Kalkine has a fully transformed New Avatar.

This report is an updated version of the report published on 14 August 2025 at 11:22 AM AEST.

Company Overview

Company Overview: HMC Capital Limited (ASX: HMC) is an ASX-listed diversified alternative asset manager specialising in high conviction and scalable real asset strategies on behalf of individuals, large institutions, and super funds. Select Harvests Limited (ASX: SHV) is an ASX listed producer of almond products for retail and industrial markets. Kalkine’s Sector Report covers the Investment Summary, Sector Overview & Supporting Catalysts, Data Insights & Analysis, Financial Metrics, Financial Commentary, Risks, Outlook, Technical Analysis along with the Valuation, Target Price, and Recommendation on selected stocks.

Investment Summary

Sector Overview and Supporting Drivers

Australia’s financial sector is a cornerstone of the economy, encompassing major banks, insurers, asset managers, and fintech firms. Dominated by the “Big Four” banks, it plays a critical role in credit provision, wealth management, and capital markets. The sector benefits from a resilient regulatory framework and strong household wealth, though it remains sensitive to interest rate shifts, housing market trends, and global economic conditions. Recent rate cuts and stable employment support lending growth, while technology adoption and fintech innovation enhance efficiency and customer engagement. Ongoing housing demand, infrastructure investment, and foreign capital inflows are key catalysts for future expansion.

Australia’s consumer sector is a key driver of the economy, covering both essential and discretionary goods and services. Its performance is shaped by household spending, population growth, and evolving consumer habits. Spanning industries like retail, food and beverages, healthcare, travel, and e-commerce, the sector is influenced by macro factors such as interest rates, inflation, and wage trends. Digital innovation and sustainability are transforming operations, while cost pressures, supply chain challenges, and shifting preferences present ongoing hurdles. Despite these headwinds, the sector remains vibrant, with growth potential closely linked to economic momentum and changing lifestyle patterns.

Sector Catalysts

Index Performance

Investment theme and stocks under discussion (HMC, SHV)

After understanding the sectors, let us now look at two companies from the Financial and Consumer sectors listed on the ASX. The price potential of the companies under discussion have been analysed based on Price/Book Value and Price/Cash Flow Per Share based relative valuation methods.

