Kalkine has a fully transformed New Avatar.

Company Overview: Japara Healthcare Limited is an owner, operator and developer of residential aged care facilities. The Company is a private sector residential aged care operator in Australia with over 47,000 resident places and approvals for places nationally across approximately 40 facilities located in Victoria, New South Wales, Queensland, South Australia and Tasmania. In conjunction with the business of providing aged care service, the Company also operates approximately 80 Independent Living Units (ILUs) across over five retirement villages, located adjacent to its aged care facilities. The Company cares for over 4,000 residents, offering a range of living arrangements, amenities, services, meal plans, social activities and care options. It offers independent living, low and high care, Dementia and Alzheimer care, respite and extra services care. Japara Retirement Living offers range of retirement property options, including independent living units/villas and apartments.

.png)

JHC Details

Portfolio Expansion & Increased Investments are Key Catalysts: Japara Healthcare Limited (ASX: JHC) is Australia’s top aged care provider and owns, operates and develops residential aged care homes. It provides elderly care services to over 4,000 residents across ~50 homes in Victoria, Queensland, South Australia, New South Wales, and Tasmania. The company operates approximately 180 independent living units and apartments across five retirement villages in Australia. It’s business model primarily facilitates ‘ageing-in-place’ by servicing a complete range of resident care needs.

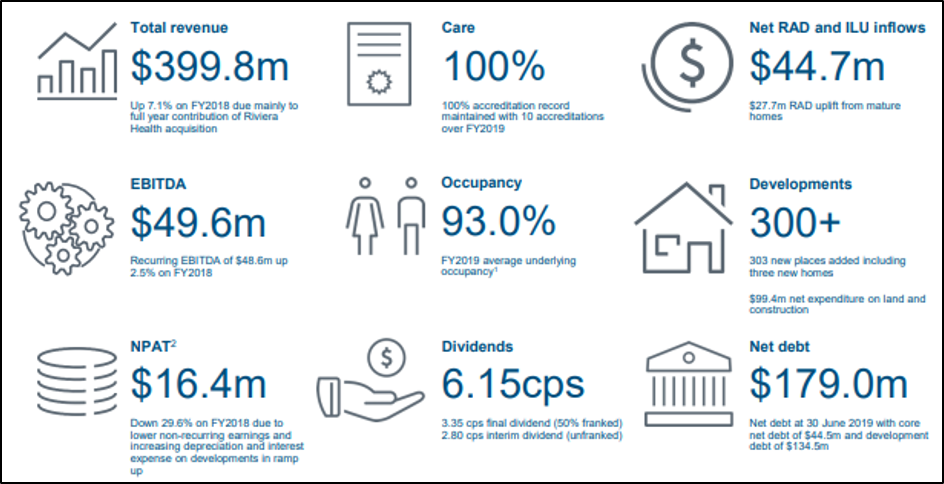

For the year ended 30 June 2019, the company reported revenue of $399.8 million, up around 7.1% year over year. The overall increase in revenue resulted from an expansion in the number of operational places through strategic acquisitions of existing homes, advancement of new homes (Greenfields) along with the construction of extensions to existing homes. EBITDA for the year stood at $49.6 million, down by 2.2% year over year. Resultantly, net profit after tax (NPAT) came in at $16.4 million in FY19.

For FY20 & beyond, the company continues to improve its strategy and focus relating to occupancy, which would become more essential in a situation of intensified competition and heightened customer expectations. The company continues to focus on delivering additional capacity to meet the growing demand for residential aged care facilities. For this purpose, it remains committed for new quality standards, with increased investment in resident amenity and improvements in quality and safety systems. Further, the company focuses on expanding its portfolio and continues to take necessary measures to improve the quality of its existing homes. In doing so, the company has capitalized in new technology to boost care and business operations. The group also intends to commence pilots of a new IT-based clinical and medical management system for implementation across all homes. The move is likely to expand its portfolio and improve financial performance in the coming years.

The company witnessed a compound annual growth rate of 9.2% in revenue in the time span of FY15-FY19. The company has been investing in new technology and service enhancement. Further, the company’s focus on enhancing clinical governance, quality management and resident care systems by construction of new homes and refurbishment of existing properties to expand bed capacity, will drive future earnings. In FY19, total operational beds stood at 4,235 and the company expects to increase the number to 4,627 in FY20 and 4,961 in FY21.

