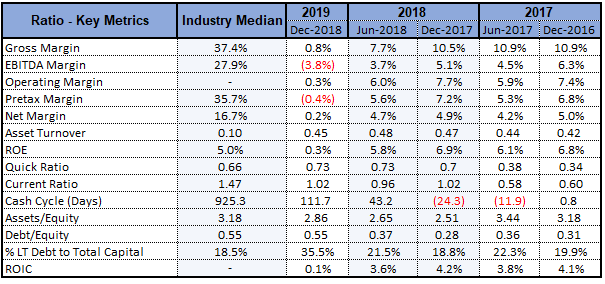

LLC Possessing Decent Position In Key Margins: The key financial ratios of Lendlease Group had witnessed improvement on the YoY basis, which builds the confidence in its operational capabilities. In FY 2018, its net margin stood at 4.8%, which implies a rise of 0.2% on the YoY basis that reflects the company’s capability to convert its top line into the bottom line. Also, the company’s operating margin in FY 2018 stood at 6.9%, which shows a rise of 0.3% on the YoY that reflects its cost-effective capabilities in carrying out the operations. However, in 1H FY 2019, its net margin and operating margin stood at 0.2% and 0.3%, respectively.

Key Metrics (Source: Thomson Reuters)

The company possesses decent liquidity levels as its current ratio stood at 1.02x, which reflects a marginal rise of 0.2% on the YoY basis, thus, it looks like the company can comfortably meet its short-term obligations. Coming to the leverage ratios, the company’s Assets/Equity ratio stood at 2.86x, which is lower than the industry median of 3.18x, thus, it can be assumed that the company is less dependent on debt when it comes to funding its assets. Also, its Debt/Equity ratio stood at 0.55x, which is in line with the industry median.

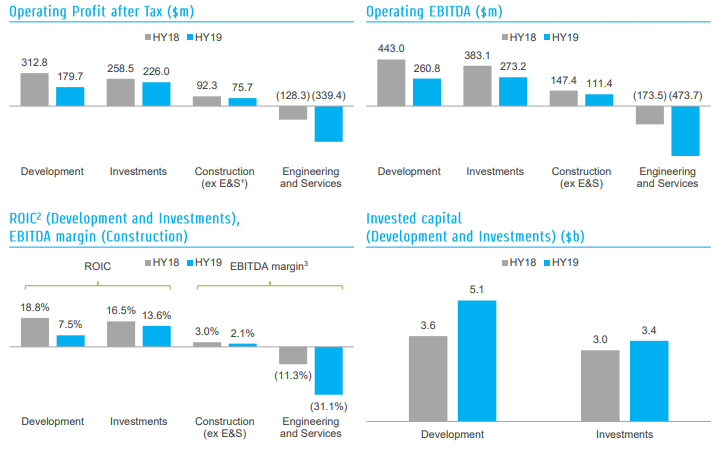

Despite Certain Challenges, LLC Converted Origination Opportunities In Global Gateway Cities: Lendlease Group’s profit after tax amounted to $15.7 million for the period ended 31 December 2018 while the earnings per security (EPS) amounted to 2.8 cents. Its return on equity stood at 0.5%, and the distribution per security amounted to 12 cents. The company’s EBITDA amounted to $83.1 million and was impacted by the result for Engineering and Services business. This business included $500 million of expected losses from the underperforming projects. The Investments segment had continued to outperform, and Development segment had delivered a solid result, although Development earnings are expected to be skewed towards the second half of the financial year. The company stated that Building businesses in each of the regions had delivered solid performance.

Segment Financial Metrics (Source: Company Reports)

The company stated that the recurring earnings had supported the performance of the Investments segment, although the earnings were lower than in the prior corresponding period.

Dealing with Class Action: In the release dated April 18, 2019, Lendlease had been served with representative proceeding filed in Supreme Court of New South Wales, which names Lendlease Corporation Limited and Lendlease Responsible Entity Limited as responsible entity of Lendlease Trust as defendants. The proceeding has been filed by Maurice Blackburn and it is said to be brought on the behalf of the securityholders who acquired an interest in Lendlease’s stapled securities or American Depositary Receipts in period November 17, 2017 to November 8, 2018. However, Lendlease had denied any liability, and it would be vigorously defending the proceeding.

LLC Conducted Comprehensive Strategic Review: Lendlease Group had stated that a comprehensive strategic review determined that the Engineering and Services happen to be a non-core segment and is no longer a required part of the company’s strategy. In order to maximise the securityholder value over the long term, LLC would be focusing on proven integrated capabilities throughout development, construction, and investments. Therefore, Engineering and Services business would be reported as non-core in FY19 results and beyond. The company also added that alternatives for business are being considered.

After the review, it was concluded that it is in best interests of clients, employees as well as securityholders to consider the alternatives that would allow both Engineering and Services business and Lendlease Group to focus towards core competitive advantages. In order to allow Engineering and Services to continue to participate in transport engineering sector while the alternatives are being considered, the company is implementing a lower risk profile business strategy. The company stated that this strategy includes operational improvements and stronger focus towards alliance style partnerships where the risk is more appropriately shared with the project partners. However, the company happens to be in a robust financial position, which is having a gearing ratio at mid-point of the 10%-20% target range and $2.1 billion of the available liquidity even though the Engineering underperformed.

