S&P ASX 200was up by 4.3 points or 0.08 %on Thursday and closed at 5638.9 points. BHP Billiton lost 0.3 per cent to $38.03, extending the previous session’s slide. Rio Tinto fell 0.6 per cent to $65.60. Breville was the worst performer, easing 18.6 per cent to $7.10. Origin Energy lifted 4.2 per cent to $14.78 despite full-year underyling net profit slipping. Santos, Iluka, Sims Metal, IOOF, QUBE Holdings, Federation Centres report earnings.

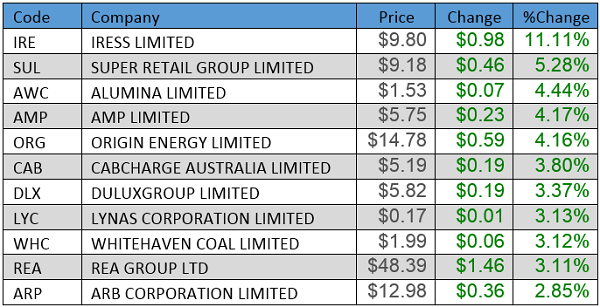

Infomedia Group’s (IFM) Net Profit after Tax (NPAT) grew by 22.0% to $12.3m and sales revenue grew by 17.4% to $57.1m. Heritage Bank’s audited before tax profit of $50.04 million for the year ended 30th June 2014 represented a 5.5% decrease on the previous year. Vale has awarded Worley Parsons an engineering services contract for its Kronau Potash Project. The Australian dollar is trading at US92.98¢. The top performer on ASX 200 was Iress with a rise of 11.11%.

IRESS Daily Chart (Source – Thomson Reuters)

The top gainers on ASX 200 were:-

Stock of the Day – ANZ Bank (ANZ)

ANZ provided a trading update last week for the nine months to 30

th June. While trends across most businesses were solid, global Markets was weaker. We estimate 3Q Global Markets revenue was $450m, compared to an average of $620m for 1Q & 2Q, as lower volatility impacted Trading and Balance Sheet Income. As a result ANZ now expects revenue to be at the lower end of its target range partly offset by cost management.

Share of the world GDP (Source – Company Reports)

ANZ announced cash NPAT of $5.2bn implying $1.7bn of cash NPAT for 3Q14, slightly softer than our expectation of $1.8bn given a softer quarter of global markets revenue. ANZ commented that it expects FX adjusted earnings for FY14 to be in line with guidance with revenue growth at the lower end of the 4 to 5% guidance range but costs well controlled. ANZ’s cost guidance is for 2% growth in FY14.

ANZ revenue pools forecast 2017 (Source – Company Reports)

ANZ continues to see a trend improvement in non-performing loans, with non-performing loans down 6 basis points to 105 basis points of loans in the quarter. Impaired loans drove the improvement down 7 basis points to 67 basis points. 90 day arrears have continued to see a modest increase over the last few quarters. Specific provision cover of impaired assets increased 60 basis points to 39.4 % on a regulatory reported basis.

ANZ Daily Chart (Source – Thomson Reuters)

Whilst the trading update was 2% softer than consensus, with revenue weakness bolstered by lower bad debts, we remain comfortable with ANZ given: 1) The miss appears to be dominated by relatively volatile item markets income. 2) ANZ is still confirming FY14 guidance. Positively capital generation over 3Q14 was relatively strong. We put a HOLD recommendation on the stock at the current price.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.

Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).

The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.

Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.

The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...