In today’s daily we have covered stock research on

Westpac. To view

3 Media Stocks with 6%+ Dividends click here

S&P 500 was down by 8.92 points or 0.47% to 1888.53 on Wednesday. U.S. stocks fell on Wednesday, with the Dow and S&P 500 easing back from recent record highs, as small caps resumed their sell-off and consumer discretionary shares lagged. Decliners in the Dow included

Wal-Mart which also experienced an unusual mini "flash crash." In less than one second, the stock tumbled from $78.66 to $78.06 but rebounded back within a minute.

Groupon Inc. sank 4.4 percent to lead the Dow Jones Internet Index lower by 1.2 percent.

Fossil Group Inc. fell 10 percent after the maker of watches and accessories forecast earnings that trailed analysts’ estimates.

IBM slid 1.8 percent to $188.72 for the steepest slide in the Dow.

S&P 500 Daily Chart (Source – Thomson Reuters)

S&P ASX 200was down by 1.7 points or 0.03% on Wednesday and closed at 5496.5 points.

CBA shares closed up 1.2% at $80.89. The stock is up 12% from February.

BHP Billiton is considering sale of its Nickel West assets in Western Australia.

GPT Group announced ownership interest of

UBS AG representing 9.05% of the total voting power.

AGL Energy’s managing director and CEO, Michael Fraser is to retire by June 30, 2015.

Telstra completes the sale of its Hong Kong based mobiles business CSL to HKT Limited. Sale proceeds equate to $1.99 bln for Telstra’s 76.4 pct interest in CSL after preliminary completion adjustments.

S&P ASX 200 Daily Chart (Source – Thomson Reuters)

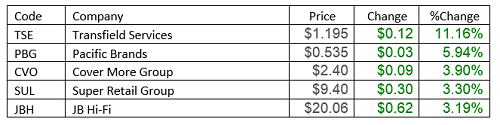

The

top gainers on ASX 200 were:-

Stock of the Day – Westpac (WBC)

Stock of the Day – Westpac (WBC)

Westpac Banking corporations’ impressive cash profit of AUD 3.8 billion for first half fiscal 2014 increased 8% on first half fiscal 2013 and exceeded consensus by 4%. The result was hard to fault and confirms our positive view on the bank’s ability to produce strong profits despite operational and economic challenges. Westpac benefited from improving revenue growth (up 5%) and a further sharp improvement in bad debts (down 22%) resulting in earnings per share up 7% and a 5% increase in fully franked dividends.

Improved asset quality, solid balance sheet growth and disciplined cost control again featured. Despite the strong profit and high quality result, no special dividend was declared but a special dividend is likely with the full year result later this year. Costs increased more than expected, up 6% on the first half of 2013. As expected net interest margins deteriorated compared with a year ago but are broadly in line with the second half of 2013.

.png)

Source - WBC

Solid lending growth (up 8% on March 2013) was spread across the Australian and New Zealand loan Portfolios. The most surprising outcome was Westpac’s peer leading credit quality with the 22% decline in bad debt expense to AUD 341 million. The very low bad debt impairment is just 0.15% of average loans outstanding. CBA is Westpac’s closest peer with bad debt to average loans of 0.16% in its latest half year, while ANZ Bank is at 0.22%.

.png)

WBC Daily Chart (Source - Thomson Reuters)

Impairments at these historic lows are unsustainable and our medium term forecast of 20 basis points for Westpac is retained. Australian housing loans rose 5% despite increasing number of customers taking advantage of low interest rates and repaying home loans faster. The continued improvement in asset quality bodes well for future earnings. Earnings and dividends are likely to grow at about 7% per annum during our five year forecast period based on moderate credit growth, steady net interest margins, improving fee and commission income, and tight cost control. We gave the buy on WBC at $30.87 on 03/02/2014 (

KIR – 102), we recommend a HOLD on the stock at the current price of $34.20.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.

Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).

The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.

Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.

The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...