In today’s daily we have covered stock research on

Dulux Group (Overvalued/Expensive). To view

3 Undervalued Stocks to Buy click here

S&P 500 was up by 4.46 points or 0.24% to 1892.49 on Thursday. U.S. stocks ended higher on Thursday, led by gains in small-cap stocks while the

Nasdaq advanced on a rally in biotech shares. World stock indexes climbed on Thursday as data showed factory activity picked up in both the United States and China, while U.S. Treasuries prices slipped on the signs of growth in the world's largest economies.

China's factory sector had its best performance in five months in May, while

U.S. factory output growth hit its fastest pace since February 2011, providing support for stocks. In Europe, an unexpected pickup in the service industry was offset by lackluster factory activity, though it was enough to show the euro zone's fragile recovery has some traction. The United States endured a sluggish first quarter, which has given the Federal Reserve some pause, and minutes of its last policy meeting show it is in no rush to raise rates.

S&P 500 Daily Chart (Source – Thomson Reuters)

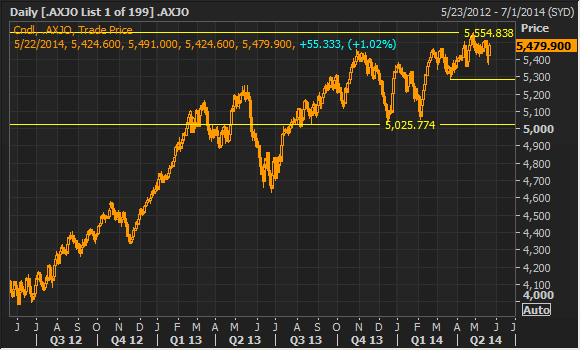

S&P ASX 200was up by 55.3 points or 1.02% on Thursday and closed at 5479.9 points.

Glencore has announced that it will close its Newlands Coal mine in Australia in late 2015.

Qube and

Aurizon have obtained exclusive rights over the development of an intermodal terminal at Moorebank in Sydney.

SealinkTravel Group (SLK) announced that

Commonwealth Bank of Australia and its related bodies corporate have an interest representing 5.24 pct. of total voting power.

Mineral Resources (MIN) announced that

Southeastern Asset Management Inc has an interest representing 5.38 pct. of total voting power.

S&P ASX 200 Daily Chart (Source – Thomson Reuters)

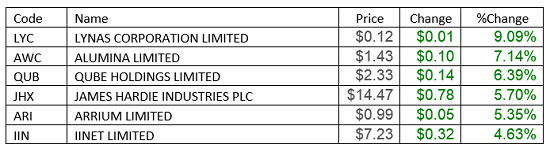

The

top gainers on ASX 200 were:-

Stock of the Day – Dulux Group (DLX)

Stock of the Day – Dulux Group (DLX)

Dulux Group is a manufacturer and marketer of premium branded paint, coatings, adhesives, garden care and other building products to the residential home improvement, commercial and infrastructure markets across Australia and New Zealand with niche positions in Papua New Guinea, China and South East Asia.

While the company has strong market positions and is well managed, we believe the market may be overestimating the company’s leverage to improved new housing activity, which represents just 16% of group sales revenue. The company has a lower share of this segment of the market and it tends to be lower margin.

Source - DLX

We view Dulux Group’s slightly above market 1H14 result to be positive for the company, however the market may be concerned by the 22% reduction in net operating cash flow, the generic outlook commentary and the cautionary comments in relation to the timing of its new housing exposure, the outlook for its commercial and infrastructure markets, and input costs.

DLX Daily Chart (Source - Thomson Reuters)

The heritage Dulux business performed well with earnings growth of 12.5% on revenue growth of 4% with the Alesco businesses generating earnings growth of 7%. While the outlook for most of the company’s key markets is stable to improving the company cautioned that its exposure to new housing activity is just 16% of group sales revenue and that its exposure is at the tail end of construction. The company also cautioned that the outlook for its commercial and infrastructure markets was less positive given the downturn in mining activity. We believe the stock is overvalued at its current price and would review the stock at a later date.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.

Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).

The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.

Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.

The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...