.png)

Bed & Total Residents Highlight (Source: Company Reports)

FY19 Performance: During the period, revenue stood ~$399.9 million, increasing 7.1% year over year.In FY19, JHC retained a 100% accreditation record along with 10 re-accreditation and an additional 57 unexpected evaluation contact audits. Average underlying occupancy in FY19 was ~93%. Total operational places in FY19 stood at 4,235, up from 4.1% in FY18.EBITDA for the year stood at $49.6 million, down 2.2% year over year, largely due to non-recurring items. In FY19, net profit after tax (NPAT) stood at $16.4 million, as compared to $23.3 million reported in FY18. Decrease in NPAT was on the back of development activities with higher depreciation and net interest expense. Diluted earnings per share for the period came in at 6.16 cents per share, as compared to 8.76 cents per share in FY18. The company declared a final dividend of 3.35 cps (50% franked) along with an interim dividend of 2.8 cps, which brought the full-year dividends to 6.15 cents per share.

FY19 Results (Source: Company Reports)

Geographical performance: During the year, total number of operational homes in Queensland stood at 3 homes. With respect to Victoria, New South Wales, South Australia and Tasmania, total number of operational homes was 32, 8, 5 and 2, respectively. Total number of operational places in FY19 came in at 4,235, as compared to 4,069 in FY18.

FY19 Homes (Source: Company Reports)

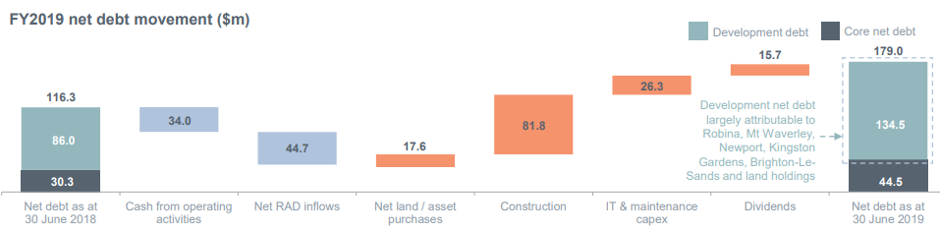

Balance Sheet Position: At the end of the year, the company’s cash balance stood at $31.47 million. For the year, the company had a net bank debt of $179 million, out of which $44.5 million is reflected as core net debt and $134.5 million is development debt. As at 30th June 2019, the company had total bank facilities of $210.5 million. Net Refundable Accommodation Deposit (RAD) and Independent Living Units (ILU) cash inflows came in at $44.7 million in the year, as compared to $41.6 million in FY18.

Net Debt Movement (Source: Thomson Reuters)

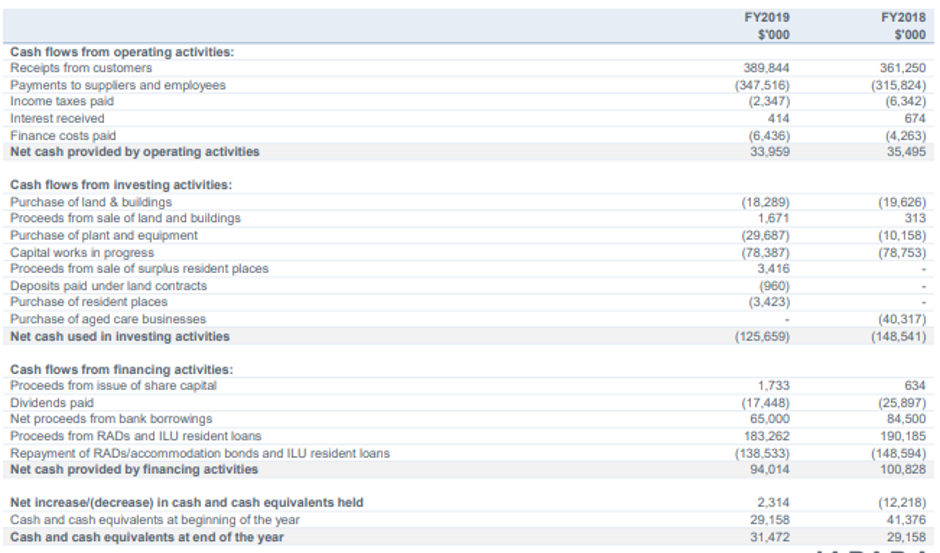

Cash Flow Position: Operating cash inflow in FY19 came in at $33.96 million, as compared to $35.49 million in FY18. Net cash outflow from investing activities in FY19 came in at $125.66 million as compared to $148.54 million in FY18. Net cash inflow from financing activity in FY19 came in at ~$94 million.