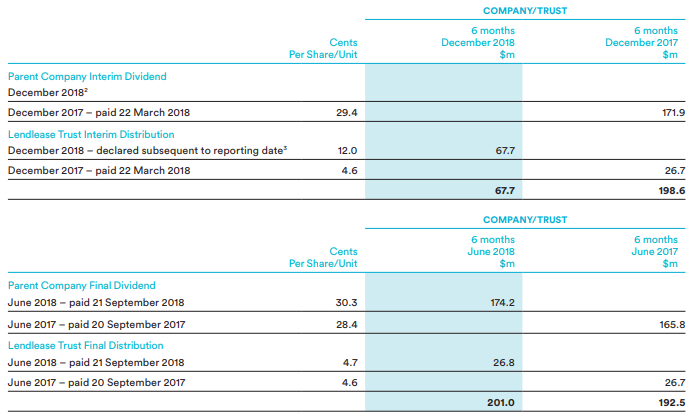

Interim Distribution Paid by LLT: The interim distribution is comprised of trust distribution amounting to 12.0 cents per unit which have been paid by Lendlease Trust (LLT), which is a subsidiary of Lendlease Group. The unfranked interim distribution amounting to $67.7 million had been approved by Directors. The company has been targeting the dividend pay-out ratio in the range of 40%-60%.

Dividends/Distributions (Source: Company Reports)

As per ASX, the company is having an annual dividend yield of 3.54% which can be considered at reasonable levels as there were certain challenges faced by the company. The maintenance of an optimal capital structure, which is a core element of Portfolio Management Framework, is crucial in maximising the securityholder value, which might attract the attention of market players. As a part of a disciplined approach towards managing the capital, there was a completion of an on-market buyback with $352 million of securities acquired.

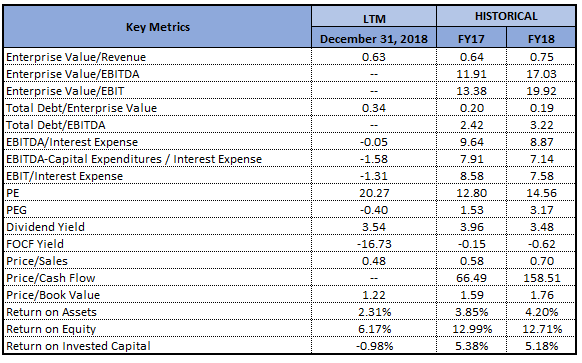

Key Valuation Metrics (Source: Thomson Reuters)

What To Expect From Lendlease Group: Even though Lendlease Group witnessed a challenging period, the competitive advantage of the integrated business model makes the company well positioned for the growth in the future. The company stated that earnings visibility happens to be decent as there is a growing pipeline, diversified by the geography and sector, throughout Development and Investments segments. The development pipeline, which amounted to $74.5 billion had witnessed the significant growth with the company’s focus towards urbanisation in targeted gateway cities. The origination focus has centred on the international operations and the last calendar year was dominated by the new projects which have been secured in Europe.

The company’s funds under management witnessed a rise of 20% on the prior corresponding period and stood at $34.1 billion. The development pipeline helps future growth potential. Together with the investment positions amounting to $3.6 billion, the Investments segment of the company is well placed to deliver a solid base of recurring earnings.

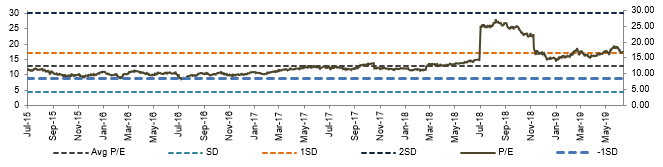

Historical P/E Band (Source: Company Reports)

Stock Recommendation: The stock of Lendlease Group has delivered the return of 14.58% in the span of previous six months while, in the time frame of past three months, the return delivered by the stock stood at 6.92% which can be considered at respectable levels. The decision that Engineering and Services are non-core had been made so that the securityholder value can be maximised over the long term by focusing on the proven integrated capabilities across Development, Construction and Investments.

Moving forward, the company would be placing greater emphasis on the urbanisation as well as on leveraging the competitive advantage of the integrated model. The company’s track record of delivering large scale urbanisation projects gives superior outcomes for the communities, capital partners and the securityholders. The increasing focus towards Development and Investments segments and continued success with regards to securing the urbanisation projects in gateway cities gives a strong platform to provide the enhanced risk-adjusted returns to the securityholders. Hence, keeping the view of a decent outlook in the business along with mixed challenges, we have valued the stock based on 5-year average P/E multiple of 12.9x to FY20E consensus EPS of $1.21 and arrived at the target price of around $15.7, which is offering a lower double-digit upside potential (in %). Given the backdrop of aforesaid parameters and current trading level, we give a “Buy” rating on the stock at the current market price of A$12.990 per share (down 2.184% on 13 June 2019).

.png)

LLC Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...