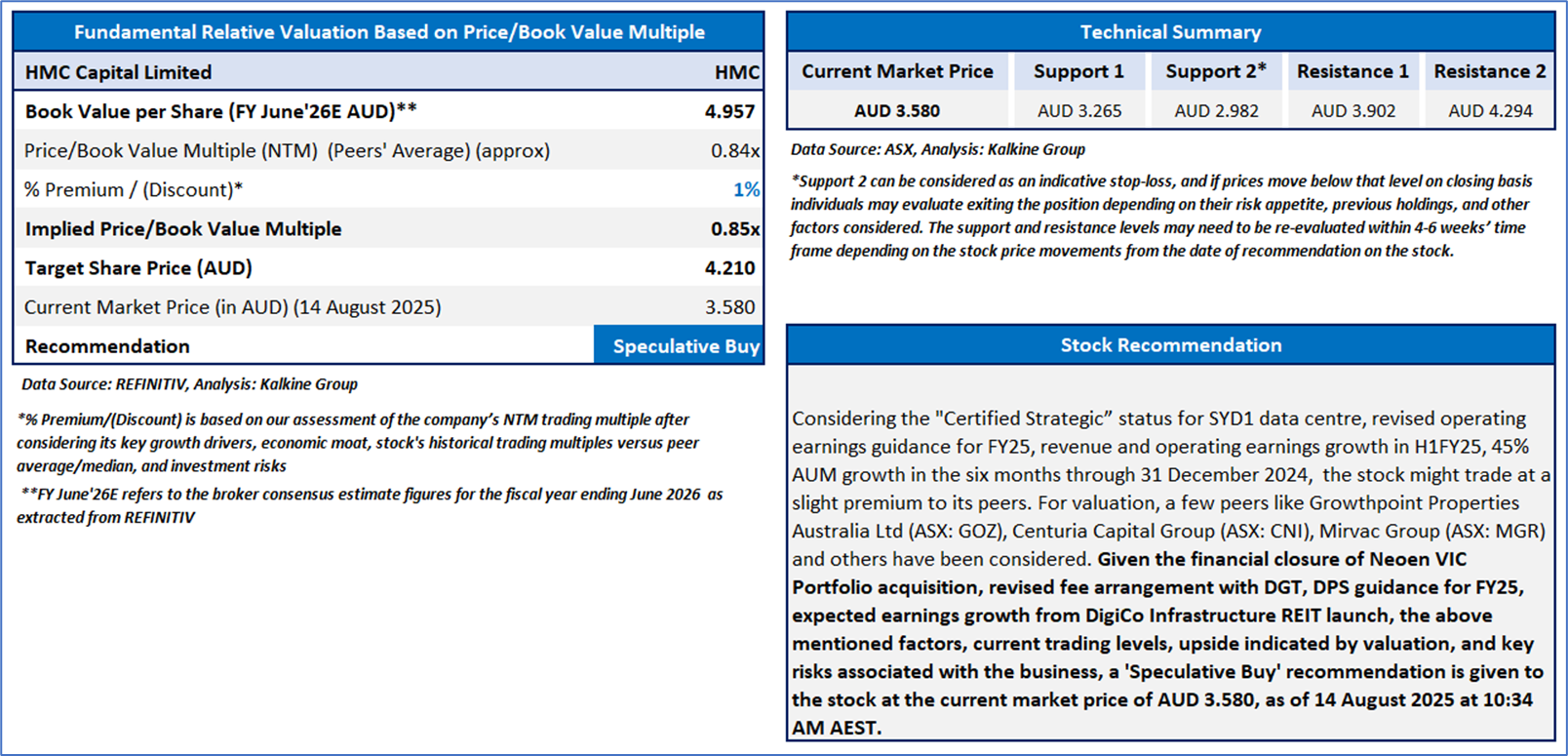

1.ASX: HMC (HMC Capital Limited)

(Recommendation: ‘Speculative Buy’ at AUD 3.58; Potential Upside: Low Double-Digit; MCap: AUD 1.47bn)

HMC is an ASX-listed diversified alternative asset manager specialising in high conviction and scalable real asset strategies on behalf of individuals, large institutions, and super funds.

Insights & Outlook

6-month ended December 2024 Financial (H1FY25) Performance: HMC's total revenue surged 202.6% to AUD 272.3mn in H1FY25, driven by a 179% surge in investment income and 209% annual jump in fund management fees. Its assets under management (AUM) expanded by 45% from June 2024, supported by active capital deployment across HMC’s Digital Infrastructure, Energy Transition, and Private Credit divisions. Its operating earnings post tax rose to AUD 140.5mn vs AUD 57.8mn, a 143.1% annual jump. HMC will report FY25 earnings on 19 August.

Outlook: On 11 August 2025, HMC announced that SYD1 data centre, a part of DigiCo Infrastructure REIT, has received “Certified Strategic” status from the Department of Home Affairs, boosting asset value. With planned capacity expansions and rising AI-driven demand, HMC expects leasing and earnings growth from DGT. HMC has revised its FY25 annualised operating EPS (pre-tax) to 66 cents, down from 70 cents previously forecast in April, due to fair value movements in HMCCP and financial assets during that month. However, its FY25 dividend guidance remains steady at 12 cents per share. HMC management anticipates the real estate division will contribute over AUD 2.5bn in additional AUM.

Key Risks: Market and Economic Risk, Capital Raising and Fund Performance Risk, Execution and Strategic Risk, Regulatory and Compliance Risk

The stock has witnessed a decline of ~3.63% in last one month, and over the past six months, it has fallen by ~63.16%. The stock has a 52-week low and 52-week high of AUD 3.46 and AUD 13.160, respectively and is currently trading near the 52-week-low level. HMC was last covered in a report dated ‘15 July 2025’.

2. ASX: SHV (Select Harvests Limited)

(Recommendation: ‘Speculative Buy’ at AUD 3.73; Potential Upside: Low Double-Digit; MCap: AUD 527.21mn)

SHV is an ASX listed producer of almond products for retail and industrial markets.

Insights & Outlook

6-month ended March 2025 Financial (H1FY25) Performance: SHV's revenue saw 54.1% annual jump to AUD 104.5mn in H1FY25, supported by higher realised price for almonds. The company reported a net profit of AUD 28.7mn, a positive swing of AUD 31 million from AUD 2.4 million net loss reported in H1FY24, driven by higher revenue and lower finance costs.

Outlook: SHV reaffirmed its 2025 crop forecast mid-point of 25,250 MT, despite USDA’s July forecast of a 3 billion-pound US almond crop, which some industry participants believe is overstated. The USDA report has driven almond spot prices down USD 0.45/lb, but Australian prices remain supported by tariff regimes and potential upside from trade uncertainties. With 75% of the 2025 crop already contracted, only the remaining balance is exposed to price volatility, the company said. Management believes value-add products and consistent sales pacing mitigate risks, while demand is expected to grow 5–7% annually amid flat global supply. Sales, shipping, and balance sheet strength remain on track.