Cash Flow Details (Source: Company Reports)

In FY19, the company had an outstanding progress on the development program with an establishment of more than 1,100 net new places. The company opened new homes in Glen Waverley, Rye and Brighton-Le-Sands, with 60 places, 99 places, and 60 places, respectively, during FY19. The company also received planning approval for several latest developments. The company also completed the Brownfield extensions of 84 places at Kingston Gardens and Mirridong. With the above scenario in place, the company is confident about retaining its existing customer base and expects to maintain dominant growth momentum in FY20.

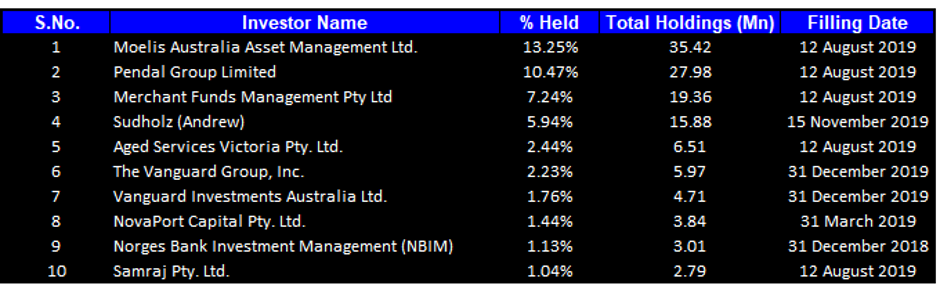

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together form around 46.95% of the total shareholding. Moelis Australia Asset Management Ltd is the entity holding maximum shares in the company at 13.25%. Pendal Group Limited is the second-largest shareholder, with a holding of 10.47%.

Top Ten Shareholders (Source: Thomson Reuters)

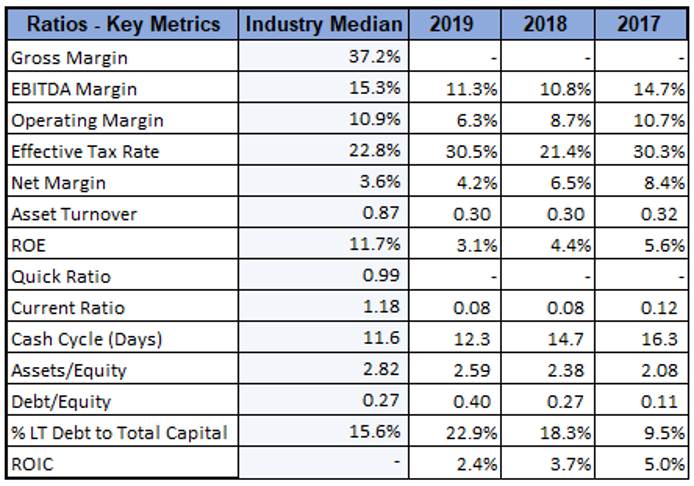

Key Metrics: In FY19, the company had EBITDA margin of 11.3%, which is higher than the FY18 figure of 10.8%, representing decent fundamentals. The company’s debt-to-equity multiple in FY19 stood at of 0.40x. Net margin of the company was reported at 4.2%, higher than the industry median of 3.6%.

Key Metrics (Source: Thomson Reuters)

Outlook: The company expects its FY20 EBITDA to be in the range of 5%-10% lesser than FY19, mainly due to the removal of the Government’s temporary subsidy increase that applied from 20 March 2019 to 30 June 2019, low occupancy and challenges in the funding environment. Further, the company’s recently completed developments are anticipated to lessen industry headwinds. The company remains on track to accommodate new quality standards, with increased investment in resident amenity as well as improvements in quality and safety systems. It continues to improve its strategy and focus related to occupancy, which would become even more vital in an environment of increased competition. Further, JHC continues to emphasis on the distribution of its development program with more than 300 net new places likely to be commenced in FY20, following the completion of existing greenfield and brownfield projects. In FY20 & beyond, the company expects redevelopment of 2,500 sqm of land secured adjacent to Japara’s Elanora home. In FY20, total operational beds are expected to be ~4,627, whereas, the company expects total operational beds to be 4,961 in FY21. The company would be carrying out activities which would support it in the refurbishment along with the implementation of expansion plans for the existing homes. The company’s balanced approach with respect to growth coupled with expansion of its existing portfolio reflects its progress towards sustainable future growth.

