Company Overview: Johnson & Johnson is a holding company, which is engaged in the research and development, manufacture and sale of a range of products in the healthcare field. It operates through three segments: Consumer, Pharmaceutical and Medical Devices. Its primary focus is products related to human health and well-being. The Consumer segment includes a range of products used in the baby care, oral care, skin care, over-the-counter pharmaceutical, women's health and wound care markets. The Pharmaceutical segment is focused on five therapeutic areas, including immunology, infectious diseases, neuroscience, oncology, and cardiovascular and metabolic diseases. The Medical Devices segment includes a range of products used in the orthopedic, surgery, cardiovascular, diabetes care and vision care fields. Its research facilities are located in the United States, Belgium, Brazil, Canada, China, France, Germany, India, Israel, Japan, the Netherlands, Singapore, Switzerland and the United Kingdom.

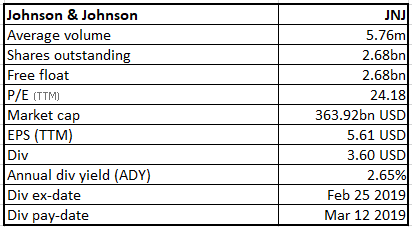

JNJ Details

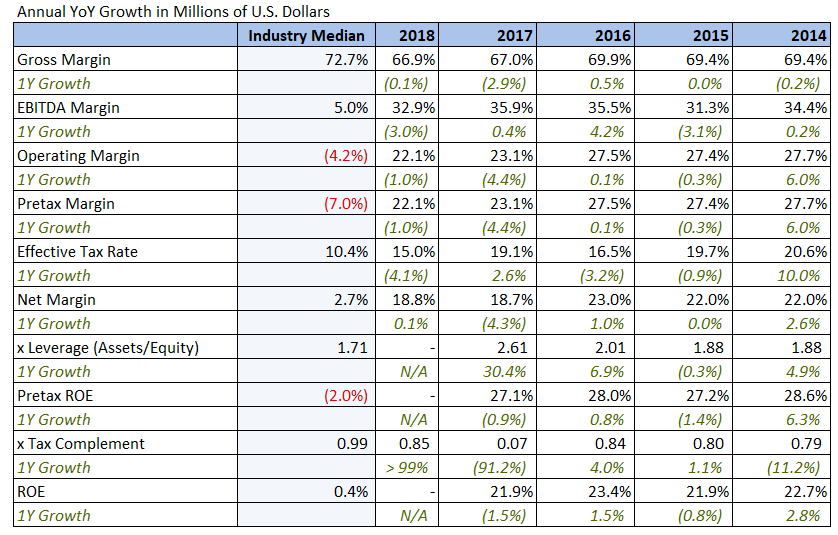

Johnson & Johnson (NYSE: JNJ), a world class healthcare company, is into the research and development, manufacturing and sale of multiple range of personal care hygienic products, pharmaceuticals and surgical equipment. The group has been facing some legal challenges (in the baby powder space), nonetheless, it seems to strive towards growth driven by many strategic moves. The group is now managing the subpoenas from the U.S. Justice Department and the Securities and Exchange Commission in regard to safety of its talc-containing products. On the other hand, it has been able to deliver in terms of financial performance as seen lately. On daily stock price chart, the group has been able to slightly outpace the broader index as at February 20, 2019, and the stock appears to be closer to industry median in terms of forward P/E. The track record on dividends, operating profitability and overall sound business with diverse growth levers across the portfolio are expected to manage the risks emanating from baby powder segment (a reputable one though). If one looks at the margins in the table provided below, JNJ has been delivering performance on a consistent basis, and this is expected to be continued in the long term.

