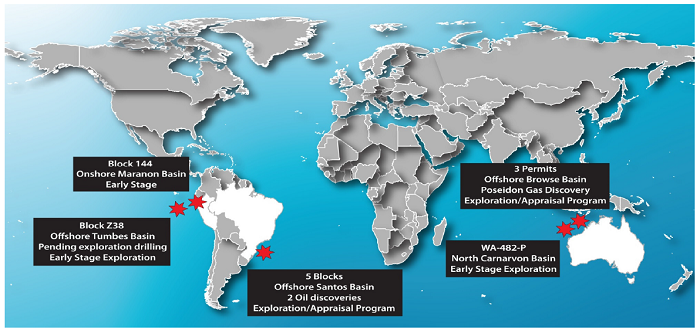

Company Overview - Karoon Gas Australia Ltd (Karoon Gas) is an Australia-based exploration company. The Company is principally engaged in the hydrocarbon exploration and evaluation in Australia, Brazil and Peru. The Company operates in three segments: Australia, Brazil and Peru exploration. The Company’s Australia segment is involved in the exploration and evaluation of hydrocarbons in four offshore permit areas: WA-314-P, WA-315-P, WA-398-P and WA-482-P; The Company in its Brazil segment is involved in the exploration and evaluation of hydrocarbons in five offshore blocks including Block S-M-1037, Block S-M-1101, Block S-M-1102, Block S-M-1165 and Block S-M-1166. The Company under its Peru exploration segment is involved in the exploration and evaluation of hydrocarbons in two blocks in Peru, including Block 144 (onshore) and Block Z-38 (offshore).

Analysis – High impact but costly funding drilling programs in Western Australia and later this year in Brazil pose funding challenges. Processes are underway to free up cash but are uncertain. The risks are high of a funding crunch. Lacking production, KAR is dependent on equity capital and asset sales to fund ongoing exploration. Farm out processes have been underway with respect to all of KAR’s acreage since December quarter 2012 and as early as 2010 for Peru. It has longer to conclude deals than we had originally expected and the outcome of the processes remain uncertain. Funds could be exhausted by mid-year given the commitments for the Browse basin program and later this year Brazil. There is urgency to conclude a farm out asset sale or raise equity and until resolved we expected the share price to reflect funding risks.

We view KAR’s geology as attractive, evidenced by oil and gas discovered to date. The recent dry hole at the “GRACE” location offshore Western Australia does not detract from thee value of discovered resources at Poseidon or Brazil Our base case assumes successful farm outs or asset sales to mandate this value. We believe that KAR is exposed to world class exploration assets offshore Western Australia, Brazil and possibly Peru. It has excellent exploration track record to date. Currently there is no revenue stream so KAR must fund drilling commitments from cash, external funds sale of acreage. Inability to sell assets, farm down or raise equity on a timely manner increase risk of forfeiture of assets. Some of the key value drivers in regards to KAR would be:-

-

Exploration and appraisal success on discovered resources

-

Execution of trade sale deals in the form of farm outs or outright sale of permits for cash would provide relevant look through valuations and ease funding obligations.

KAR’s 5 year low share price does not reflect lack of exploration success but rather funding pressures. Without production revenue, KAR may need to raise capital or sell assets to stay liquid and between these events the funding concerns mount. At this time we asses it as acute due to a combination of higher exploration spending in the past year and spilling into 2014, longer than expected duration to conclude farm outs and CAPEX commitments this year which we assume will exhaust KAR’s existing cash resources. By mid-year we believe that KAR will have exhausted its cash reserves unless there is a fresh injection of funds. The obvious solutions are to sell or farm down assets or raise equity but if done cheaply then the value implications are negative and the question of funding beyond 2014 unanswered.

KAR’s exploration activities are ongoing in three separate regions, namely offshore Brazil in the Santos basin, offshore WA in the Browse basin and Offshore Peru in the Tumbes basin. Geologically offshore WA and Brazil are attractive regions. They are characterized as regions where Energy and Petroleum companies are active and where large discoveries have been made. They also happen to be in offshore marine environments where drilling costs are very high and where time line from acreage award through discovery to development can span several years. KAR has no production and we don’t anticipate any until later this decade on the presumption that at least one of the two oil discoveries offshore Brazil can be developed by then. Until such time KAR will be dependent on equity raisings and additional farm downs or even outright asset sales for cash in order to meet exploration, appraisal and development drilling costs.

