-

-

Company Description - Lend Lease Corporation Limited (Lend Lease) is an international property and infrastructure company. The Company’s services include construction and infrastructure, development management, asset and property management, building, engineering, infrastructure development, investment management, construction, project management and other services. The Company’s construction and infrastructure services include funding and managing projects and properties, through to the design, development and construction of state of the art precincts, buildings and infrastructure assets including maintenance. Development management includes providing workplace solutions, constructing leading-edge commercial buildings and managing complex refurbishments and tenancy fit-outs for clients around the world. Asset and property management offers facilities management for public institutions such as schools, hospitals in the United Kingdom and military housing communities in the United States.

-

-

-

-

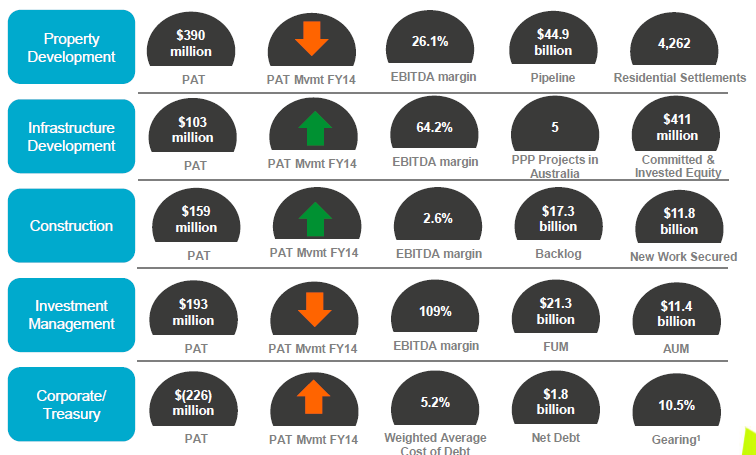

Strong Pipeline: Lend Lease Group (ASX: LLC) profit after tax fell by 25% yoy to $618.6 million in the fiscal year of 2015 impacted by the lower property development and investment management. LLC’s EBITDA also declined by 19% yoy to $967.0 million while the earnings per stapled security decreased by 25% yoy to 106.8 cents during the period. On the other hand, Moody's commented that the group’s results was in line with the estimations and Moody’s also maintained its Baa3 long-term issuer rating. LLC projects its development pipeline end value rose by 19% yoy to $44.9 billion and achieved a record year for residential settlements of 4,262, which is an increase by 24% against prior corresponding period. Lend Lease Group’s funds under management improved by 31% yoy to $21.3 billion, and also raised over $2.1 billion of third party capital over the twelve months ended on June 30 2015. Construction backlog revenue increased by 7% to $17.3 billion as compared to the corresponding period of last year. Moreover, LLC won over $11.8 billion worth of new work construction which is a rise of 16% yoy against last fiscal year. Meanwhile, LLC declared a final distribution of 27.0 cents per security (wherein the dividend component is franked to 25%) resulting in the total year distribution to 54.0 cents per security.

Strong Pipeline: Lend Lease Group (ASX: LLC) profit after tax fell by 25% yoy to $618.6 million in the fiscal year of 2015 impacted by the lower property development and investment management. LLC’s EBITDA also declined by 19% yoy to $967.0 million while the earnings per stapled security decreased by 25% yoy to 106.8 cents during the period. On the other hand, Moody's commented that the group’s results was in line with the estimations and Moody’s also maintained its Baa3 long-term issuer rating. LLC projects its development pipeline end value rose by 19% yoy to $44.9 billion and achieved a record year for residential settlements of 4,262, which is an increase by 24% against prior corresponding period. Lend Lease Group’s funds under management improved by 31% yoy to $21.3 billion, and also raised over $2.1 billion of third party capital over the twelve months ended on June 30 2015. Construction backlog revenue increased by 7% to $17.3 billion as compared to the corresponding period of last year. Moreover, LLC won over $11.8 billion worth of new work construction which is a rise of 16% yoy against last fiscal year. Meanwhile, LLC declared a final distribution of 27.0 cents per security (wherein the dividend component is franked to 25%) resulting in the total year distribution to 54.0 cents per security.