Financial Ratios (Source: Company Reports and Thomson Reuters)

Acquisition of Auris Health, Inc.: JNJ is now focusing to create the next frontier of surgery, through its subsidiary Ethicon, Inc., which has signed a definitive agreement for the acquisition of developer of robotic technologies, Auris Health, Inc. for the total consideration of approximately $3.4 billion in cash. Under the arrangement, an additional contingent payment of up to $ 2.35 billion is to be paid, and this may happen post fulfilling the requisite predetermined milestones. Auris Health was initially focusing on the lung cancer and has the FDA-approved platform, the Monarch Platform, that is currently used in bronchoscopic diagnostic and therapeutic procedures. This acquisition move will help Johnson & Johnson expedite its efforts to penetrate well in robotics space and set the premise for growth into various interventional applications. Further, the Monarch Platform robotic technology is expected to play an important role for JNJ’s Lung Cancer Initiative (LCI). LCI will comprise of developing the differentiated digital solution which will underpin the lung cancer care journey, that starts from diagnosis to early stage intervention, which will help the company to intercept and cure this deadly disease. Meanwhile, the acquisition is subject to antitrust clearance and requisite customary conditions; however, the transaction is expected to be complete by the end of the second quarter of 2019. The details of the transaction are slated to be discussed during the quarterly earnings call scheduled to be held on April 16, 2019.

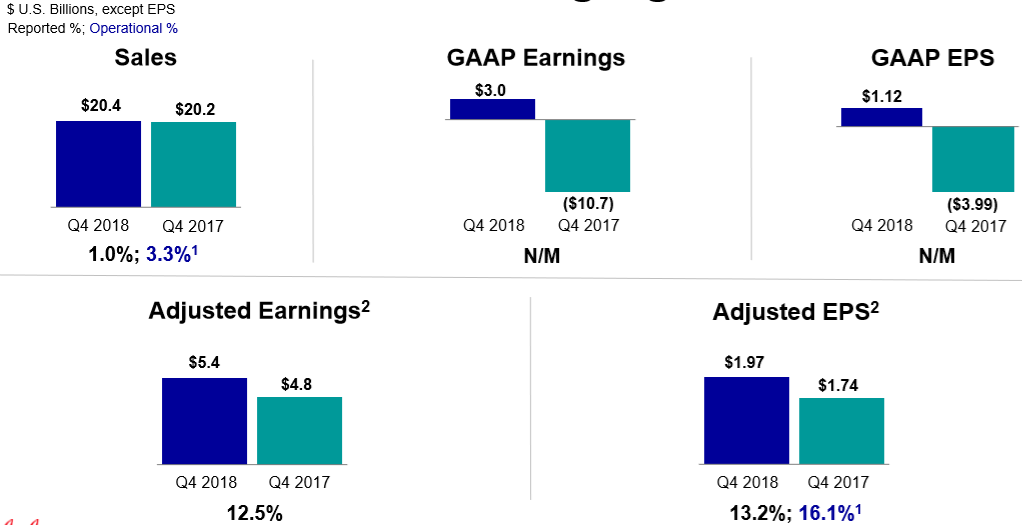

Better than Expected Fourth Quarter 2018 Financial Performance: Johnson & Johnson for the fourth quarter of 2018 has posted better than expected results with adjusted earnings per share of $1.97, beating the market estimates of around $1.95. The adjusted revenue growth of about 1 percent to $20.4 billion has also been above the market estimates of $20.2 billion while full-year sales of $81.6 Billion has been up 6.7%. During the fourth quarter of 2018, the company has posted 1.5% growth in Domestic sales and 0.4% rise in International sales, which shows the operational growth of 5.1% but the negative currency impact of 4.7%. On an adjusted basis, for the fourth quarter of 2018, worldwide sales rose 5.3%, there has been 2.6% rise in domestic sales and 8.3% rise in international sales. The full year adjusted net earnings of $22.3 billion and adjusted diluted earnings per share of $8.18, represented a rise of 11.4% and 12.1%, respectively, over the same period in 2017. On the other hand, company’s litigation expenses moved up and almost doubled in the fourth quarter in view of defending the cases for its talc-based baby powder, which is accused to contain asbestos and cause deadly diseases like mesothelioma, ovarian and other types of cancers. The company made a provision of $1.29 billion for the legal costs during the quarter and this is double the amount of $645 million that was spent in the prior corresponding period. The litigation expenses thus rose by 59% to $1.99 billion for FY18 over the figure of 2017. Meanwhile, the company is facing more than 9,000 cases related with talc, and the company has been denying that its products are dangerous or contain asbestos. The U.S. Food & Drug Administration in a study found that the company’s product does not contain asbestos fibers or structures. Given all of the above, Johnson & Johnson reported a net income of $3.04 billion in the quarter compared to a loss of $10.7 billion in the corresponding period last year.