.png)

Pipeline Development(Source: Company Reports)

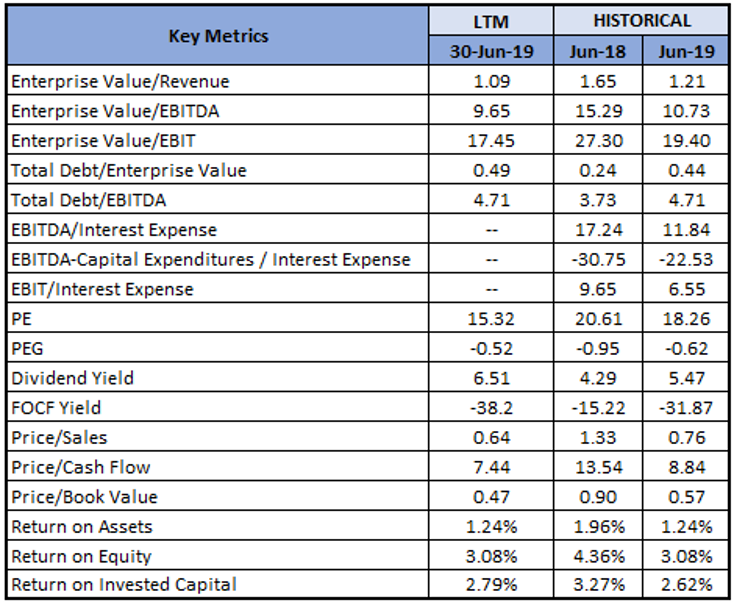

Key Valuation Metrics (Source: Thomson Reuters)

Valuation Methodologies:

Method 1: Price to Earnings Multiple Approach

.png)

Price to Earnings Based Valuation (Source: Thomson Reuters)

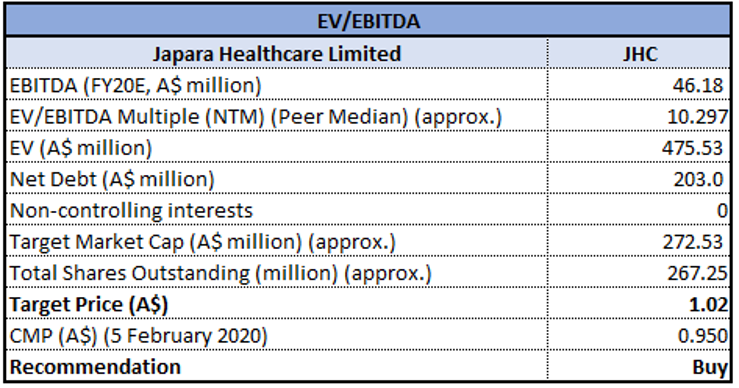

Method 2: EV/EBITDA Multiple Approach

EV/EBITDA Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: The stock of the company is currently trading below the average of its 52-week trading range of $0.920 - $1.550. The stock has a market cap of ~$252.55 million with an annual dividend yield of 6.51% and a P/E multiple of 15.34x, depicting a decent opportunity for accumulation. In FY19, the company delivered a decent result, driven by increased investment in residential aged care amenities as well as improvements in quality and safety systems. The company made substantial investments in infrastructure, people, and technology. JHC has continued to invest in greenfield and brownfield developments to boost future earnings growth while the existing portfolio also continues to provide mature home RAD inflows. The company has also planned its total operational beds to be ~4,627 in FY2020, whereas, the company expects total operational beds to be 4,961 in FY21. In FY19, the company remained on track to distribute dividends to its shareholders and depicted a stable financial position with debt remaining at decent levels.

From the analysis standpoint, the company has recorded revenue CAGR of 9.2% over the last four years. Considering the above factors, we have valued the stock using two relative valuation methods, i.e., P/E multiple and Enterprise Value to EBITDA multiple, and for that purpose, we have considered Regis Healthcare Ltd (ASX: REG), Ryman Healthcare Ltd (ASX: RYM), Pacific Smiles Group Ltd (ASX: PSQ), National Veterinary Care Ltd (ASX: NVL), as peer group which come under healthcare facilities & services category. As a result, we have arrived at a target price of high single-digit to low double-digit growth (in % terms). Hence, we recommend a “Buy” rating on the stock at the current market price of $0.950, up 0.529% on 5th February 2020.

JHC Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...