KAR Assets (Source – Company Reports)

KAR Assets (Source – Company Reports)

At December 31, KAR’s cash reserves were $180m, and expenditure this quarter is expected to be $100m of which $95.9m is for exploration drilling including the residual costs for the recently completed dry-hole at Grace. Funding of the remaining wells in the current drilling program offshore Western Australia in the Browse Basin, which is phase 2 of greater Poseidon, Poseidon North and one other well. We estimate that each of these wells will cost around $100m gross, with KAR’s share in aggregate $80m. Following a one month break for scheduled maintenance Poseidon North in March on the drilling rig, drilling is expected to begin in March.

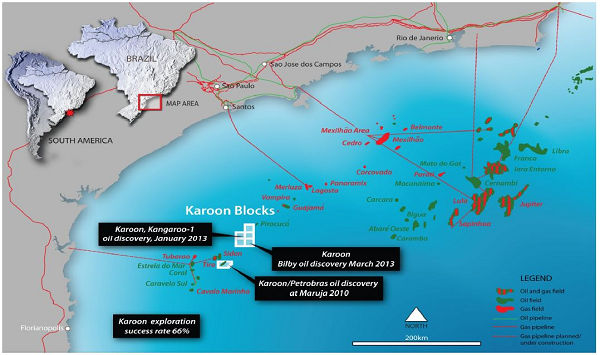

Drilling commitments agreed with the Brazilian authorities for 2014 and 2015 work programs on the 5 Santos basin blocks. In 2013 there were 3 wells drilled for 2 discoveries fully funded by Pacific Rubiales. That carry has been exhausted and from here KAR is fully exposed to its 65% share of future exploration and appraisal costs. The committed work program for 2014 is two wells for an appraisal well on the Kangaroo oil discovery and an exploration well on the Kangaroo West prospect, in addition to seismic re processing. Based on the costs of the first 3 wells which the JV partner carried for US$240m, we figure the gross cost of this program is in the order f $130m and Karoon’s funding exposure around US$85m. In the off shore Tumbes block (PERU), KAR’s working interest is 75%. To retain the permit, the JV are required to drill 2 wells and begin drilling before mid 2015 in order to retain the licenses.

KAR Brazil Assets (Source – Company Reports)

KAR Brazil Assets (Source – Company Reports)

KAR has a 65% working interest in 5 blocks in the Santos basin in JV with Pacific Rubiale and a 20% interest in a Petrobras operated small oil discovery in Maruja. In summary Pacific Rubiale free carried KAR through a 3 well US$240 drilling program which commenced in January 2013. All 3 wells encountered oil with the results from Kangaroo-1 the most encouraging.

Daily Chart Karoon Gas (Source - Thomson Reuters)

Daily Chart Karoon Gas (Source - Thomson Reuters)

In the browse basin offshore WA, KAR (40%) and partner ConocoPhillips COP (60%) have completed 3 of the planned 5 wells in phase2 drilling on the greater Poseidon structure which occupies permits WA315 and WA398. The first 3 wells in the phase 2 campaign, Boreas, Zephrys and Proteus all discovered gas. The fourth and most recent well in adjacent permit WA314 (KAR 90%, COP 10%) was Grace#1. This well failed to find reservoir objectives but as an independent structure this result does not impact the results or prospects for Poseidon. Two more wells follow in the current phase of drilling on the Poseidon structure, after a month of scheduled maintenance on the drilling rig. We like the KAR story and would be putting BUY at the current price of $3.11

Disclaimer

Kalkine provides general advice on securities. Kalkine does not provide advice that takes into account your, or anybody else’s investment objectives, financial situation or needs. We strongly suggest that you should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. Employees and/or associates of Kalkine Pty Ltd may hold one or more of the stocks reviewed on this website. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...