Fourth Quarter 2018 Financial Performance (Source: Company Reports)

Segment Performance During the Fourth Quarter of 2018 & Full year: During the fourth quarter of FY 18, JNJ’s Pharmaceutical sales reached $10.19 billion, which is better than what many analysts’ were projecting ($9.99 billion). The company’s anti-inflammatory treatment Stelara has posted better-than-expected sales during the quarter of $1.44 billion, however Simponi missed the estimate at $482 million in sales, as the average estimate of the analysts’ amounted to $573.3 million. During the fourth quarter 2018, the prostate cancer drug Zytiga delivered revenue of $786 million, which is better than the expectations of around $695 million. Last year, a patent invalidation scenario for Zytiga allowed the company to enter its generic versions in the market. Therefore, despite Zytiga's strong performance in the fourth quarter, some investors are worried about the loss that could arise due to the patent related issue and its impact on future sales. The company’s consumer business has posted improved performance during the fourth quarter as it matched the sales estimates of $3.55 billion, up from the $3.54 billion delivered during the corresponding quarter in 2017.

Full year Performance (Source: Company Reports)

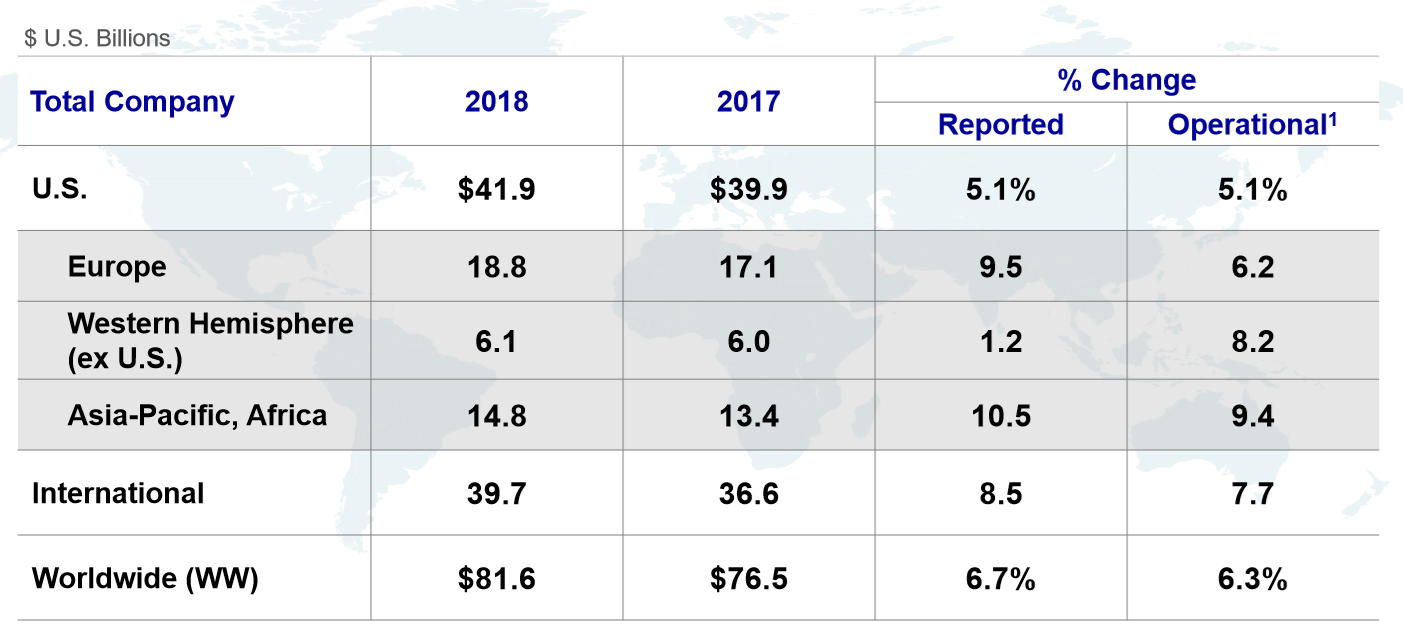

However, the sale of baby care products (with baby powder) dropped to $473 million from $490 million in the fourth quarter of 2017; and JNJ is trying to revive the segment with relaunch of the line of products and introduction of new products. Moreover, JNJ’s medical device segment is still facing a challenging environment as sales of this segment has totaled $6.67 billion, down from market expectations of $6.68 billion and $6.97 billion reported in the corresponding period a year earlier. Additionally, for the full year 2018, Worldwide Consumer sales grew 1.8% to $13.9 versus the prior. For the full-year 2018, Worldwide Pharmaceutical