Key Risks: Agricultural and Climate Risks, Water Availability and Pricing, Almond Price Volatility, etc.

The stock has declined by ~5.26% in last one month, and over the past six months, it has corrected by ~21.63%. The stock has a 52-week low and 52-week high of AUD 3.37 and AUD 5.45, respectively and is currently trading below its 52-week high-low average. SHV was last covered in a report dated ‘17 July 2025’.

Markets are trading in a highly volatile zone currently due to certain macro-economic issues and geopolitical tensions prevailing. Therefore, it is prudent to follow a cautious approach while investing.

Note 1: Past performance is neither an Indicator nor a guarantee of future performance.

Note 2: The reference date for all price data, currency, technical indicators, support, and resistance levels is 14 August 2025. The reference data in this report has been partly sourced from REFINITIV.

Note 3: Investment decisions should be made depending on an individual’s appetite for upside potential, risks, holding duration, and any previous holdings. An ‘Exit’ from the stock can be considered if the Target Price mentioned as per the Valuation and or the technical levels provided has been achieved and is subject to the factors discussed above.

Note 4: Kalkine reports are prepared based on the stock prices captured either from REFINITIV or Trading View. Typically, REFINITIV or Trading View may reflect stock prices with a delay which could be a lag of 25-30 minutes. There can be no assurance that future results or events will be consistent with the information provided in the report. The information is subject to change without any prior notice.

Technical Indicators Defined: -

Support: A level at which the stock prices tend to find support if they are falling, and a downtrend may take a pause backed by demand or buying interest. Support 1 refers to the nearby support level for the stock and if the price breaches the level, then Support 2 may act as the crucial support level for the stock.

Resistance: A level at which the stock prices tend to find resistance when they are rising, and an uptrend may take a pause due to profit booking or selling interest. Resistance 1 refers to the nearby resistance level for the stock and if the price surpasses the level, then Resistance 2 may act as the crucial resistance level for the stock.

Stop-loss: It is a level to protect further losses in case of unfavourable movement in the stock prices.

This report (“Report”) has been issued by Kalkine Pty Limited (ABN 34 154 808 312) (Australian financial services licence number 425376) (“Kalkine”) and prepared by Kalkine and its related bodies corporate who are authorised to provide general financial product advice. Kalkine.com.au and its associated pages are published by Kalkine.

Any advice provided in this Report is general advice only and does not take into account your objectives, financial situation or needs. You should therefore consider whether the advice is appropriate for your objectives, financial situation and needs before acting upon it.

There may be a Product Disclosure Statement, Information Memorandum or other offer document (“Offer Document”) for the securities or other financial products referred in this Report. You should obtain a copy of the relevant Offer Document and consider it before making any decision about whether to acquire the security or financial product.

Kalkine strongly recommends that you seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) before acting on any of the general advice in this Report or on the Kalkine website. Not all investments are appropriate for all people.

The information in this Report and on the Kalkine website has been prepared from a wide variety of sources, which Kalkine, to the best of its knowledge and belief, considers accurate. Kalkine has made every effort to ensure the reliability of the information contained in its reports (including this Report), newsletters and websites. All information represents our views at the date of publication and may change without notice.

The information in this Report does not constitute an offer to sell securities or other financial products or a solicitation of an offer to buy securities or other financial products. Our reports contain general recommendations to invest in securities and other financial products. Kalkine is not responsible for, and does not guarantee, the performance of, or returns on, any investments mentioned in this Report.

Kalkine does not issue, sell or deal in any financial products.

This Report may contain information on past performance of particular investments. Past performance is not a reliable indicator of future performance. Returns stated do not take into account transaction costs and taxes. To the extent permitted by law, and excluding any dishonesty or gross negligence by Kalkine, Kalkine disclaims and excludes all liability for any direct, indirect, implied, punitive, special, incidental or other consequential loss or damage arising from the use of or reliance on this Report, the Kalkine website and any information published on the Kalkine website without any warranties or representations by Kalkine to you. To the extent the law prohibits or limits this exclusion, Kalkine limits its liability to the resupply of services.

Please also read our Terms & Conditions and Financial Services Guide for further information. Employees and/or associates of Kalkine and its related entities may hold interests in the securities or other financial products covered in this Report or on the Kalkine website. Any such employees and associates are required to comply with certain, procedures and disclosures as required by law.

Kalkine Media Pty Ltd, an affiliate of Kalkine Pty Ltd, may have received, or be entitled to receive, financial consideration in connection with providing information about certain entity(s) covered on its website including entities covered in this Report.

Copyright 2025 Krish Capital Pty. Ltd. (ABN 61629651510). All Rights Reserved. No part of this report, or its content, may be reproduced in any form without our prior consent.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...