Segment Highlights (Source: Company Reports)

Segment Highlights (Source: Company Reports)

-

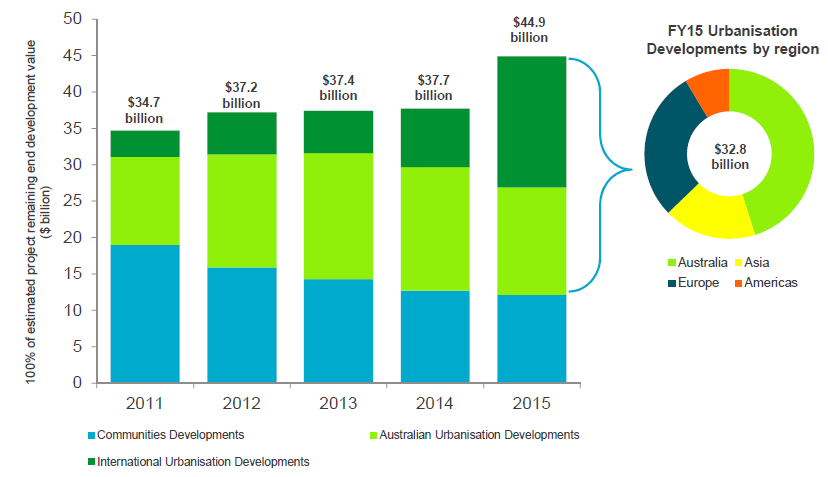

Focus on Urban Projects: Lend Lease Group’s portfolio of main urban regeneration projects had been witnessing a constant growth. The group achieved over $8 billion of major projects across Asia and the Americas over the twelve months ended on June 30 2015. Lend Lease began to focus on urban areas since fiscal year of 2009, and accordingly developed a strong backlog of zoned apartment projects. Subsequently, the group built a backlog of over 18,000 apartments across all regions wherein most of them are at main urban regeneration developments. Moreover, total gross value of apartment pre sales improved to over $4.7 billion during the fiscal year of 2015, from $0.4 billion. The group’s better delivery risk management efforts resulted in a pre-sales of more than 50% prior to starting of construction. As per the backlog for construction, total revenue increased by 3% yoy to $9.9 billion during FY15, boosted by the new work secured revenue worth of $6.5 billion during the period. The group estimates the realization of engineering backlog revenue to profit in the coming 18 to 24 months, and would have an impact of 20% project completion profit recognition edge. But, the withdrawal of the East West Link contract during April 2015, which the group initially estimated to bring engineering earnings during fiscal year of 2016 might lead to a more skew in its backlog revenue. Meanwhile, LLC estimates to maintain its EBITDA margin range in Australia less than the 4.0% to 5.0% range, impacted by the lower engineering contribution in FY16. Moreover, the group had realigned expense base in Engineering. LLC won over $630 million worth of Gateway Upgrade North project in Queensland quite recently, which is not reflected in engineering backlog revenue. Lend Lease had also been witnessing a major growth in production capital from last three years and have over $2.2 billion worth of capital employed in production as at June 30 2015, which is an increase of 46% yoy over the previous twelve months. LLC estimates a peak production by fiscal year of 2017.

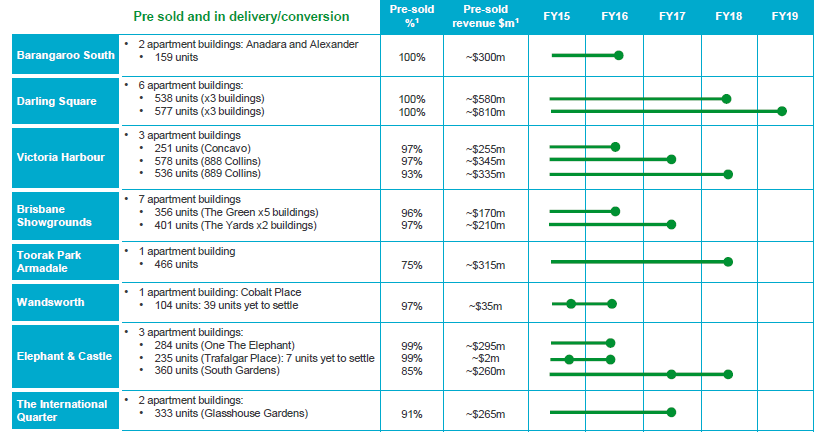

Ongoing urban regeneration projects (Source: Company Reports)

Ongoing urban regeneration projects (Source: Company Reports)