sales has been up by 12.4% to $40.7 billion over the prior year; while Worldwide Medical Devices sales grew 1.5% to $27.0 billion during the full-year 2018 as it included the impact of the divestiture of Lifescan business. JNJ recently announced about completion of the acquisition of Ci:z Holdings Co., Ltd. (which has products like DR.CI:LABO, LABO LABO and GENOMER line of skincare products).

Other Important Developments During the December 2018 Quarter: The group has lately announced that the U.S. Food and Drug Administration (FDA) approved an additional indication for INVOKANA (canagliflozin) for reducing the risk of major adverse cardiovascular (CV) situations like a heart attack, stroke or death in adults along with people having type 2 diabetes and CV diseases. Then the European Commission has given the approval for apalutamide (a next generation oral androgen receptor inhibitor) for treatment of adult patients along with non-metastatic castration-resistant prostate cancer (nmCRPC) and those at an increased risk for developing metastatic disease. A supplemental Biologics License Application to the FDA and a Type II Variation Application to European Medicines Agency (EMA) for getting the approval of STELARA (ustekinumab), have also been submitted. Moreover, a supplemental New Drug Application has been made to the FDA to help the company enhance the horizon for the use of XARELTO (rivaroxaban), meant for the prevention of venous thromboembolism (VTE), or blood clots. Two Type II Variation Applications were submitted to EMA with regards to use of IMBRUVICA (ibrutinib). A worldwide collaboration and license agreement has been signed with argenx BVBA and argenx SE for the development and commercialization of cusatuzumab (ARGX-110), an investigational therapeutic antibody that targets CD70 (immune checkpoint implicated in numerous cancers). Thus, the group is enhancing the spectrum with regards to regulatory approvals on its products.

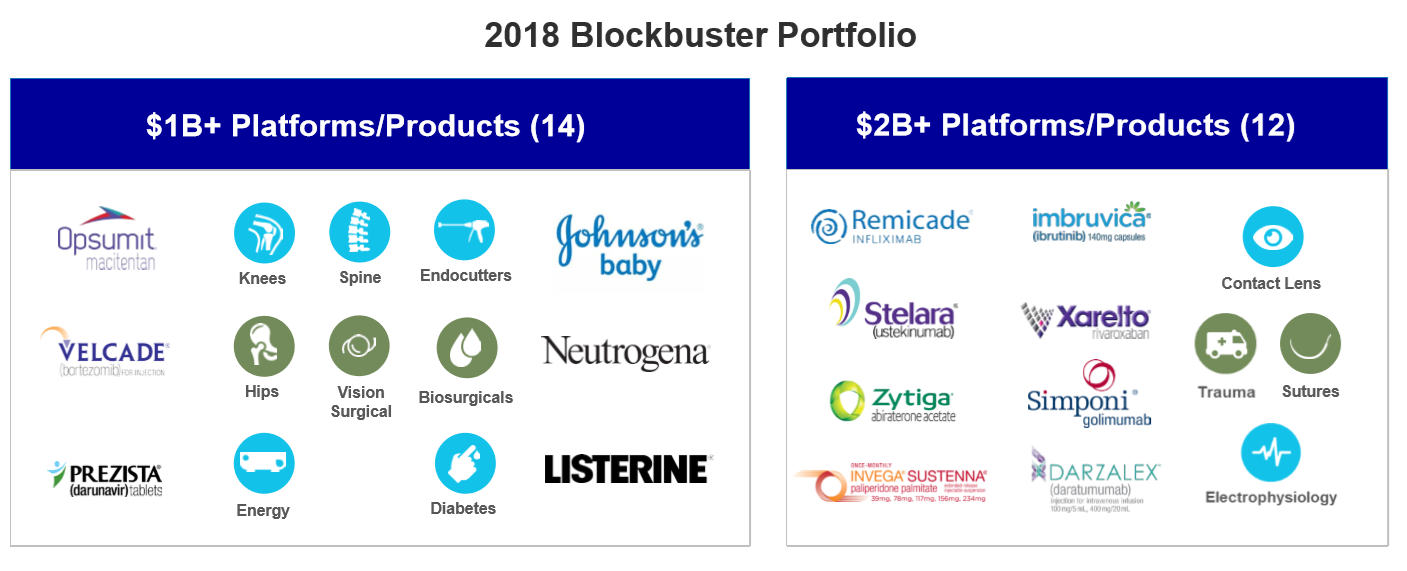

Portfolio (Source: Company Reports)

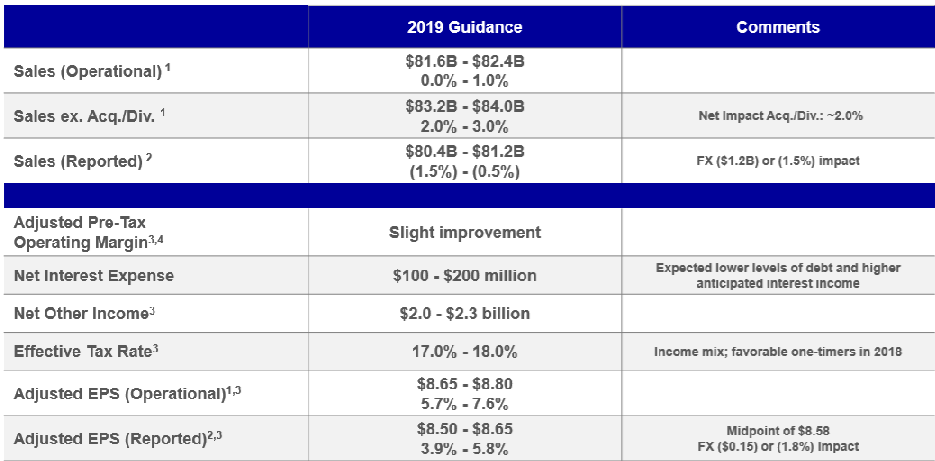

Capital Management and Outlook: In December 2018, JNJ had announced a share repurchase program of up to $5.0 billion of the company's common stock. For full year 2019, JNJ’s sales are expected to be in the range of $80.4 billion to $81.2 billion in view of operational growth to be in the range of 0.0% - 1.0% and expected adjusted operational growth in the range of 2.0% - 3.0%. The full year adjusted earnings are expected to be in the range of $8.50 to $8.65 per share. While the market was expecting some better numbers, the long term view still remains positive.

2019 Guidance (Source: Company Reports)

Stock Recommendation: JNJ stock is trading at a price of $136.35, and has a support at $122 level and resistance at $148. JNJ has posted healthy fourth quarter earnings and has a modest projection for full year sales growth for 2019. This is on the back of the consumer healthcare performance, which is expected to improve while sales suffered owing to issues related with JNJ's iconic baby powder. However, the company is confident that its business will grow on the back of its strong portfolio of products. Given the EPS to grow on a consistent basis, a single digit growth in stock price is expected in the next 12-24 months. We give a “Buy” on JNJ at the current price of $ 136.35.

.png)

JNJ Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...