-

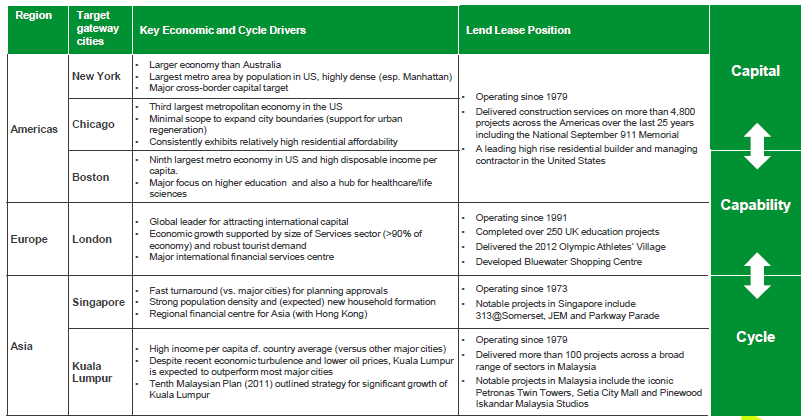

Delivered solid performance in Americas: Lend Lease Group’s Americas segment delivered solid growth during the fiscal year, wherein the region’s EBITDA improved by 21% yoy to $155 million in FY15, while profit after tax improved by 14% yoy to $90 million. Moreover, LLC’s America region has a solid property development pipeline of over $2.8 billion. The region’s Construction backlog revenue rose 3% yoy to $5.5 billion, while won new Construction new work worth of $3.2 billion in FY15, which is an increase of 17% yoy as compared to pcp. Lend lease had been developing solid US development operations and intends to invest over $200 million to $300 million range worth of capital on new projects. The group even won new development opportunities in the Americas region which are targeted at major cities like River South, Chicago; Fifth Avenue, New York; and Clippership, Boston. The overall projects maximum end development value is $2.8 billion.

International regions contribution to Lend Lease (Source: Company Reports)

International regions contribution to Lend Lease (Source: Company Reports)

-

Major pipeline across Asia and Europe as well: With regards to the Europe region’s highlights, the region’s EBITDA plunged by 78% yoy to $130 million in FY15 as the segment’s FY14 performance for Europe consisted profit on sale of Lend Lease’s interest in the Bluewater Shopping Centre in Kent, UK. Accordingly, the region’s profit after tax fell 75% yoy to $112 million. But, property development pipeline for Europe improved by 16% yoy to $9.4 billion while the region’s Pre sold revenue surged by 51% yoy to $1.3 billion during the period. LLC Europe’s Construction backlog revenue increased by 36% yoy to $1.5 billion in FY15 while the regions funds under management rose by 22% yoy to $2.2 billion. Meanwhile. LLCs’ Elephant & Castle project at London delivered first apartments at Trafalgar Place (circa 230 units) before the schedule. The group launched West Grove which is the major release at Elephant Park, and already 48% were pre-sold. Over 25% of affordable housing is estimated to be delivered across the project. As the per The International Quarter (joint venture with LCR), LLC intends to deliver first two commercial office buildings totaling 780,000 square feet and even signed agreements for lease with transport for London and Financial Conduct Authority. The buildings are estimated to be delivered by 2018 while Glasshouse Gardens might be finished in 2017 (333 apartments). As per the Asian regional highlights, the region’s EBITDA decreased by 58% yoy to $39 million in FY15, while profit after tax fell 77% yoy to $17 million. The region’s property development pipeline reached $5.8 billion while the Funds under management surged by 47% yoy to $5.3 billion. LLC won 60% joint venture stake at the TRX Lifestyle Quarter, Kuala Lumpur, which is over $2.8 billion end development value. Lend Lease also entered into 30% JV stake in Paya Lebar Central, Singapore which is a $3.0 billion end development value.

-

LLC Daily Chart (Source - Thomson Reuters)

LLC Daily Chart (Source - Thomson Reuters)

-

Guidance: Lend lease estimates its residential markets to witness a decent growth for both Australia as well as UK markets. The group expects over $5.2 billion of pre-sold residential revenue across communities and apartments, which is an increase of 109%. LLC also estimates to witness a solid residential settlements, which is an increase by 24% yoy for the fiscal year of 2016. Over 25 major apartment buildings and 5 commercial buildings would be delivered in the coming months. Meanwhile, Lend Lease estimates that the Construction markets would remain competitive while the ongoing weakness in engineering revenue were offset by solid building revenues (including internal workbook). International markets would also contribute to the group’s growth opportunities.

Solid Pipeline (Source: Company Reports)

Solid Pipeline (Source: Company Reports)

-

Stock Performance: Lend Lease Group (ASX:LLC) has corrected over 18% in the last three months, given the challenging marketing conditions and investor’s concerns on the oversupply of new properties especially in the Sydney markets coupled with rising property prices which might affect consumers affordability. On the other hand, Lend lease has built a solid backlog and presales revenue. International regions performance especially Americas and London would also continue to contribute to the LLC’s performance. The recent correction in the stock also placed LLC at attractive investment opportunity, with the stock trading relatively cheaper at a P/E of 11.23x. Lend Lease also has a decent dividend yield of 4.3%. We remain bullish on the firm, and recommend investors to “BUY” the stock at the current levels of $12.90.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...